Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Wondering If You Should Still Buy a Home Right Now? Here’s What To Keep in Mind.

With economic headlines, global events, and near constant talk about affordability, you may be wondering if this is the right time to move. But here’s what you need to remember.

While recent events do have some impact on the housing market, they don’t take buying off the table. You just have to use a different strategy.

Mortgage Rates Have Been Up Slightly – Here’s Why

After trending down for most of 2025, mortgage rates have been higher again for over roughly a month now. And experts say it’s a result of what’s happening overseas and in the broader economy. As Mark Fleming, Chief Economist at First American, explains:

“Mortgage rates have recently moved higher, driven by geopolitical uncertainty and rising energy costs that are contributing to inflation concerns.”

But what does that really mean for you? Should you wait for everything to settle back down before you buy a home?

The short answer is no. You don’t have to wait.

Your Window To Buy Didn’t Close

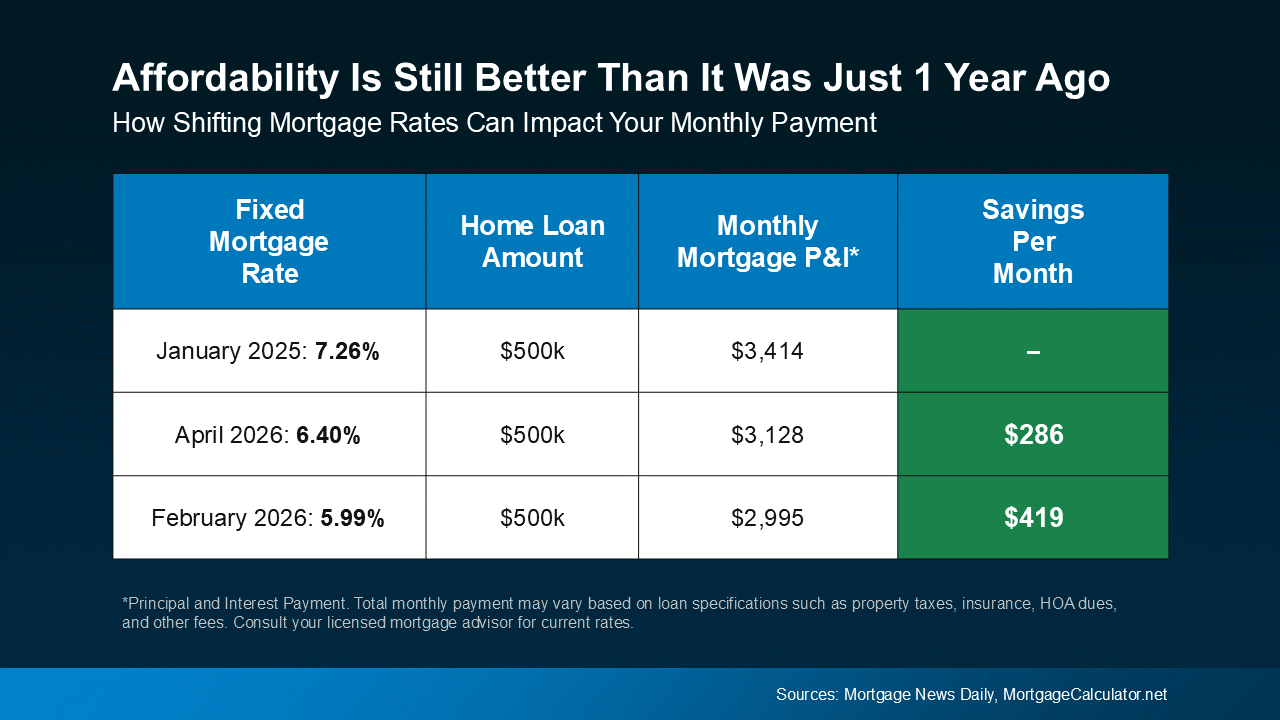

It’s true that a month or so ago, when rates were just shy of 6%, buying felt a bit more affordable. And now that rates are hovering around the mid-6s, monthly payment costs are higher.

But zoom out for a second.

Let’s say you’re taking out a loan for $500k. Even with rates in the mid 6s, you’re still saving roughly $300 on your monthly payment compared to buyers who made their purchase early last year.

That means this recent increase in rates hasn’t erased the progress we’ve seen. Buying is still more affordable than it was just one year ago (see below):

Sure, your monthly payment would’ve been a little less expensive a few weeks back. But hindsight is always 20/20.

The goal moving forward shouldn’t be to perfectly time the market. Things change too quickly for that. Instead, the real goal is to make the best decision you can based on where things are today. And the best advice anyone can give is: brace for volatility.

When It Comes To Rates, Expect the Unexpected

Mortgage rates are going to continue to be move around in the weeks or months ahead as new information and economic reports come out.

Try to remember, you can’t control global events or where rates go next week (or even next month). But you can control how you prepare. If you do that, it becomes less about the headlines, and more about your situation.

If You Want or Need To Move, You Still Can

The simple truth is, if you want or need to move, you still can.

Some buyers are choosing to move forward right now because their needs haven’t changed. A growing family, a job relocation, a lifestyle shift – those things still matter.

