Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

April 2025 Market Update

After three months of stabilization around $1.7M, it’s clear the 10% median price increase is real. That said, the 2% appreciation is misleading: prices surged 18% early in 2024 before leveling off to a more sustainable 6% annual growth rate, which better reflects the true market appreciation.

Looking ahead, a modest pricing correction seems likely, driven by rising inventory and broader economic uncertainty. The previously cited 1.1 months of inventory no longer reflects current conditions—we are approaching 2.0 months, indicating a shift toward a balanced market.

What are the implications? For sellers: price conservatively to align with current market conditions. For buyers: continue to focus on affordability through your monthly payment, and do not hesitate to move forward with a purchase if it fits your financial goals.

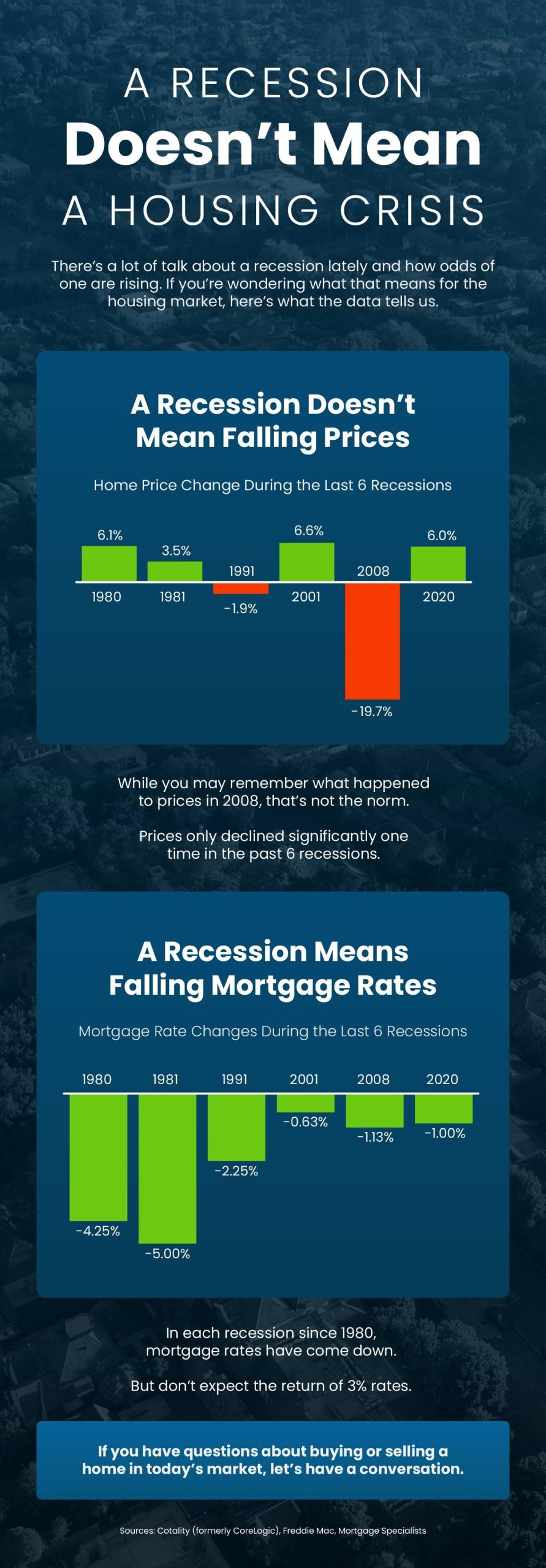

A Recession Doesn’t Mean a Housing Crisis

There’s a lot of talk about a recession lately and how the odds of one are rising. If you’re wondering what that means for the housing market, here’s what the data tells us. While you may remember the price crash in 2008, that’s not the norm. Looking back all the way to 1980, home prices usually rise and mortgage rates tend to fall. If you have questions about buying or selling a home in today’s market, let’s have a conversation.

Paused Your Moving Plans? Here’s Why It Might Be Time To Hit Play Again

Last year, 70% of buyers abandoned their home search – and maybe you were one of them. It makes sense. Inventory was low, prices were high, and mortgage rates were up and down like a rollercoaster. All of that made it really hard to find a home you loved – and could afford.

But guess what? The market is shifting.

So, if you paused your moving plans in 2024, it might be time to hit play again. Here’s why.

