Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Eastside Stats

The Eastside market is more balanced than it’s been in years—prices have softened and inventory is up, but homes are still selling, the sky isn’t falling, and smart pricing (for sellers) and confident, strategic buying (for buyers) wins the day.

We’re starting the year with 67% more inventory than this time last year, which sounds alarming—but context matters. At 2.6 months of inventory, we’re still solidly in a balanced market, so there’s no need to panic. One of my favorite housing economists keeps saying we’re “back to a 2019 market.” On the Eastside, we actually have 13% more inventory than in 2019, and back then inventory sat at 1.4 months. So… I’m still chewing on that comparison.

Historically, the first quarter tends to start with a bang, though it’s too early to know if that pattern will hold. One wildcard: a meaningful number of sellers chose to cancel listings late last year with plans to relist in 2025. If that’s the case, some of today’s inventory may simply be deferred from Q4. As always—time will tell.

It’s also worth noting that the Eastside is lagging King County overall, which currently sits at 2.1 months of inventory and is “only” 36% higher than last year (and 19% higher than 2019). So while inventory is elevated across the board, the Eastside is feeling it a bit more.

With about half of homes selling within 30 days, the sky is clearly not falling. That said, 57% of sellers needed a price reduction to get sold, so yes—pricing has softened. January is a notoriously wonky month for median price data, but we’re currently down 3% year over year (and up 5% month over month—though that follows an 8% drop the month prior). Zoom out a bit further and the picture changes: since 2020, Eastside prices are up 36%, averaging roughly 7% per year, or about $400,000. Not too shabby.

So what does this all mean?

First: the sky isn’t falling.

Sellers should approach the market as both a price war and a beauty competition.

Buyers can buy with confidence—and if possible, go against the grain. Homes that others overlook often offer the best opportunities (easier said than done, I know).

I’m very curious to see how the rest of January unfolds

October 2025 Eastside Market Update

Months of inventory — how we take the pulse of the market — are down based on pending sales. That’s not surprising, given September’s dip in interest rates ahead of the Fed Funds rate cut, which temporarily boosted buyer confidence. That said, the last two weeks have slowed buyers down. Economic uncertainty isn’t great for decision-making (which, ironically, is exactly what makes now a great time to buy — more on that later).

Median prices are up 2% month-over-month and 3% year-over-year. Interest rates are hovering between 6% and 6.5%, and realistically, that’s probably where they’ll stay for the foreseeable future. (Reason #2 not to delay buying.)

At 2.3 months of inventory, we’re in a balanced market with a slight lean toward sellers. However, we still have more active inventory than we’ve seen in the last five years — (Reason #3 to buy now.) Homes that are well priced are selling fast — 12% of the market sold in the first weekend. But if a home has challenges that pricing doesn’t account for, or it’s simply overpriced, it won’t move without a reduction.

What does this mean?

Sellers: Price conservatively (yes, that means low).

Buyers: Honestly, now is the time — as long as you can afford the payment and plan to stay 3+ years (ideally 5+). Inventory is solid, rates are likely to hold (and can be refinanced later), and economic uncertainty is causing other buyers to pause. That combination creates opportunity.

September Stats

Year-over-year, median prices are basically flat, but they did slip month-over-month for the 4th month in a row. As always, take pricing with a grain of salt—it’s one of the trickiest stats to pin down. With September’s burst of activity and (slightly) lower interest rates, buyer demand will likely keep prices steady through the rest of the year.

Inventory now sits at 2.5 months—technically a balanced market. But here’s the kicker: this is the first time in a decade we’ve seen August’s months of inventory at this level. It feels dramatic because it’s new, but it’s not doomsday. Think of it as shifting from the freeway fast lane at 85 mph down to a solid 55 mph. Is it slower? Sure. But you’re still moving forward.

And the sky? Definitely not falling. Roughly one-third of homes are still selling at or above asking, and two-thirds are going under contract within 30 days. That’s not weakness—it’s recalibration toward a healthier, more sustainable pace.

Buyers: enjoy the breathing room, but stay sharp—19% of homes still sold with multiple offers last month.

Sellers: pricing and presentation matter more than ever. Nail both in the first two weeks if you want top results.

What a Fed Rate Cut Could Mean for Mortgage Rates

The Federal Reserve (the Fed) meets this week, and expectations are high that they’ll cut the Federal Funds Rate. But does that mean mortgage rates will drop? Let’s clear up the confusion.

