Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

One of the biggest reasons buyers are still sitting on the sidelines is because they think home prices are going to come down.

- Some believe a crash is coming and they’ll get a better deal if they hold off.

- Others worry they’ll buy now and watch their home’s value fall later.

And nobody wants to overpay or buy right before values drop. But here’s the question worth asking:

What if the crash you’re waiting for isn’t actually coming?

Because that’s what the latest data suggests.

Experts Are Not Calling for a Crash

If you’ve spent any time online lately, you’ve seen posts claiming home prices are about to come crashing down. And it’s true that some markets are seeing small price declines right now.

But that’s not the same thing as a nationwide crash.

While some places are going through a price adjustment, Realtor.com data shows home prices are still rising in 71% of housing markets across the country.

The trouble is, since negative news sells, you’re seeing more coverage about how a handful of markets are seeing declines, than how the majority are still seeing prices rise. And that’s unfortunate.

It’s exactly why a lot of buyers end up with the impression that prices are falling everywhere when they’re not. So how do you really know where prices are really headed from here?

That’s where the Home Price Expectations Survey (HPES) from Fannie Mae comes in.

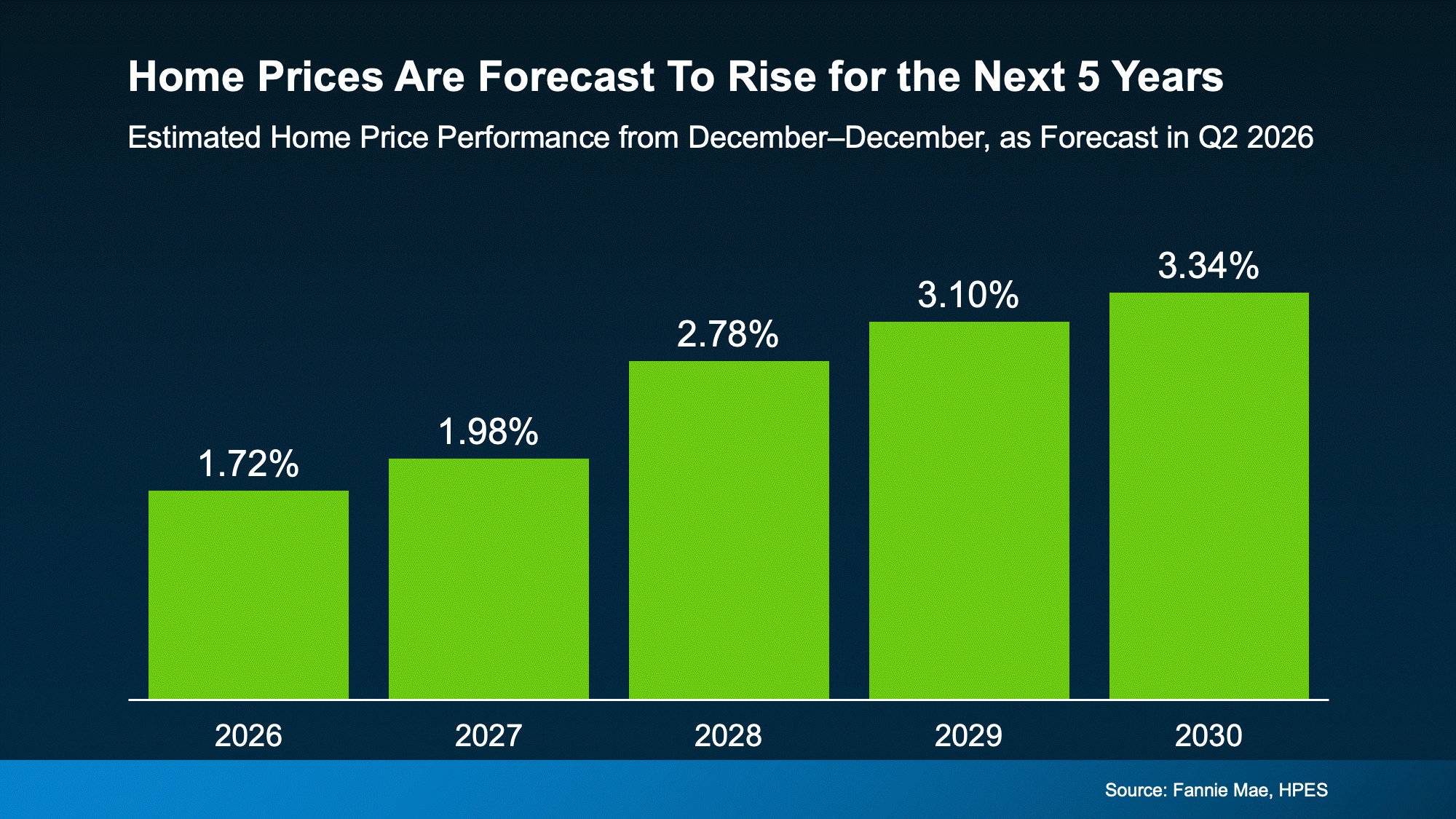

Home Prices Will Rise for the Next 5 Years

Every quarter, more than 100 economists, housing experts, and market analysts are asked where they think home prices are headed based on the latest data available.