And for buyers who do decide to move forward, there are ways to make it work.

For example, you could explore options like adjustable-rate mortgages (ARMs) to get a lower rate upfront. That may or may not be the right fit for you, but it highlights an important point: there are strategies that can help you move, even now.

What matters most is having a plan.

And working with the right agent and lender is a big part of that. With expert help, you’ll:

- Understand your budget and what the math looks like at today’s rates.

- Explore your financing options, including ARMs and assistance programs.

- Have trusted guidance from experts who’ll keep you up to date throughout the process.

Bottom Line

Even though there’s some uncertainty, that doesn’t mean you’re out of options.

If you need to move, you still can. Let’s connect so we can explore all your options and make your move happen.

Before You Fall in Love with a House, Do This First.

Be honest. Have you started looking at homes online yet? If you have, it’s already time to get pre-approved. Because here’s what not enough people know.

If buying a home is on your radar – even if it’s more of a someday plan than a right now plan – you don’t want to wait until later on in the process to tackle this step.

No matter what you’ve heard, pre-approval isn’t about commitment. It’s about clarity. And here are the two big ways pre-approval sets you up for success.

You Know Your Numbers Up Front

During the pre-approval process, a lender will walk through your finances and tell you what you can borrow based on your income, debts, credit score, and more. And once you have that number, your search becomes a lot more focused.

With a mortgage pre-approval, you know what you can borrow, so it’s easier to figure out your ideal price point, and what you can actually afford. And that clarity is key. Because if you just start browsing online and just guess at your price point, you run the risk of falling for a house that’s outside of your price range – or missing out on ones that aren’t.

You want this number to be clearly defined before your search. Here’s why.

You Can Move Quickly When You Find the One

This is how a lot of home searches go today. You scroll through listings just to see what’s out there, and then it happens. You fall in love with something you’ve seen online.

If you’re already pre-approved? You’re probably in great shape.

But if you’re not…

Instead of being able to jump on that house and quickly make an offer, you have to scramble to get a lender, gather the financial documents, and then submit the necessary pre-approval paperwork first. And while you’re waiting to hear back from your lender, someone else who’s more prepared could beat you to the house. As Bankrate explains:

“The best time to get a mortgage preapproval is before you start looking for a home. If you find a home you love but don’t have a preapproval in hand, you likely won’t have time to get preapproved before you need to make an offer . . .”

And that’s avoidable, with the right prep.

Because while you can’t control when the right home shows up, you can be ready for it. Think of it like showing up to the starting line with your shoes tied and your warm-up done – while everyone else is still looking for parking.

It’s not about rushing your timeline. It’s about removing the delay between finding the right home and being able to move on it.

One Thing You Need To Know About Pre-Approvals

Speaking of timing, pre-approvals do have an expiration date. So, be sure to ask your lender how long it’s good for. The Mortgage Reports explains:

“Mortgage preapproval letters are typically valid for anywhere from 30 to 90 days. However, a preapproval can be updated and extended if the lender re-checks your information.”

Doing the right prep and knowing this information can make the whole process a lot smoother.

You don’t have to be ready to buy to be ready to buy.

Getting pre-approved doesn’t mean you’re committing to buy right now. It just means you’ve taken a step to understand your numbers. And when a home catches your attention, you’re prepped and good to go.

Bottom Line

Ask yourself this: if your perfect home popped up tomorrow, would you be ready to make a move?

If the answer is no and you want to buy, it may be time to get pre-approved. You don’t feel behind before your search even officially kicks off.

The #1 Reason Buyers Walk Away (And How To Get Ahead of It)