The Fed Doesn’t Directly Set Mortgage Rates

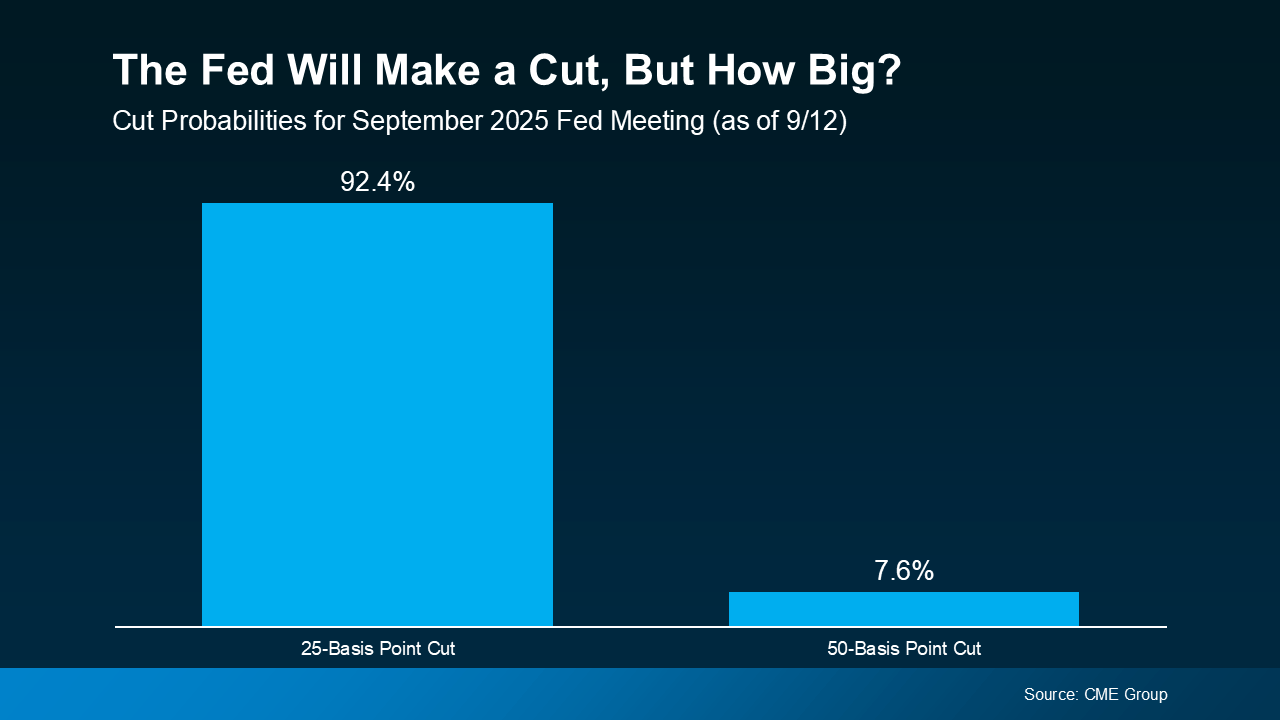

Right now, all eyes are on the Fed. Most economists expect they’ll cut the Federal Funds Rate at their mid-September meeting to try to head off a potential recession.

According to the CME FedWatch Tool, markets are already betting on it. There’s virtually a 100% chance of a September cut. And based on what we know now, there’s about a 92% chance it’ll be a small cut (25 basis points) and an 8% chance it will be a bigger cut (50 basis points):

So, what exactly is the Federal Funds Rate? It’s the short-term interest rate banks charge each other. It impacts borrowing costs across the economy, but it’s not the same thing as mortgage rates. Still, the Fed’s actions can shape the direction mortgage rates take next.

Why Markets Already Saw This Cut Coming

Here’s the part that may surprise you. Mortgage rates tend to respond to what the financial markets think the Fed will do, before the Fed officially acts. Basically, when markets anticipate a Fed cut, that outlook gets priced into mortgage rates ahead of time.

That’s exactly what happened after weaker-than-expected jobs reports on August 1 and September 5. Each time, mortgage rates ticked down as financial markets grew more confident a cut was coming soon. And even though inflation rose slightly in the latest CPI report, the Fed is still expected to make a cut.

So, if the Fed goes with a 25-basis point cut, as expected, that’s likely already baked in to current mortgage rates, and we may not see a dramatic drop.

But if they go bigger and drop their Federal Funds Rate by 50 basis points instead, mortgage rates could come down more than they already have.

So, Where Do Mortgage Rates Go from Here?

