Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

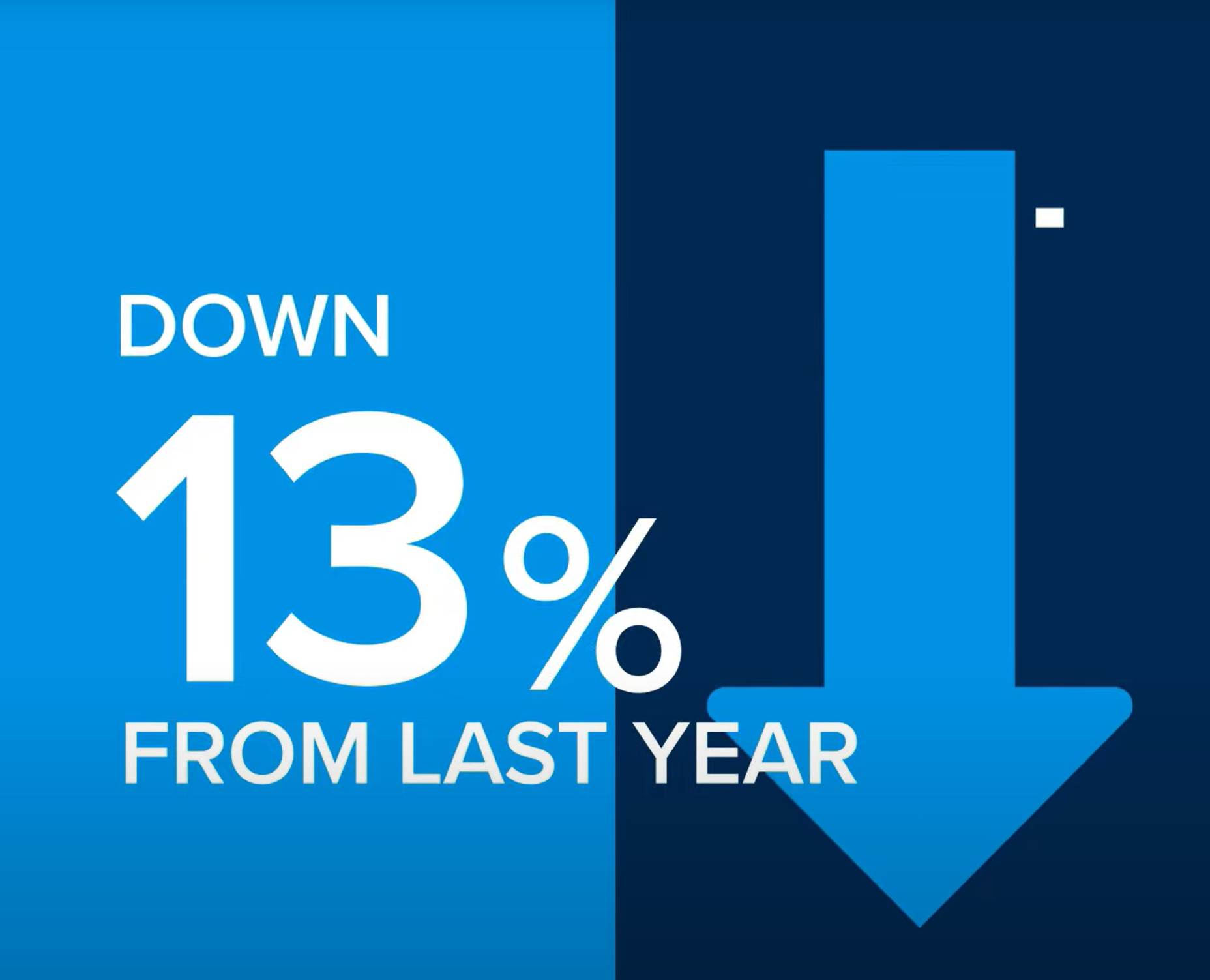

Median pricing crept-up 2% since last month but is down 13% year-over-year. (Note, year-over-year deprecation will continue through June or July.) Interestingly, King County’s year-over-year pricing is flat and Seattle is up 2%, (but, they both will have depreciation next month). Making an analogy, the Eastside was an intense roller coaster like California Screaming/Incredicoaster; whereas, King County and Seattle were a kiddie coaster, like Goofy’s Sky School. Looking bigger picture at Eastside year-over-year pricing, we had 32% (!!) appreciation in 2022 and 22% (!) appreciation in 2021, which lands us 48% higher than January 2020 pricing—not too shabby. Those who bought around the peak should rest assured that they secured the lowest interest rates in history and their monthly payment is lower than if they bought at today’s pricing (and hopefully they can hold on to the home for a several years as pricing will rise). Lastly, at 1.4 months of inventory, we are solidly in a sellers’ market. We need more inventory, which is usually the case in January, so I’m not panicking (yet). Some say the Super Bowl is the kick-off of the real estate season, but I think it’s after mid-winter break (the week of President’s Day) where we really start to see more inventory. Time will tell.

Windermere Real Estate / East, Inc.