More Inventory Opens Up More Options

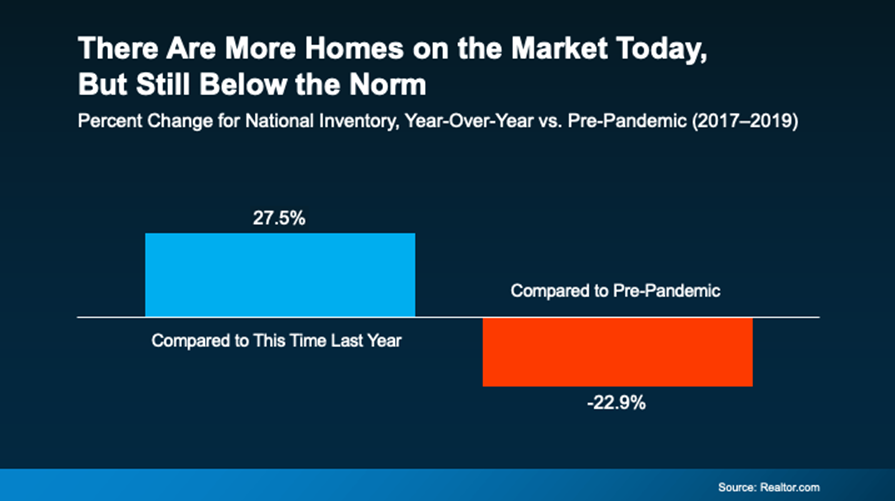

Even if you could make the numbers work, the lack of available homes in recent years probably made it hard to come by something that fit your needs. But inventory is rising, which means you have more options now.

According to Realtor.com, inventory has jumped 27.5% since this time last year (see graph below):

So, if you were reluctant to list your house because you weren’t sure where you’d go if it sold, you have more choices than you did a year ago. That’s a big win.

Homes Are Staying on the Market Longer, Too

When the supply of homes for sale is low, they’re snatched up quickly because there just aren’t enough of them to go around. And a few years ago, that meant your house could sell overnight. While that’s not always a bad thing, if you’re planning a move and also need to find your next home, a slower pace isn’t the end of the world. In fact, it’s welcome relief.

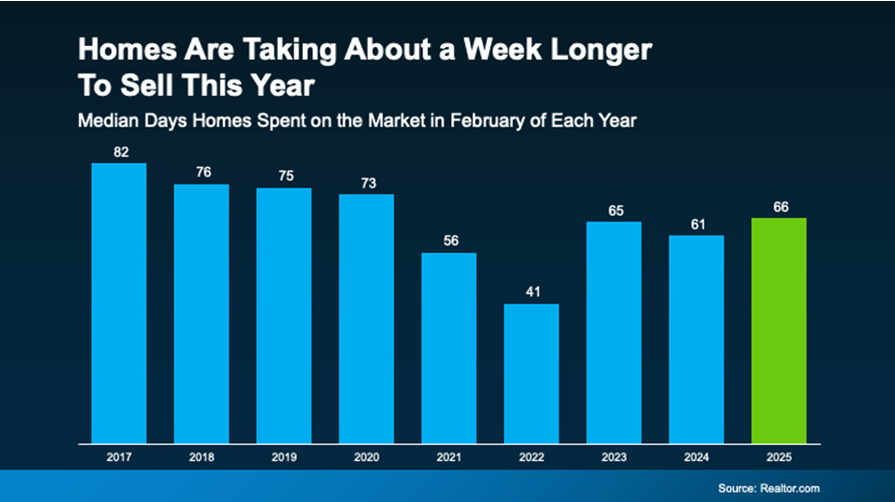

Now that inventory has grown, homes are staying on the market longer, meaning you don’t have to feel as rushed in the process (see graph below):

The latest data shows the typical time homes spent on the market went up by about 8% this year – that’s higher than we’ve seen since 2020, but still a faster pace than before the market ramped

- And it’s about a week longer than last year. Talk about a sweet spot for movers. It may seem like just a few days, but it gives you more flexibility and time to be thoughtful about your decisions. As Hannah Jones, Senior Economic Research Analyst at Realtor.com, notes:

“There are more homes for sale than in the last few years, which means the market pace is a bit more manageable–with longer days on market–and many sellers are more flexible . . . Though buyers face still-high housing costs, they may find a bit more give in the market, which could give them more time to make a decision, even in the busy spring and summer months.”

And if you’re thinking – but wait – doesn’t that mean it will be harder to sell my house? Don’t worry. With inventory still almost 23% below the pre-pandemic norm, well-priced homes are selling, especially as more buyers step back into the game this season.

