Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Are Investors Actually Buying Up All the Homes?

Are you trying to buy a home but you feel like you’re up against deep-pocketed Wall Street investors snatching up everything in sight? Many people believe mega investors are driving up prices and buying up all the homes for sale, and that’s making it hard for regular buyers like you to compete.

But here’s the truth. Investor purchases are actually on the decline, and the big players aren’t nearly as active as you might think. Let’s dive into the facts and put this myth to rest.

Most Investors Are Small, Not Mega Investors

A common misconception is that massive institutional investors are dominating the market. In reality, that’s not the case. The Mortgage Reports explains:

“On average, small investors account for around 18% of the market, while mega investors represent only about 1%.”

Most real estate investors are mom-and-pop investors who own just a few properties — not large corporations buying up entire neighborhoods. They’re people like your neighbors who have another home they’re renting out or a vacation getaway.

Investor Home Purchases Are Dropping

But what about the big investors you hear about in the news? Lately, those institutional investors – the ones that make headlines – have pulled back and aren’t buying as many homes.

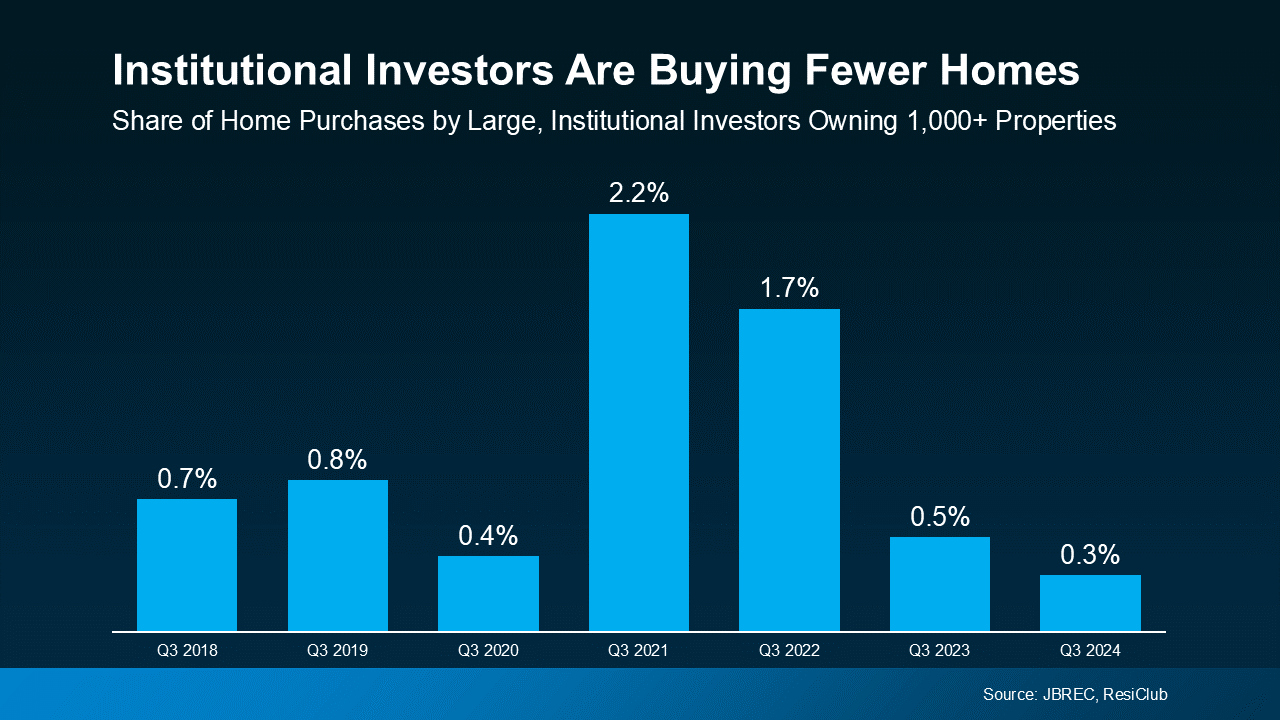

According to John Burns Research and Consulting (JBREC), at their all-time peak in Q2 2022, institutional investors (those owning 1,000+ single-family homes) only made up 2.4% of home sales. And that number has only come down since then. By Q3 2024, that number had fallen to just 0.3% (see graph below):

That’s a major shift, and it means far fewer investors are competing in the market now than just a few years ago.

Investors are clearly more reluctant to buy in today’s market, but why? The answer is largely because higher mortgage rates and home prices have made it less attractive for them.

The idea that Wall Street investors are buying up all the homes and making it impossible for you to compete is a myth. While some investors are still in the market, they’re not nearly as active as they were in past years.