And despite all the uncertainty in today’s market, there’s one thing they largely agreed on:

They don’t think a crash is coming.

In fact, the average of all of their forecasts calls for home prices to rise every year for at least the next 5 years (see graph below):

The point is that the overwhelming expectation isn’t for prices to fall. It’s for prices to rise at a more normal pace. And just in case you’re looking at the forecasts and saying: “of course they’d say that” – know that this survey doesn’t just include optimists. It includes pessimists too.

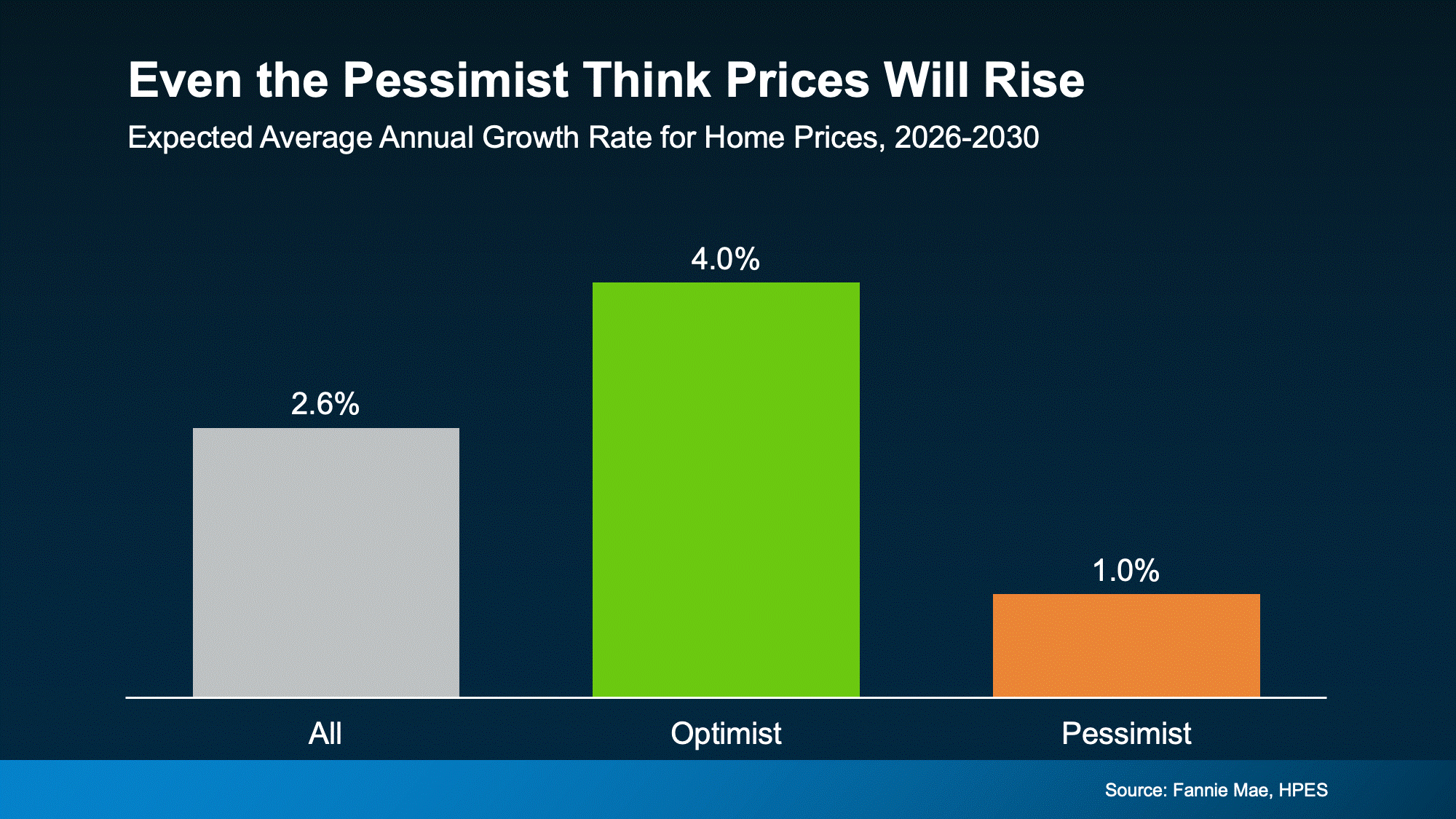

Even the Pessimists Aren’t Predicting a Crash

Researchers broke the panel into groups based on how bullish or bearish they were about housing. The result? Even the most pessimistic group still expects home prices to climb over the next five years.