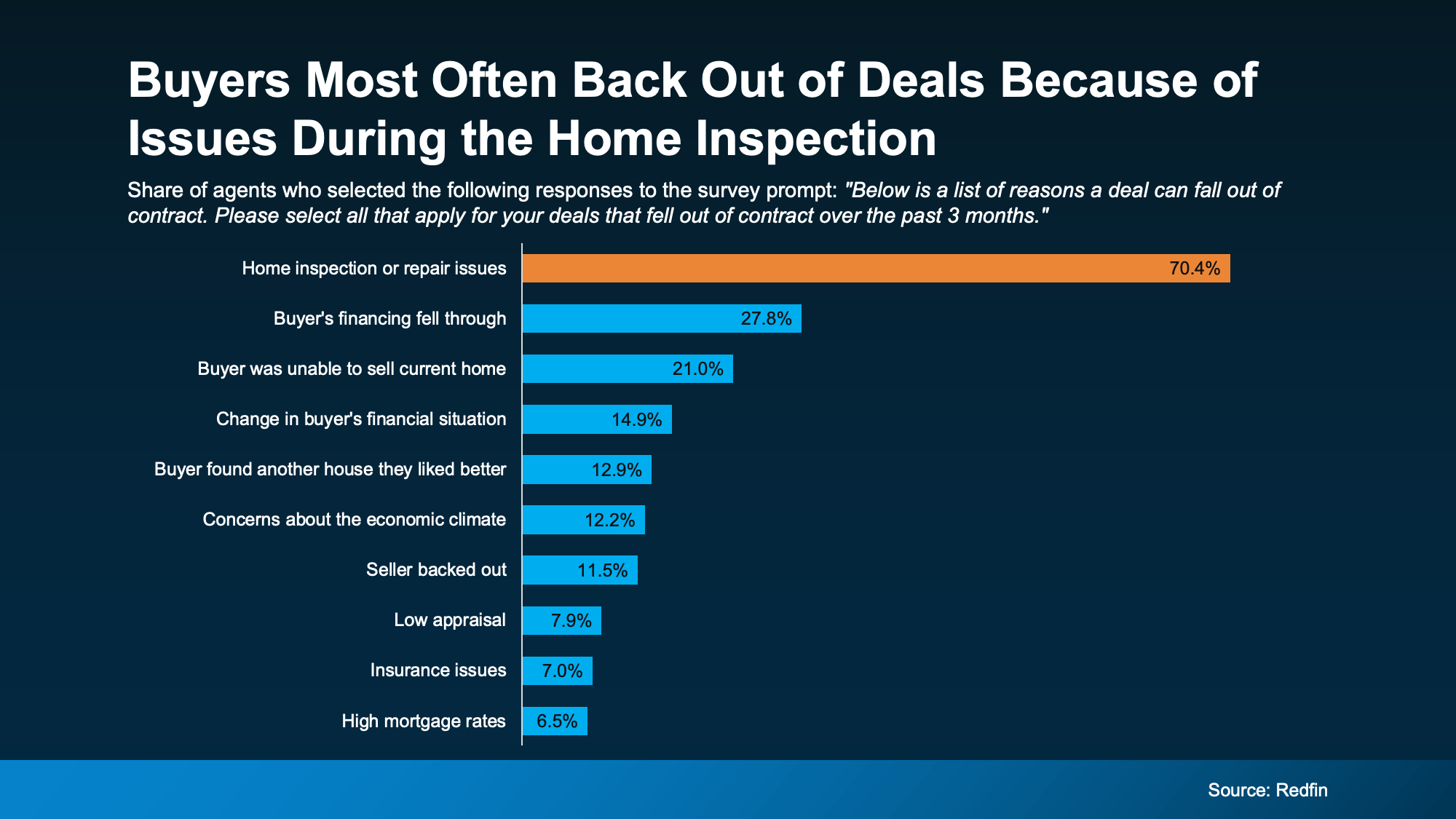

You may have seen headlines on social saying the number of buyers backing out of their contracts is on the rise – and has recently reached a high not seen since 2017. That can sound intimidating. But it varies a lot by market.

And here’s the key thing to understand if you want to sell. A lot of the time, there’s one common cause. And it’s something you can actually control.

Here’s what you can do to get ahead of the biggest dealbreaker before it ever becomes a problem.

The Top Dealbreaker: Issues That Pop Up During the Inspection

A Redfin survey shows over 70% of recently cancelled contracts happened because of issues during the home inspection (see graph below):

And that makes sense. Because today’s buyers have something they didn’t have a couple of years ago: options.

Why Fixing Things Before You List Matters More Today

A few years back, when buyers felt rushed or boxed in due to the limited number of homes for sale, they were more willing to overlook issues.

But in today’s market, skipping essential repairs is one of the fastest ways to lose a deal.

Now that there are more homes to choose from, buyers can be more selective. If a house feels risky, outdated, or like it’s hiding expensive surprises, they’re a lot more likely to walk away. So, what do you have to fix? Just ask an agent.

How Your Agent Can Help Give You the Edge

A local agent will be able to walk through your house and offer advice on what to tackle based on your specific home, your market, and what buyers are prioritizing in your area. They’ll also have first-hand knowledge about some of the biggest turnoffs for buyers today. And you can use that expertise to prevent future headaches.

For example, according to Zillow, these are some of the issues buyers will care the most about:

- Roof leaks or damage: sagging, leaking, etc.

- Plumbing problems: standing water, leaks, water damage, etc.

- Electrical concerns: outdated or exposed wiring, missing GFCI outlets, etc.

- HVAC issues: non-functioning units

- Pest or insect damage: termite colonies, etc.

- Hazardous materials: lead, mold, asbestos, etc.

- Safety/code violations: missing smoke detectors, windows stuck closed, etc.

- Structural problems: cracks in the foundation, sagging floors, etc.

Odds are not all of this even applies to your house. Maybe only 1-2 things do. Or maybe none of them do. It just depends. But an agent will have the tools and resources to help you figure it out and stay one step ahead.

The Benefits of a Pre-Listing Inspection

To buyers, these aren’t cosmetic issues. They’re trust issues. And that’s what you need to watch out for today. Once buyers start wondering “what else might be wrong,” it’s hard to recover momentum.

That’s why some agents are even recommending a pre-listing inspection as a sneak peek into what buyers will see on their own inspection. With that insight, you can:

- Fix concerns before you list, or disclose issues upfront

- Avoid having to respond or negotiate under pressure

- Stop scrambling to find contractors with availability before your closing date

But remember, you don’t have to fix everything. You just have to be strategic about what you do tackle, so you and your buyer aren’t caught off guard.