Bottom Line

Big institutional investors aren’t buying up all the homes – if anything they’re buying less than they have been. Let’s connect and talk about what’s happening in our local market. There could be more opportunities than you think.

How does knowing investors are buying fewer homes change the way you see your chances in today’s market?

The Return to Urban Living — Why More People Are Moving Back to Cities

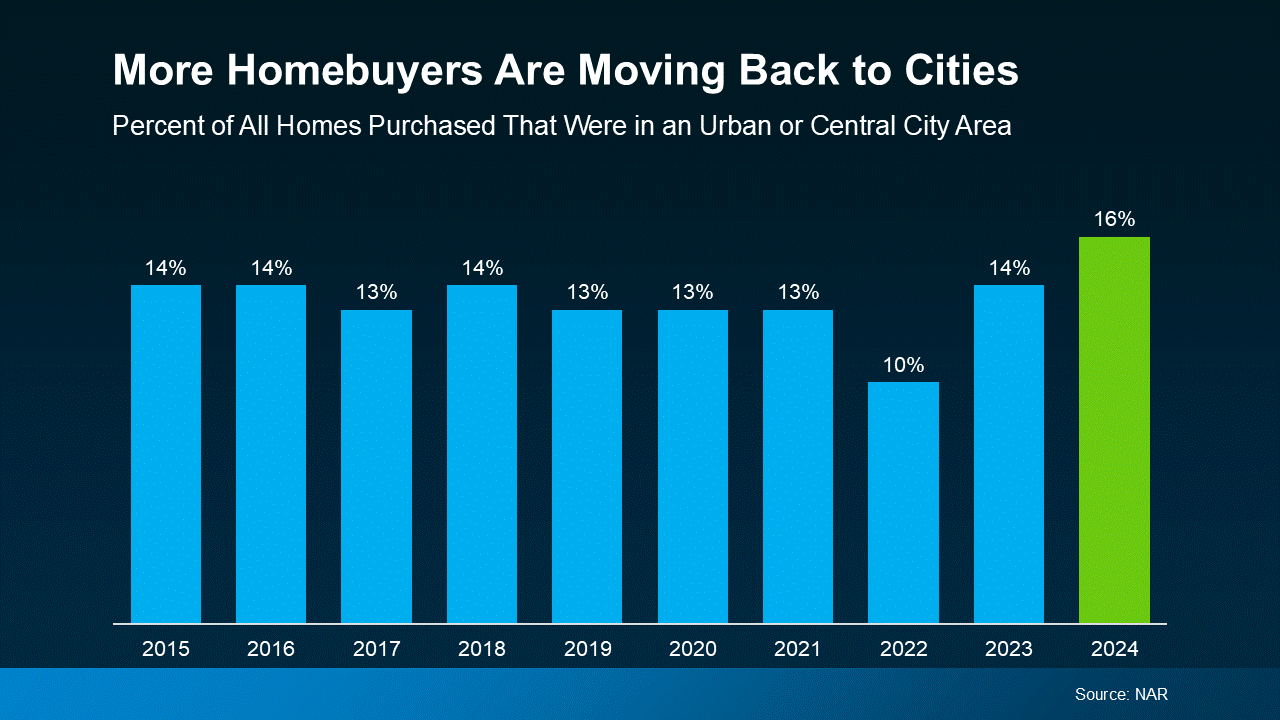

After years of suburban and rural migration during the pandemic, cities have been making a comeback in the past couple of years. According to the National Association of Realtors (NAR), the percentage of people moving to cities has risen to 16%. While that may not sound like a big number to you, it is the highest level in a decade – and that’s a big deal (see graph below):

And data from BrightMLS seems to confirm this trend. In a recent survey, 1 in 5 (20.6%) people looking to buy say they want to live in the city.

So, what’s behind this ongoing shift back to urban living? Let’s break down the top three reasons why people are trading quiet suburbs for bustling cityscapes. You may find out you want to sell your house with a big yard and move to an urban oasis, too.

- Vibrant Culture

Cities have always been hubs of culture, entertainment, and community. They’re packed with energy and there are always endless things to do. During the pandemic, a lot of that excitement was put on pause. But the last couple of years? Cities are buzzing again.

There’s nothing quite like being able to walk to your favorite coffee shop, pop into a local gallery, see a live concert or show, or grab a last-minute dinner at a great spot down the street. It’s a lifestyle that’s easy to love — and one a lot of people want today.

- Being Close to Work

Remote work is still a thing, but most companies are moving to hybrid schedules or even bringing employees back to the office. That makes living closer to work way more convenient. Whether it’s cutting down a long commute or having more chances to network in person, being close to the office is a big plus — especially for industries that thrive on face-to-face connections.

- Easy Access To Everything You Need or Want

One of the best things about living in a city? The convenience. Public transportation, top-notch healthcare, and so much more are all within easy reach. For a lot of people, having everything nearby just makes life easier — and it’s a big reason they’re drawn to urban living.