Bottom Line

With growing inventory, sellers who want to upgrade, downsize, or relocate have more choices. Plus, with less pressure to rush into an offer, it could be a great time to revisit your home search if you’ve put it on hold.

With more homes on the market and more time to make decisions, what else do you need to see in order to kickstart your home search again? Let’s talk about what’s happening in our local market right now.

Buying Your First Home? It’s Okay To Feel Nervous

Buying your first home is exciting, but let’s be real – it can also feel overwhelming. It’s a big step, and with that comes plenty of questions. Am I making the right decision? Can I really afford this right now? Will I be able to make ends meet if I have unexpected repairs? What if I lose my job?

Here’s the thing: every first-time homebuyer has these thoughts.

The homebuying process has always been a mix of excitement and nerves, and that’s completely normal. Here’s some information that can give you a bit of perspective, so you don’t have these concerns.

Focus on What You Can Control

Since homeownership is new to you, you’re probably feeling like it’s hard to know what to budget for. And that can be a bit scary. You’ll have the mortgage, home insurance, and maintenance to think about – maybe even lawn care or homeowner’s association (HOA) fees. It’s easy to let the dollar signs be overwhelming. As Zillow says:

“Buying a house is a big decision, and you might feel confused and indecisive as you assess your current financial situation and try to work through whether or not the timing is right. Making big life choices might come with some self-doubt, but crunching the numbers and thinking about what you want your life to look like will help guide you down the right path.”

The important thing is to focus on what you can control. By partnering with a local agent and a trusted lender, you can get a clear understanding of what you can borrow for your home loan, what your monthly payment would be, and how your mortgage rate can impact it. And since that payment will likely be your biggest recurring expense, the key is to make sure the number works for you.

Don’t Stress About Repairs

The maintenance and repairs? Those can be a little bit harder to anticipate. But don’t forget you’ll get an inspection during the homebuying process to give you a better look at the condition of your future house. And with your inspection report in hand, you’ll have a good idea of what needs work. This way, you can start saving up so that you’re ready if and when something breaks.

But even then, if this is something that’s still really nagging at you, talk to your agent about asking the seller to throw in a home warranty. Those can cover repairs for some of the bigger systems in the house, like the HVAC, if they break within a specific time frame. While this isn’t a huge expense for the seller, the likelihood of a seller agreeing to one depends on what’s happening in your local market and how competitive it is right now.

It’s Okay To Stretch – Just Not Too Far

And remember, chances are that money will be a little tight – at least at first. And that’s kind of to be expected. A lot of times when someone buys their first home, they cut down on things like shopping and eating out for a while until they get a better idea of how their expenses will shake out in the new home.

But if you’re crunching the numbers and you won’t have enough money left for things like gas, food, etc. – it’s a sign you’d be stretching yourself too far. The last thing you want is to take on a payment that’s too much to handle. But stretching a little? That’s different. That’s normal.

Your Job Will Probably Change – And That’s Okay

And don’t forget, you’ll likely earn more down the road, so that slight stretch now won’t seem so bad as time wears on. As you advance in your career, you’ll probably start to make more money too. So, as your paycheck grows, the payments will get easier. Renting is a short-term option – and it’s one you deserve to get out of. Buying a home is a long-term play.

And just in case you’re worried about what happens if you do lose your job, you should know there are options, like forbearance, designed to help you temporarily pause payments on your home loan due to hardship.

Bottom Line

Buying your first home is a big decision, and it’s okay to feel a little nervous about it. But if you’re financially ready, don’t let fear keep you from moving forward. These emotions are normal, and great agents help their buyers get through them.

What makes you nervous when you think about buying your first home?

Let’s connect so you have an expert on your side to explain everything along the way.

Do You Know How Much Your Home Is Worth?

Over the past few years, you’ve probably seen a whole lot of headlines about how home prices keep going up. But have you ever stopped to think about what that actually means for your home?

Home prices have risen dramatically over the past five years — far more than usual. And if selling has been on your mind, this could mean a bigger-than-expected payday when you list. So, how much has your home’s value really changed? Let’s break it down.

The Rapid Rise of the Past 5 Years

Typically, home prices go up by about 2-5% a year. But in 2021-2022, there were double-digit increases. And at the peak, prices rose by a staggering 20% or more nationally. Why? There were way more buyers than homes available, which sent prices soaring. While things have normalized since then, you still get to reap the benefits of those massive increases.