And that’s why you need an agent who can:

- Decide if a pre-listing inspection is worth it where you live

- Recommend a trusted inspector (if you decide to get one)

- Look at the results with you to identify true dealbreakers in your market

- Help you decide what to fix or what to credit

- Make sure you avoid over-spending or under-preparing

Bottom Line

One of the biggest dealbreakers for buyers today is inspection issues – and that’s something you can control. You just need to be proactive about high-impact repairs before you list.

If you want help figuring out where to focus, let’s connect so we can keep your sale on track from day one.

The Remodel You’ve Been Dreaming About May Be Closer Than You Think

That kitchen you’ve been mentally redesigning…

The bathroom that really needs a refresh…

Or the outdoor space you keep saying you’ll get to someday…

What if you already have what you need to finally make it happen? Because a growing number of homeowners are realizing just that.

Homeowners are expected to spend over $522 billion on home improvements by the end of 2026 – and they’re not draining their savings accounts to get it done. Many are using their home equity.

And if you’ve owned your home for 10+ years, there’s a chance you could use your equity to fund some home upgrades too. Let’s break down what you need to know first.

What Is Equity? And How Does It Help?

Equity is the difference between what your house is worth and what you owe on your mortgage. And according to Cotality, the average homeowner has about $313,000 worth of equity today. That’s more than enough to finally knock some projects off your list. And more people are realizing they can use that to give their home a little TLC.

Research coming out of Meridian Link says home improvements are the top thing people are using their equity for today.

Top Motivations for Equity-Based Borrowing:

- Funding home improvements (45%)

- Using it to pay down other debts / debt consolidation (16%)

- Investing in other properties (16%)

Maybe it makes sense for you to do the same. But here’s what’s important. Just because you can use your equity doesn’t mean you have to. It also doesn’t mean every project makes sense.

What Projects Are Actually Worth It?

If you’re going to go this route, you’ll want to focus on upgrades that actually pay off. A good renovation should be something that improves the value of your home. Because, even if you’re not planning to sell soon, you want to make sure you’re setting yourself up for success when you do.

And an agent is the best resource as you weigh your options. They know what other homeowners are doing and what buyers in your area like. And that can be really helpful as you narrow down your project list. As the National Association of Realtors (NAR) puts it:

“Being able to help sellers prioritize home improvements and maximize their net on the sale is a key value real estate agents offer.”