What To Do If You Want To Move To the City

Let’s say you moved to a suburban area during the pandemic and you’re missing the excitement of living right off city streets. You’re probably thinking: how can I afford to move back into the heart of things with how mortgage rates and home prices are? Here’s how other people are doing it.

According to data from the Federal Housing Finance Agency (FHFA), home values have gone up by 57.4% in the last 5 years alone. And that means your house is probably going to sell for more than you bought it for.

If you already own a home in the suburbs, you may be able to sell that house and use the equity you get back to fuel your move. Sure, you may have to compromise and be happy with a smaller, urban space – but if it’s the lifestyle you’re craving – that trade-off is going to be worth it. To find out what’s possible and what it costs to live in an urban area, lean on a local real estate professional.

Bottom Line

The urban renaissance is real. Whether it’s the vibrant culture, being close to work, or having easy access to everything you need, cities are once again calling — and people are answering.

What’s your favorite thing about life in the city? Let me know.

I’d love to find you a home you love where all the hustle and bustle makes life a bit more exciting.

A Record Percent of Buyers Are Planning To Move in 2025 – Are You?

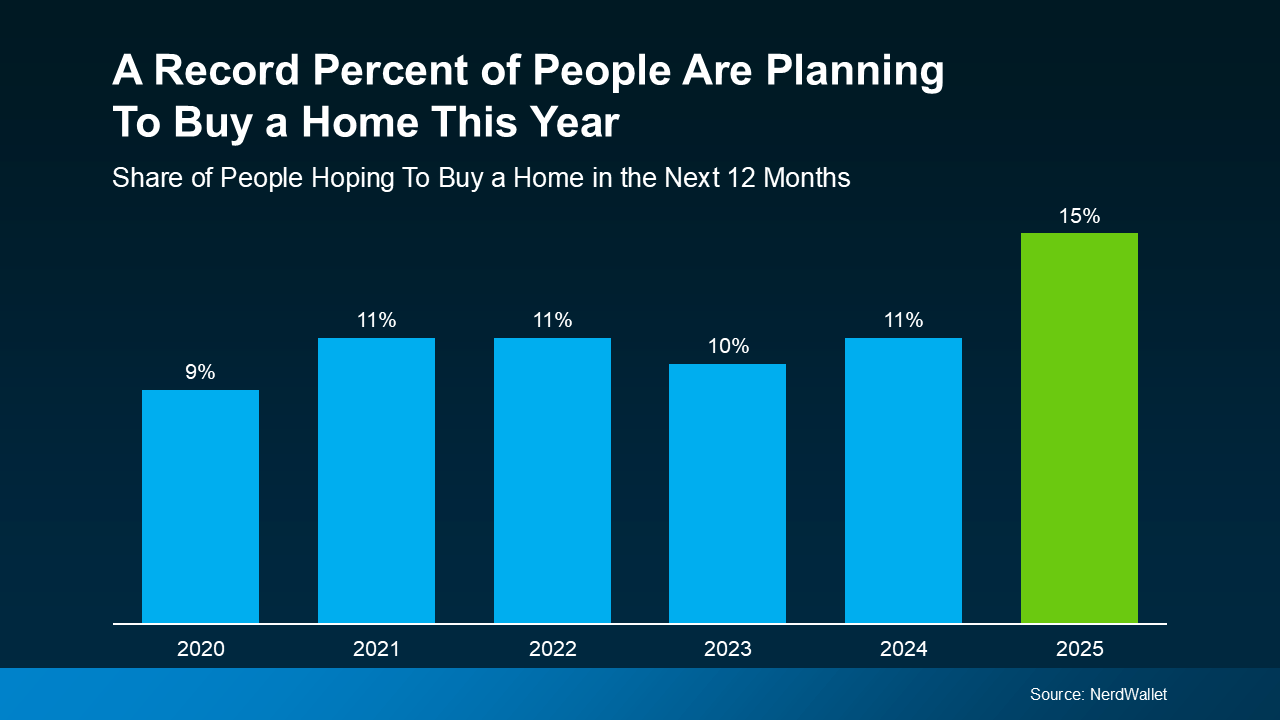

This could be the year to sell your house – and here’s why. According to a recent NerdWallet survey, 15% of people are planning to buy a home this year. That’s actually a record high for this survey (see graph below):

Here’s why this is such a big deal. The percentage has been hovering between 9-11% since 2020. This recent increase shows buyer demand hasn’t disappeared – if anything, it indicates there’s pent-up demand ready to come back to the market.

That doesn’t mean the floodgates are opening and that there’s going to be a huge wave of buyers like we saw a few years ago. But this does signal there’ll be more activity this year than last.