Your house has gained way more value than it normally would in such a short period of time – and that means a lot more wealth for you, too.

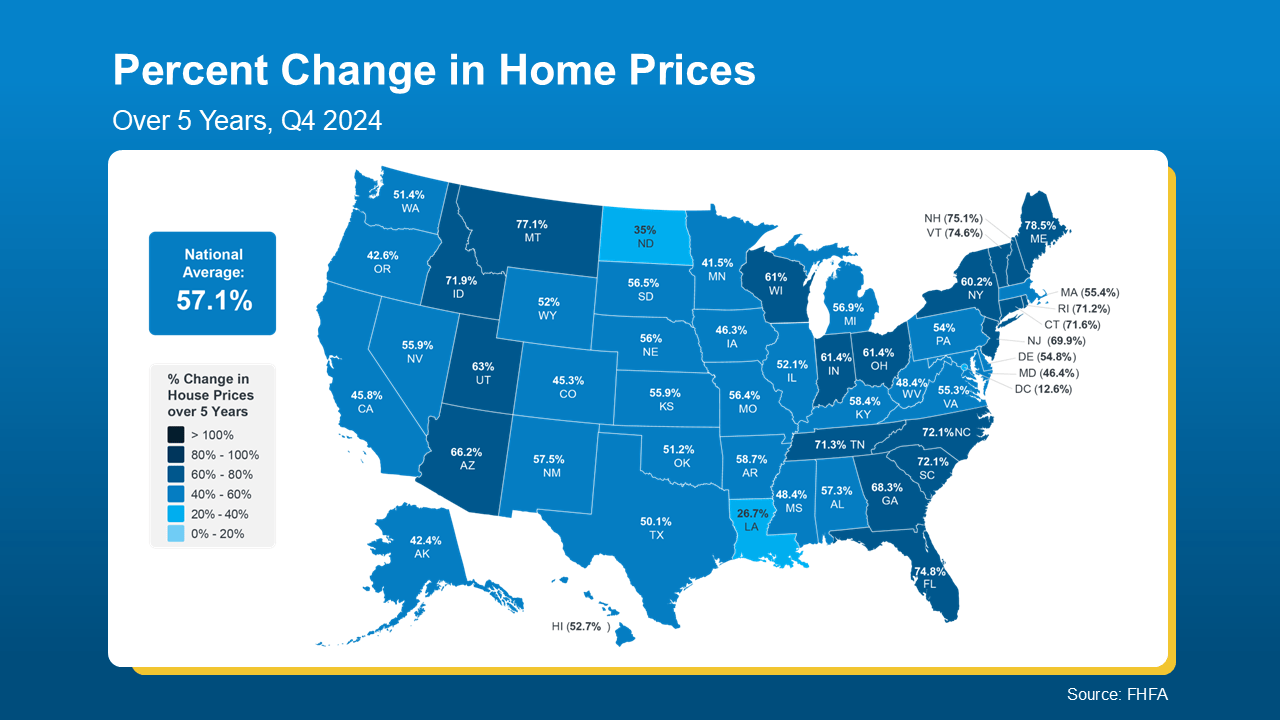

The map below uses data from the Federal Housing Finance Agency (FHFA) to show that, nationally, prices have gone up by nearly 60% in just the past 5 years alone. Here’s a breakdown that takes that one step further and gives you the numbers by state:

If you’ve been holding off on selling because you were worried about buying your next home at today’s rates and prices, let that sink in. It may be more than enough to help close the affordability gap and get you into your next house.

And what if you’ve been there for longer? That means your home’s value is probably even higher now. You get to stack the abnormal gains of the past 5 years on top of five years of more normal appreciation too. And an agent can help you figure out what that really looks like.

How To Find Out What Your House Is Really Worth

While a percentage is great, you probably want more specific numbers.

The only way to get an accurate look at what your house is really worth is to talk to a local real estate agent.

While the map above gives you the average appreciation rate by state, it doesn’t take your local market into consideration. Like, is inventory still low where you live? That may drive prices higher, and faster. Or maybe you’ve done renovation that’ll add even more value to your house. Those are insights you’ll need an agent to provide.

An agent will know what’s happening where you live and can stack that up against the data and the condition of your home to give you the best estimate of its value possible. Only they have the data and expertise to find out your real number today.

Bottom Line

Home values have climbed — maybe more than you expected. Are you curious about what your house is worth in today’s market? Let’s connect so you can find out.