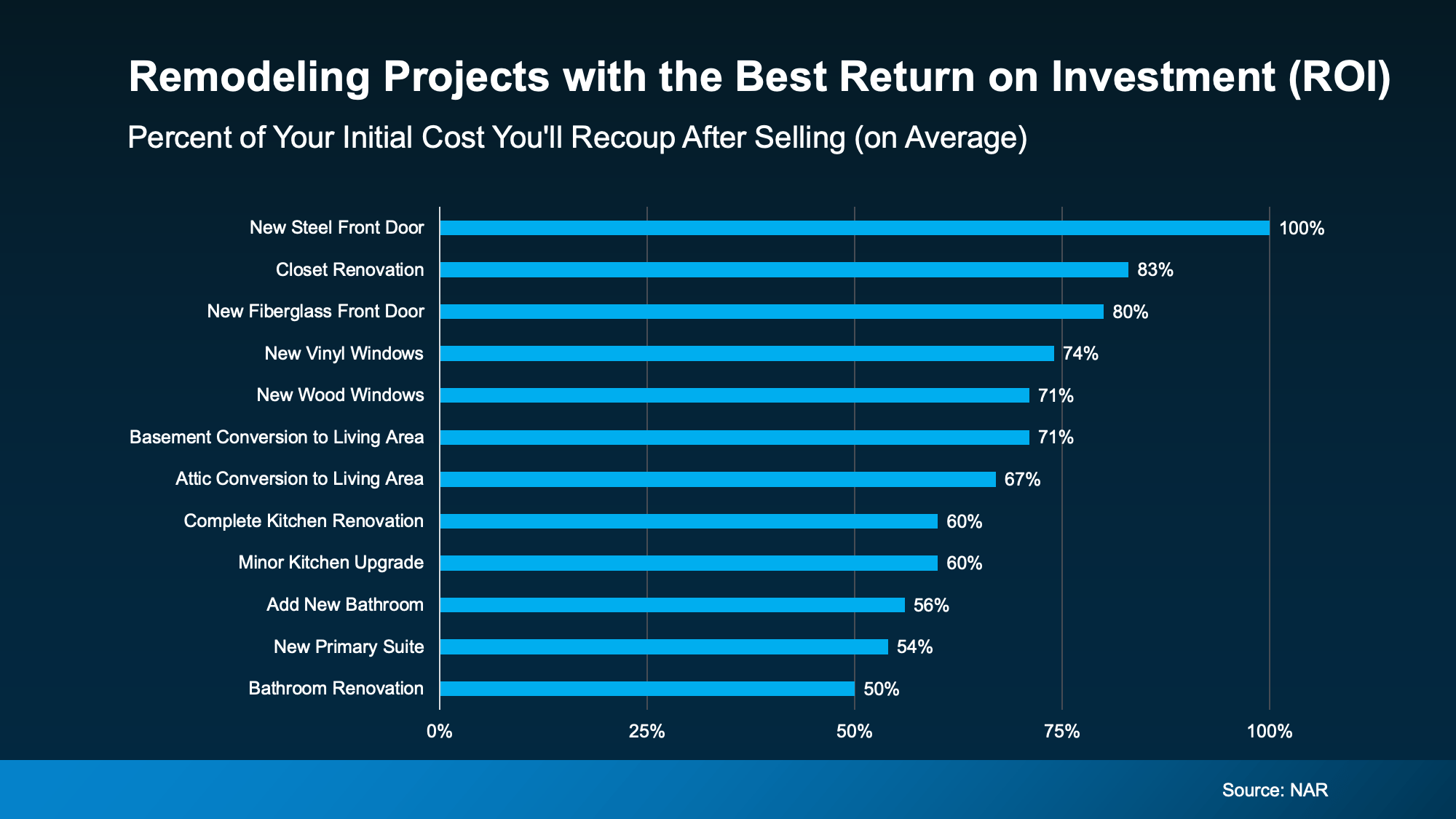

Here’s a quick rundown of the projects with the best potential to recoup your costs according to NAR (see graph below). While it’s a good starting point, just remember it can’t match the expertise an agent can provide.

As you can see, there’s a wide range of projects on that list. Yes, some are bigger-ticket items, like kitchens or baths. But others are smaller updates with surprisingly strong ROI.

As you can see, there’s a wide range of projects on that list. Yes, some are bigger-ticket items, like kitchens or baths. But others are smaller updates with surprisingly strong ROI.

A new front door is a great project. But it’s not something to use your equity for. But revamping your kitchen? That’s where your equity can come in and lighten the load.

Where To Go from Here

Whether the project you’ve been thinking about is on this list or not, chat with an agent to make sure it’s worth the time, money, and effort before calling in any contractors.

Because the goal isn’t to do everything, it’s to invest where it counts.

And if you want to use your equity to get one of the bigger projects done, meet with a financial advisor too. Because you’ll want to make sure you’ll maintain a good loan-to-value (LTV) threshold even after using your equity. That way you have all the information you need to make your decision.

Bottom Line

Whether you’re selling next year or just giving your house some TLC, the right home improvements today can set you up for success tomorrow. And the best part? Your equity may be the key to making it happen.

What’s one upgrade you’ve been thinking about – and wondering if it’s worth it?

Let’s have a quick conversation about whether it’s the right decision for your home.

Four Ways Your Home Equity Can Work for You

You may have heard homeowners today have a lot of equity built up. But what does that really mean? Let’s break it down.

Because your equity isn’t just a number, it’s a powerful asset that can help you take your next big step in life.

How Much Equity Does the Typical Homeowner Have?

Here’s how it works. As you pay down your loan and home prices rise through the years, the share of your home that you own free and clear grows. That’s your equity.