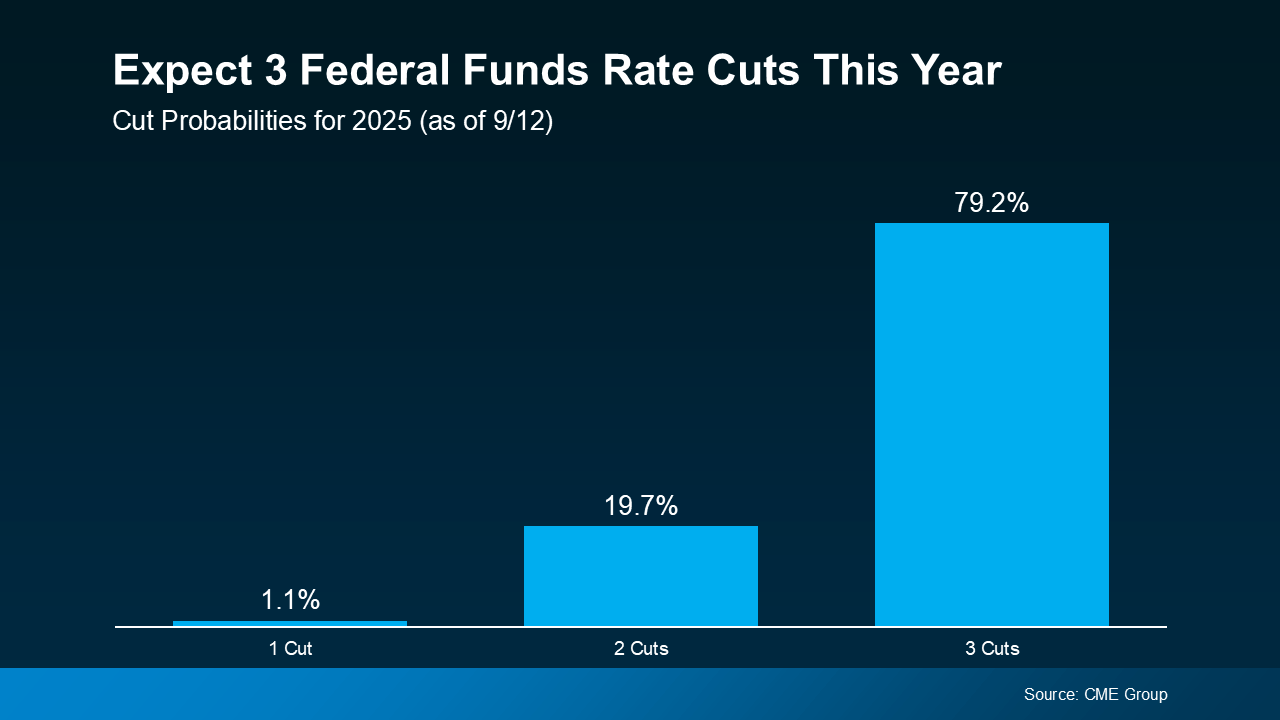

While the upcoming cut may not move the needle much, many experts expect the Fed could cut the Federal Funds Rate more than once before the end of the year. Of course, that’s if the economy continues to cool (see graph below):

As Sam Williamson, Senior Economist at First American, explains:

“For mortgage rates, investor confidence in a forthcoming rate-cutting cycle could help push borrowing costs lower in the back half of 2025, offering some relief to housing affordability and potentially helping to boost buyer demand and overall market activity.”

If multiple rate cuts happen, or even if markets just believe they will, mortgage rates could ease further in the months ahead. But here’s the catch – all of this depends on how the economy evolves. Surprise inflation data or unexpected shifts could quickly change the outlook.

Bottom Line

Mortgage rates likely won’t drop sharply overnight, and they won’t mirror the Fed’s moves one-for-one. But if the Fed begins a rate-cutting cycle, and markets continue to expect it, mortgage rates could trend lower later this year and into 2026.

If you’ve been waiting and watching the housing market, now’s the time to talk strategy. Even small changes in rates can make a meaningful difference in affordability, and understanding what’s ahead helps you make the best decision for your situation.

What Everyone’s Getting Wrong About the Rise in New Home Inventory

You may have seen talk online that new home inventory is at its highest level since the crash. And if you lived through the crash back in 2008, seeing new construction is up again may feel a little scary.

But here’s what you need to remember: a lot of what you see online is designed to get clicks. So, you may not be getting the full story. A closer look at the data and a little expert insight can change your perspective completely.

Why This Isn’t Like 2008

While it’s true the number of new homes on the market hit its highest level since the crash, that’s not a reason to worry. That’s because new builds are just one piece of the puzzle. They don’t tell the full story of what’s happening today.