March Eastside Stats

I’m surprised prices are down only 1% month-over-month, as last month’s whopping $1.7M median price seemed like an anomaly. I still think the number is artificially high. Some analysis showed more high-end home selling which is likely skewing the numbers, but it’s not clear. Even with the small dip, there is a staggering 15% year-over-year appreciation. I had previously predicted that we would be at the April 2022 peak (just before interest rates rose) of $1.722M this spring. I’m not sure that will happen, as the stock market volatility has scared away some buyers, and even though we only have 1.5 months of inventory, inventory is growing. Both factors should put downward pressure on pricing, but time will tell.

Is the Housing Market Starting To Balance Out?

For years, sellers have had the upper hand in the housing market. With so few homes for sale and so many people who wanted to purchase them, buyers faced tough competition just to get an offer accepted. But now, inventory is rising, and things are starting to shift in many areas.

So, is the market finally balancing out? And does that mean buyers will have it a bit easier now? Here’s what you need to know.

What Makes It a Buyer’s Market or a Seller’s Market?

It all comes down to how many homes are for sale in an area compared to how many buyers want to buy there. That’s what ultimately determines who has the most leverage.

- A Seller’s Market is when there are more buyers than homes available, so sellers hold the power. This leads to rising prices, multiple offers, and homes selling quickly – often above the asking price – because there isn’t enough to go around.

- A Buyer’s Market is when there are more homes than buyers. In this case, the tables turn. Sellers may have to offer concessions and incentives, or negotiate more to get a deal done. That’s because buyers have more choices and can take their time making decisions.

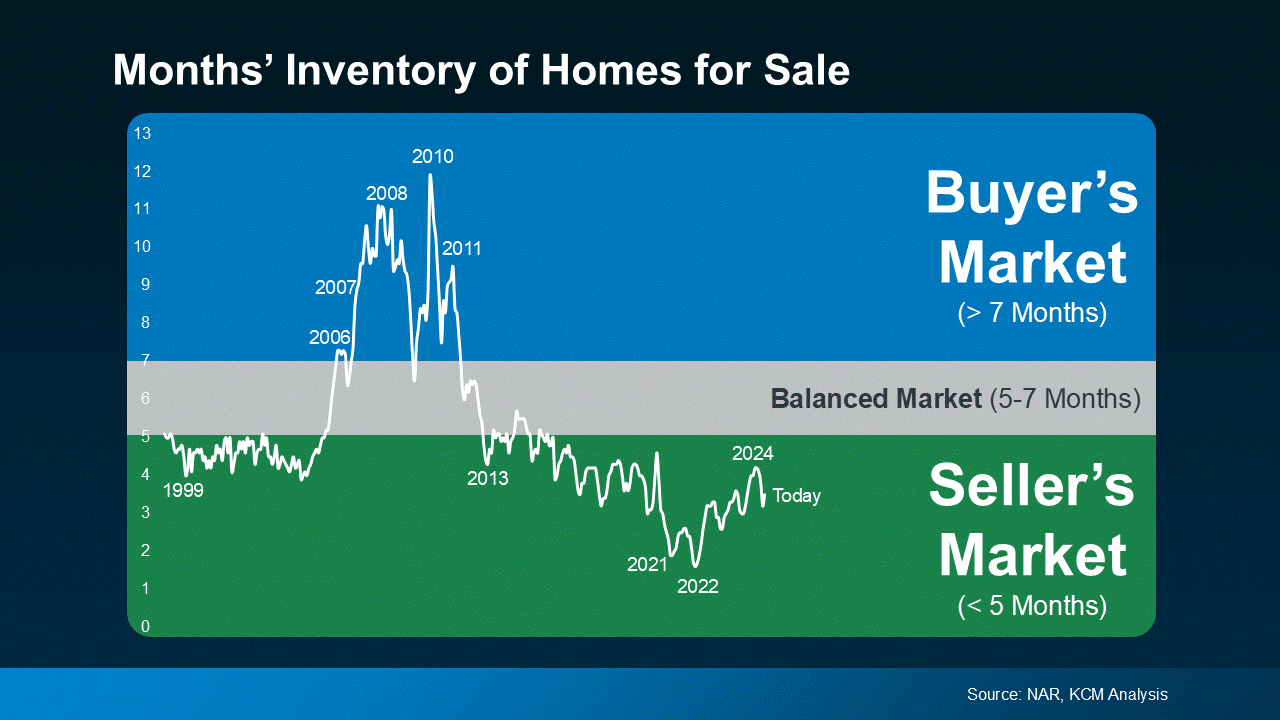

You can see this play out over time using data from the National Association of Realtors (NAR) in the graph below:

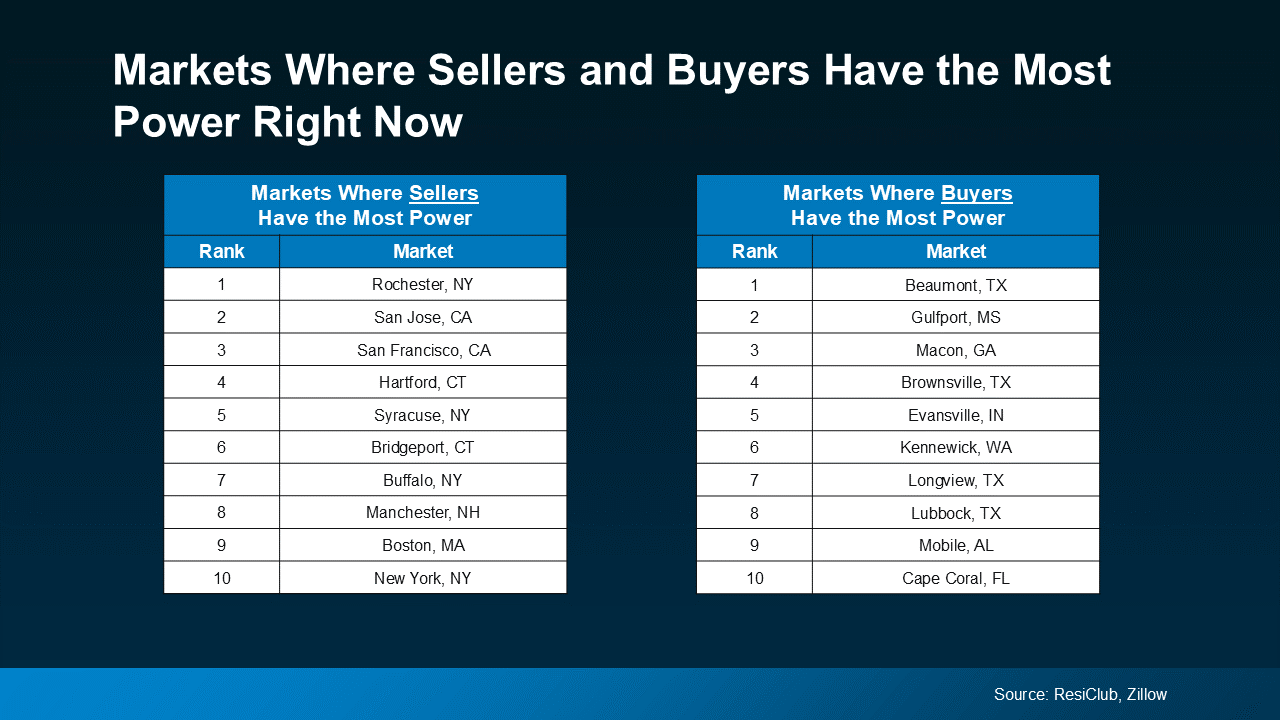

Where the Market Stands Now

While it’s still a seller’s market in many places, buyers in certain locations have more leverage than they’ve had in years. And that’s thanks to how much inventory has grown lately. As Lance Lambert, Co-Founder of ResiClub, explains:

“Among the nation’s 200 largest metro area housing markets, 41 markets ended January 2025 with more active homes for sale than they had in pre-pandemic January 2019. These are the places where homebuyers will be able to find the most leverage or market balance in 2025.”

Here’s a look at some of the strongest seller’s markets and buyer’s markets today, according to that research:

Do you know how to adjust your plans based on who’s got the most negotiating power? Because an agent does.

Clever strategies can make buying in a seller’s market easier – and vice versa. And that’s exactly why you need to hire a pro. A local real estate agent knows their market like the back of their hand. They’re super familiar with what the supply and demand balance looks like and how to help their clients get a deal done either way. So, as long as you have a skilled pro by your side, it doesn’t really matter if your town is on the list or not.

With their expertise, you’ll be able to plan ahead and buy (or sell) no matter what the market looks like.

Bottom Line

With inventory rising, the market may be starting to balance out – but it all depends on where you want to buy or sell.

Are you wondering if buyers or sellers have the upper hand in our area? Let’s connect so you can find out.