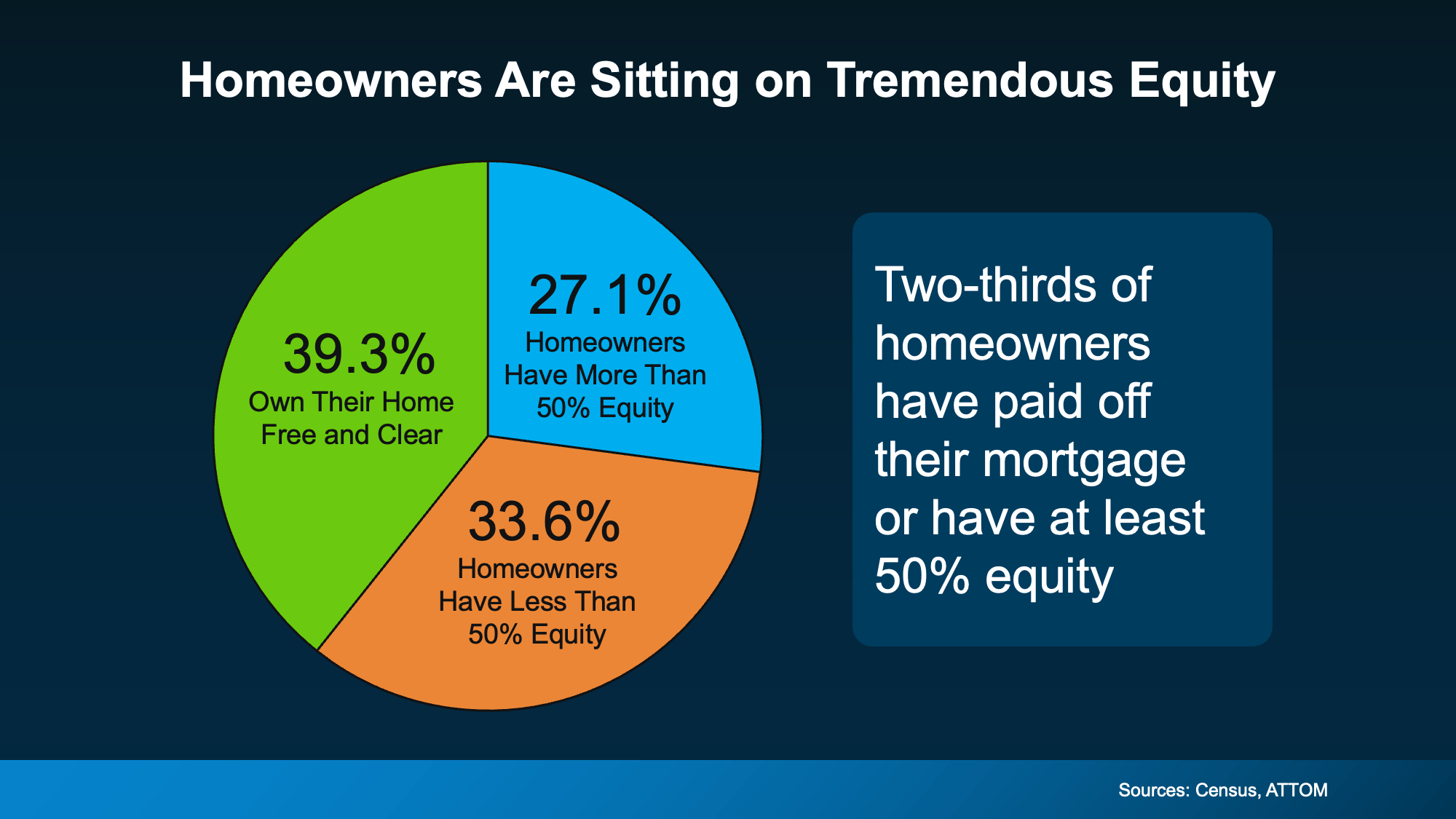

And according to data from the Census and ATTOM, two-thirds of homeowners have a substantial amount of it today.

39% own their home outright without owing anything on it. And another 27% have at least 50% equity in their homes (see chart below):

That’s a big deal. And just in case you’re wondering how that translates into real dollars, Cotality says the typical homeowner has almost $300k in equity today.

That’s six figures.

And whether you have that much, even more, or a bit less, here are a few examples of how you can use it.

Ways You Could Use Your Home Equity

1. Move Into a Home That Better Fits Your Life

Your needs change over time. Maybe your home is starting to feel cramped, or maybe you have more space than you need now that your adult children have moved out. Either way, you can use your equity as a down payment on a home that’s a better fit for what you need now, and going forward. You may even have enough equity to buy your next house in cash.

2. Upgrade Your Current Home

And if you’re not ready to move just yet, you could reinvest it in your current home instead. Renovations like a kitchen refresh or updated bathrooms could add value when it’s time to sell down the line. Just be sure to talk to a real estate agent before you tackle your project list, so you can prioritize updates that’ll give you the biggest return later on.

3. Fund a Major Life Goal

Equity can also help fund your life goals – whether it’s starting a business, saving for retirement, covering education costs, or helping out someone you love. Some homeowners are even passing down some of that wealth to help fund a loved one’s down payment on a home.

4. Avoid Foreclosure in Tough Times

If you’re struggling with payments, your equity can also be a lifeline. Many homeowners who hit financial hardships can sell their homes and walk away with money in their pockets instead of facing foreclosure. If that’s something on your mind, talk to a real estate expert about your options and how your equity can help.

Your Next Steps

If you’re interested in using your equity for one of the reasons above, here’s what to do:

- Step 1: Ask a local agent for a personalized equity assessment on your home.

- Step 2: Meet with a financial advisor if you’re interested in using that equity.

Because when it comes to tapping into this resource, there are a few things you’ll want to keep in mind – like making sure you still have a good loan-to-value ratio (LTV) even if you use some of your equity.

That means, as a general rule of thumb, you want to maintain at least 20% equity in your home as a financial cushion – something many homeowners didn’t know back in the crash of 2008.

The good news is, according to the Intercontinental Exchange, most of today’s equity meets that guideline:

“As of Q4, mortgage holders have $17.3T in home equity, including $11.2T in tappable equity ‒ accessible via cash-out refinances or home equity lines while maintaining 20% equity in the property . . . ”

Bottom Line

Your home equity is one of the biggest financial assets you have. Whether you’re thinking about moving, remodeling, or working toward a big goal, it’s worth exploring your options. Reach out to a financial advisor to learn more.

What’s one goal you have that you’d go after right now, if you had the funds for it?

October 2025 Eastside Market Update

Months of inventory — how we take the pulse of the market — are down based on pending sales. That’s not surprising, given September’s dip in interest rates ahead of the Fed Funds rate cut, which temporarily boosted buyer confidence. That said, the last two weeks have slowed buyers down. Economic uncertainty isn’t great for decision-making (which, ironically, is exactly what makes now a great time to buy — more on that later).

Median prices are up 2% month-over-month and 3% year-over-year. Interest rates are hovering between 6% and 6.5%, and realistically, that’s probably where they’ll stay for the foreseeable future. (Reason #2 not to delay buying.)

At 2.3 months of inventory, we’re in a balanced market with a slight lean toward sellers. However, we still have more active inventory than we’ve seen in the last five years — (Reason #3 to buy now.) Homes that are well priced are selling fast — 12% of the market sold in the first weekend. But if a home has challenges that pricing doesn’t account for, or it’s simply overpriced, it won’t move without a reduction.