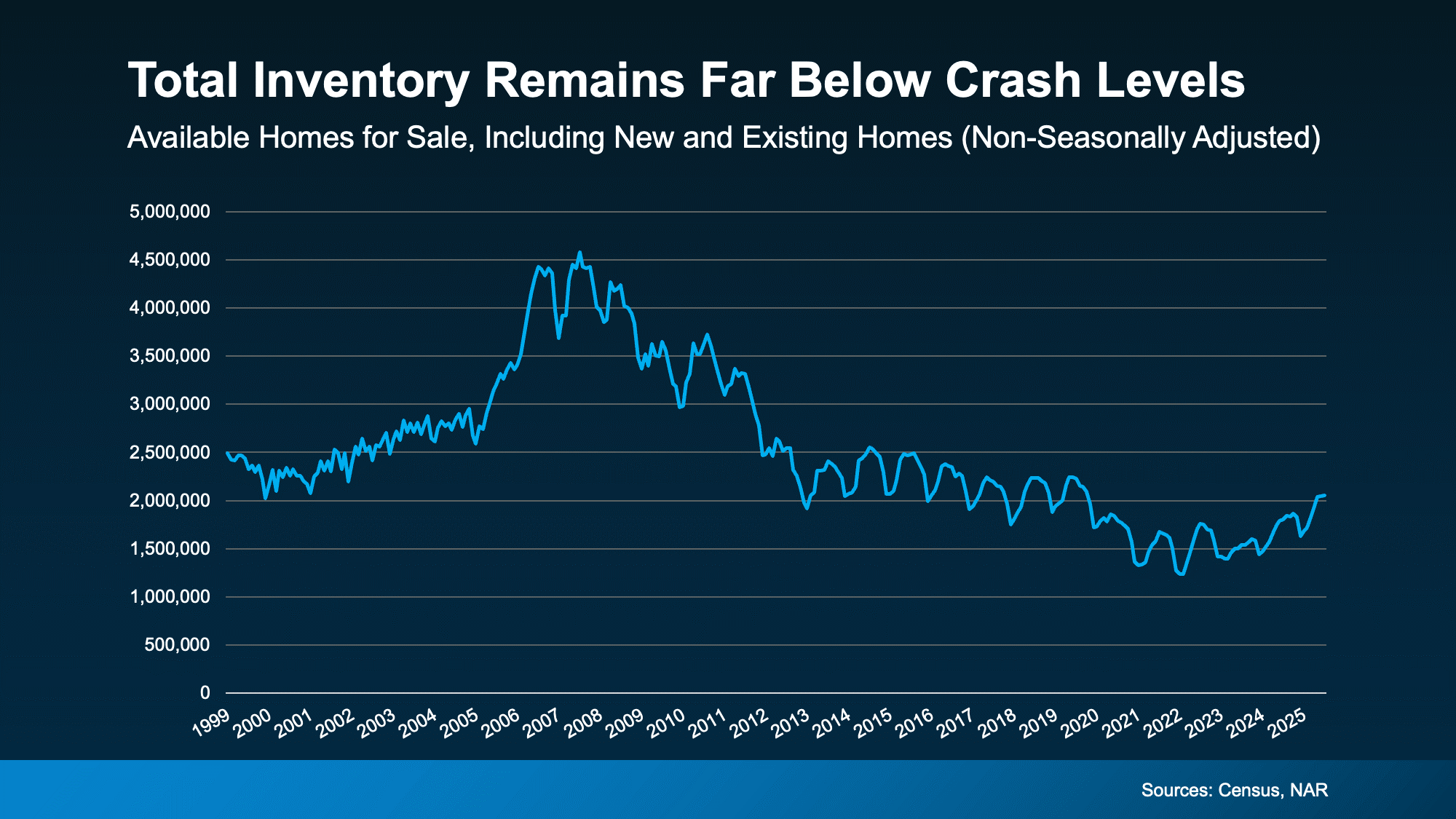

To get the real picture of how much inventory we have and how it compares to the surplus we saw back then, you’ve got to look at both new homes and existing homes (homes that were lived in by a previous owner).

When you combine those two numbers, it’s clear overall supply looks very different today than it did around the crash (see graph below):

So, saying we’re near 2008 levels for new construction isn’t the same as the inventory surplus we did the last time.