At least some of the buyers who put their plans on hold over the past few years will jump back in. Whether they’re feeling more confident about moving, they’ve finally saved up enough to buy, or they simply can’t wait any longer – this is the year they’re aiming to take the plunge.

And, according to that same NerdWallet survey, more than half (54%) of those potential buyers have already started looking at homes online.

That’s a good indicator that a number of these buyers will be looking during the peak homebuying season this spring. So, if you find the right agent to make sure your house is prepped, priced, and marketed well, you can get your house in front of them.

Bottom Line

More people are going to move this year, and with the right strategy, you can make sure your house is one of the first they look at.

What do you think these buyers will love most about your house?

Let’s talk it over and make sure it’s front and center in your listing.

Eastside February Stats

I hesitated to share this month’s stats, as that median price of $1.7M, an 11% increase, isn’t likely the true story. While it IS the real median number, I’m just not sure it’s telling the true story, as price trends have so many variables and are a tricky, almost impossible, metric to measure. My suspicion is that there were some factors at play that artificially raised this number. Regardless, the market is robust, with 30 percent selling with multiple offers, a median of 6% over the asking price. This week, I have heard of 3 situations where the price went 20% over asking, which is bonkers. That said, when I dove deeper into the data, there were more new listings than this time last year. Couple that with the higher-than-last year inventory we started with, and it would seem things would soften a bit. Months of inventory based on pending sales is around 1.5 months, which is a seller’s market, but if you look at solds, it’s more like 2 months, which is a balanced market. It certainly feels like a sellers’ market. Bottom line, I’m conflicted by the data and not quite sure what to make of it all yet.

The Perks of Buying a Fixer-Upper

There’s no denying affordability is tough right now. But that doesn’t mean you have to put your plans to buy a home on the back burner.

If you’re willing to roll up your sleeves (or hire someone who will), buying a house that needs some work could open the door to homeownership. Here’s everything you need to know so you can decide if this is the right move for you.

What’s a Fixer-Upper?

A fixer-upper is a home that’s livable but requires some renovations. Think cosmetic updates like wallpaper removal and new flooring or more extensive repairs like replacing a roof or updating plumbing.

While fixer-uppers need a little TLC, here’s why they may be worth considering, especially right now:

- They Usually Have a Lower Price Point. Because of the repairs involved, these homes are usually less expensive up front than move-in-ready options. According to a survey from StorageCafe, fixer-uppers come with price tags that are about 29% lower, making them a solid choice if you’re having trouble finding anything in your budget.

- Less Competition. When you’re ready to make an offer, you’re less likely to deal with competition from other buyers who are focused on move-in-ready homes.

- Build Equity Faster. From choosing how to redo the floors to picking which cabinets you want in the kitchen, a fixer-upper allows you to design a space that fits your needs and style. And with smart renovations, you can increase your home’s value faster and potentially see a big return on your investment.

As The Mortgage Reports notes:

“If you’re a house hunter who’s not afraid of sweat equity, buying a fixer-upper could be your ticket to homeownership. Doing so could lead to big savings, even in some of the nation’s largest and most popular housing markets. Plus, adding the right features could help your investment.”

What To Know About Buying a Fixer-Upper

The possibilities that come with a fixer-upper are exciting, but there are a few things to think about first.

- Do You Have a Gameplan? Consider if you have the time, skills, or budget to tackle renovations. Be honest about what you can handle yourself, what you’ll need to hire out, and if a fixer-upper is truly a good fit for your lifestyle. Remember, you’ll likely be living in a construction zone at least for a little while.

- Prioritize the Repairs and Upgrades: Don’t stress yourself out thinking you’ve got to do all the work up front. Space out renovations over time in a way that makes sense for your budget and what’s most important to tackle first.

- Location Matters: You want the money you’re spending to fix up a house to be worth the investment. So, make sure the home is in an area with increasing home values and amenities locals love, like parks and restaurants.

- Get a Home Inspection: Hiring an inspector to do a thorough inspection before you buy is a must. What they find will help you understand what needs to be updated, renovation costs, and if it’s a project you want to take on.

- Budget for Surprises: Renovations rarely go as planned. So, be sure to set aside extra money to cover things like extended repair timelines, an increase in the cost of materials, or other unknowns that may come up.

Talk to a Lender About Financing Options: There are some renovation mortgages designed for homes that need a little work. But they may have requirements like spending and timeline limits, so talk to a trusted lender to understand the fine print.

Bottom Line

Fixer-uppers aren’t for everyone, but if you’re open to doing a bit of work, they can be a great way to overcome today’s affordability hurdles and find something in your budget.

With the right mindset and careful planning, you could turn a less-than-perfect house into the perfect home for you.

If you found a fixer-upper that fits your budget and goals, would you consider taking the plunge? If so, let’s connect to explore what’s out there.