What does this mean?

Sellers: Price conservatively (yes, that means low).

Buyers: Honestly, now is the time — as long as you can afford the payment and plan to stay 3+ years (ideally 5+). Inventory is solid, rates are likely to hold (and can be refinanced later), and economic uncertainty is causing other buyers to pause. That combination creates opportunity.

September Stats

Year-over-year, median prices are basically flat, but they did slip month-over-month for the 4th month in a row. As always, take pricing with a grain of salt—it’s one of the trickiest stats to pin down. With September’s burst of activity and (slightly) lower interest rates, buyer demand will likely keep prices steady through the rest of the year.

Inventory now sits at 2.5 months—technically a balanced market. But here’s the kicker: this is the first time in a decade we’ve seen August’s months of inventory at this level. It feels dramatic because it’s new, but it’s not doomsday. Think of it as shifting from the freeway fast lane at 85 mph down to a solid 55 mph. Is it slower? Sure. But you’re still moving forward.

And the sky? Definitely not falling. Roughly one-third of homes are still selling at or above asking, and two-thirds are going under contract within 30 days. That’s not weakness—it’s recalibration toward a healthier, more sustainable pace.

Buyers: enjoy the breathing room, but stay sharp—19% of homes still sold with multiple offers last month.

Sellers: pricing and presentation matter more than ever. Nail both in the first two weeks if you want top results.

What a Fed Rate Cut Could Mean for Mortgage Rates

The Federal Reserve (the Fed) meets this week, and expectations are high that they’ll cut the Federal Funds Rate. But does that mean mortgage rates will drop? Let’s clear up the confusion.

The Fed Doesn’t Directly Set Mortgage Rates

Right now, all eyes are on the Fed. Most economists expect they’ll cut the Federal Funds Rate at their mid-September meeting to try to head off a potential recession.

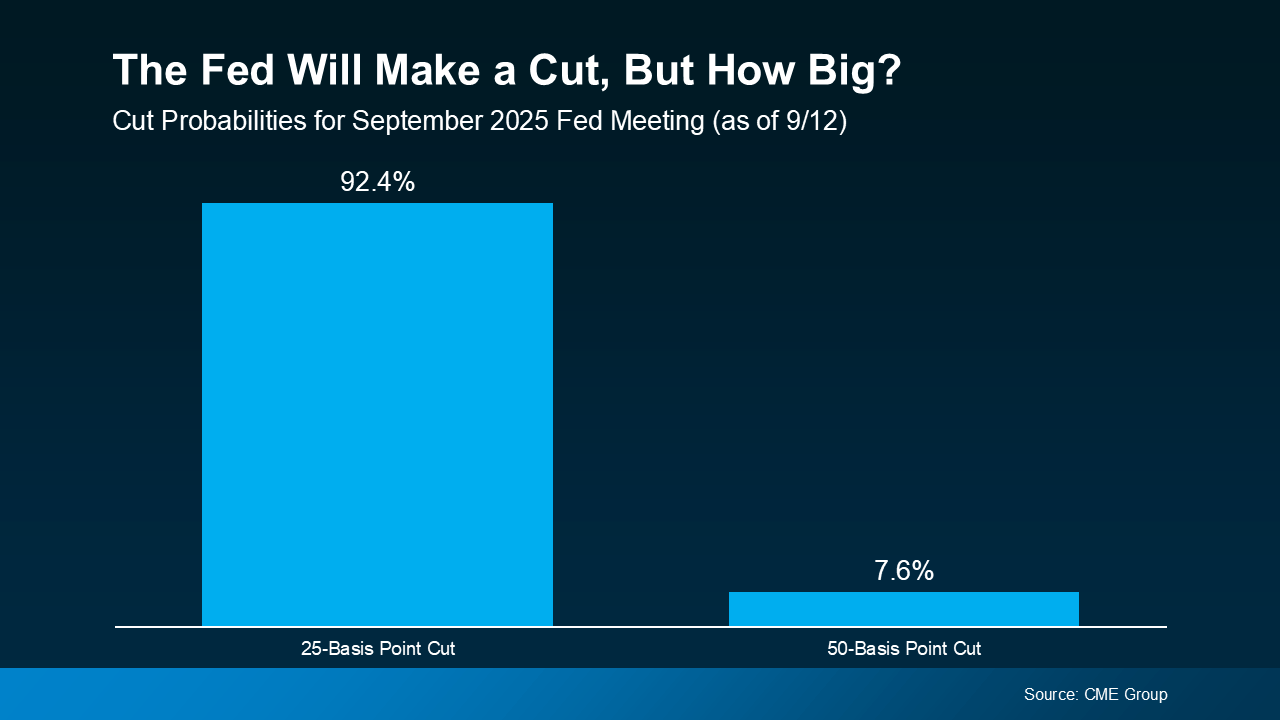

According to the CME FedWatch Tool, markets are already betting on it. There’s virtually a 100% chance of a September cut. And based on what we know now, there’s about a 92% chance it’ll be a small cut (25 basis points) and an 8% chance it will be a bigger cut (50 basis points):

So, what exactly is the Federal Funds Rate? It’s the short-term interest rate banks charge each other. It impacts borrowing costs across the economy, but it’s not the same thing as mortgage rates. Still, the Fed’s actions can shape the direction mortgage rates take next.