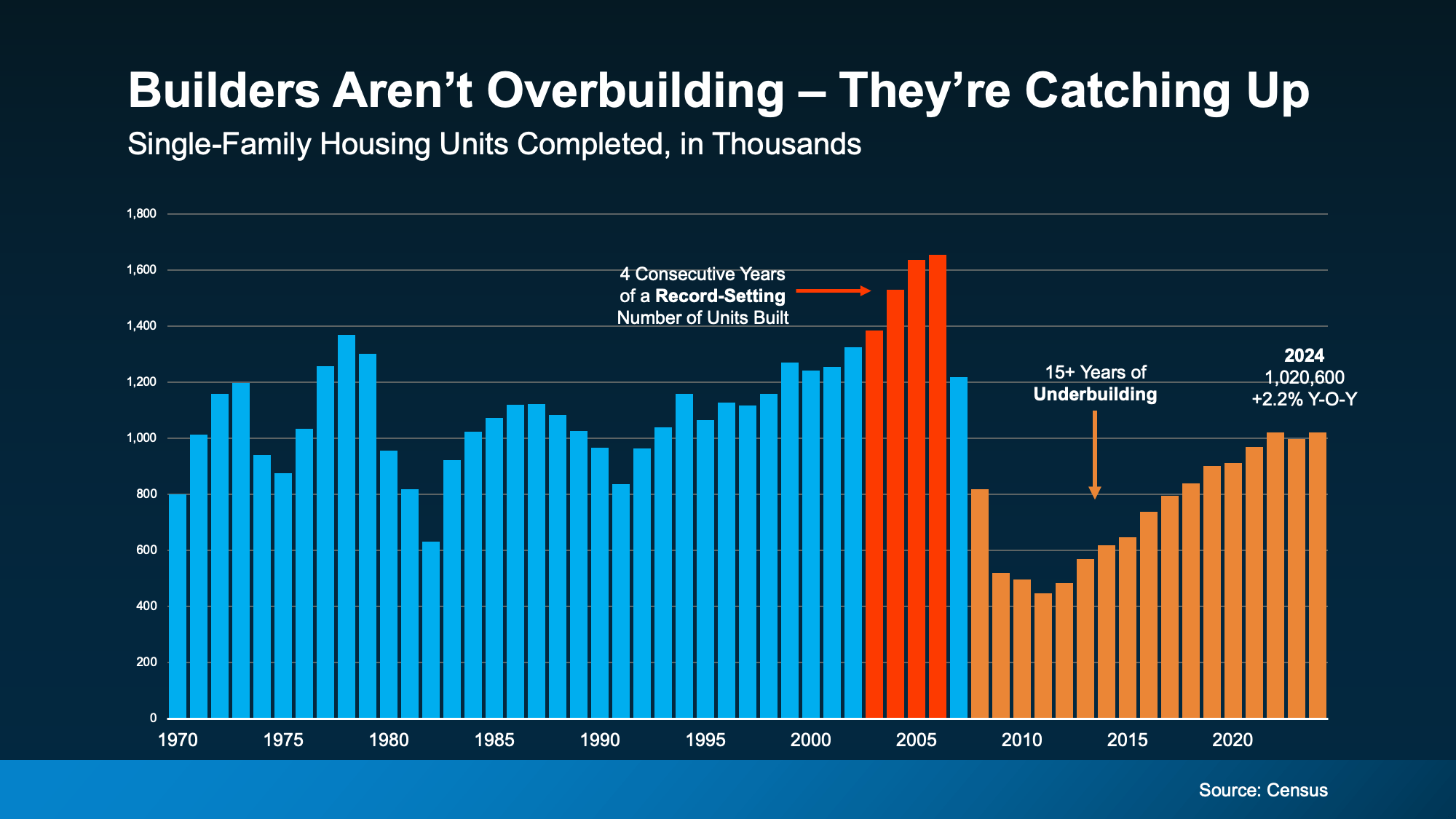

Builders Have Actually Underbuilt for Over a Decade

And here’s some other important perspective you’re not going to get from those headlines. After the 2008 crash, builders slammed on the brakes. For 15 years, they didn’t build enough homes to keep up with demand. That long stretch of underbuilding created a major housing shortage, which we’re still dealing with today.

The graph below uses Census data to show the overbuilding leading up to the crash (in red), and the period of underbuilding that followed (in orange):

Basically, we had more than 15 straight years of underbuilding – and we’re only recently starting to slowly climb out of that hole. But there’s still a long way to go (even with the growth we’ve seen lately). Experts at Realtor.com say it would take roughly 7.5 years to build enough homes to close the gap.

Of course, like anything else in real estate, the level of supply and demand is going to vary by market. Some markets may have more homes for sale, some less. But nationally, this isn’t like the last time.

Bottom Line

Just because there are more new homes for sale right now, it doesn’t mean we’re headed for a crash. The data shows today’s overall inventory situation is different.

If you have questions or want to talk about what builders are doing in our area, let’s connect.