Why Markets Already Saw This Cut Coming

Here’s the part that may surprise you. Mortgage rates tend to respond to what the financial markets think the Fed will do, before the Fed officially acts. Basically, when markets anticipate a Fed cut, that outlook gets priced into mortgage rates ahead of time.

That’s exactly what happened after weaker-than-expected jobs reports on August 1 and September 5. Each time, mortgage rates ticked down as financial markets grew more confident a cut was coming soon. And even though inflation rose slightly in the latest CPI report, the Fed is still expected to make a cut.

So, if the Fed goes with a 25-basis point cut, as expected, that’s likely already baked in to current mortgage rates, and we may not see a dramatic drop.

But if they go bigger and drop their Federal Funds Rate by 50 basis points instead, mortgage rates could come down more than they already have.

So, Where Do Mortgage Rates Go from Here?

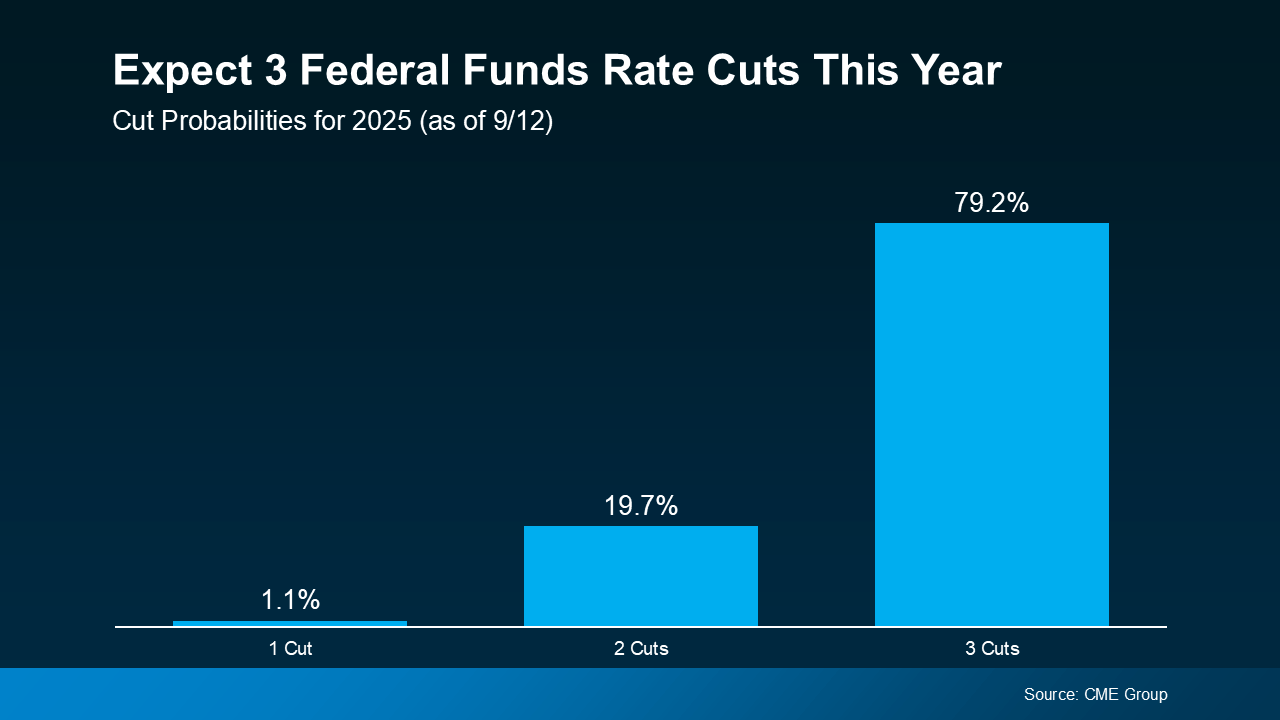

While the upcoming cut may not move the needle much, many experts expect the Fed could cut the Federal Funds Rate more than once before the end of the year. Of course, that’s if the economy continues to cool (see graph below):

As Sam Williamson, Senior Economist at First American, explains:

“For mortgage rates, investor confidence in a forthcoming rate-cutting cycle could help push borrowing costs lower in the back half of 2025, offering some relief to housing affordability and potentially helping to boost buyer demand and overall market activity.”

If multiple rate cuts happen, or even if markets just believe they will, mortgage rates could ease further in the months ahead. But here’s the catch – all of this depends on how the economy evolves. Surprise inflation data or unexpected shifts could quickly change the outlook.

Bottom Line

Mortgage rates likely won’t drop sharply overnight, and they won’t mirror the Fed’s moves one-for-one. But if the Fed begins a rate-cutting cycle, and markets continue to expect it, mortgage rates could trend lower later this year and into 2026.

If you’ve been waiting and watching the housing market, now’s the time to talk strategy. Even small changes in rates can make a meaningful difference in affordability, and understanding what’s ahead helps you make the best decision for your situation.