Optimists think we’ll see prices go up roughly 4% a year. Pessimists say it’ll be closer to 1%. The reality may be somewhere in the middle.

Think about that for a second. The debate among experts isn’t whether prices will crash. It’s how much they’ll rise.

That’s a very different conversation than the one happening across social media.

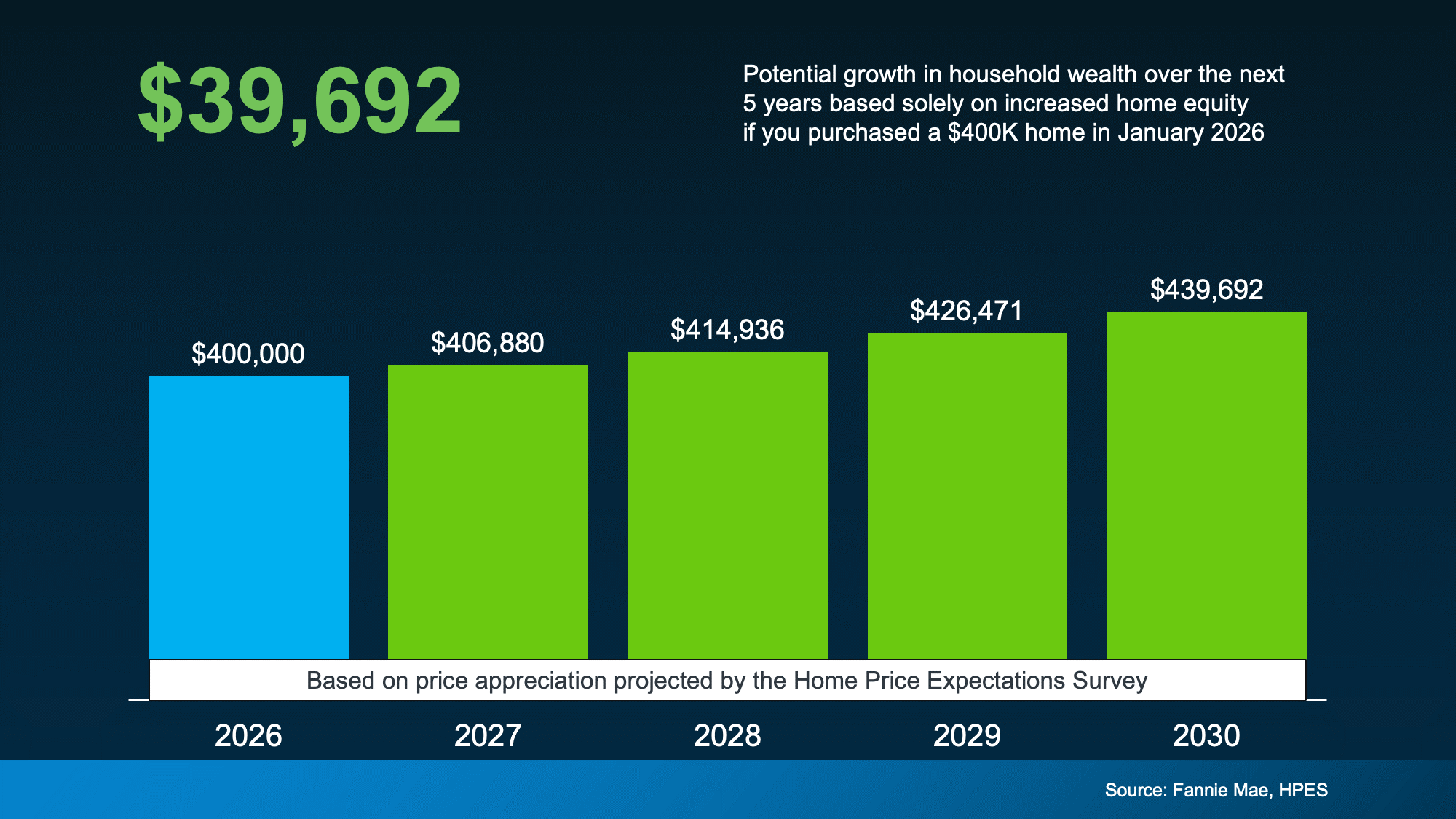

This Means Waiting Could Actually Cost You

So, if you’re putting off your move until prices come down, you may be disappointed. According to the experts, a widespread crash isn’t in the cards.

In fact, based on the HPES forecast, a buyer who purchased a $400,000 home this January would gain nearly $40,000 in equity over the next five years from appreciation alone, even in this more moderate market (see below):

Of course, this all depends on local market conditions. This forecast is a national average. But broadly speaking, if the experts are right, the bigger risk isn’t that prices will crash. It may be waiting for a crash that never comes.

Because depending on your market, if you wait, you could be missing out on $40k in equity or paying 40k more in 5 years for the same house.

Bottom Line

A lot of buyers are waiting because they think prices will fall, but that’s not what the experts are saying.

If you’re trying to decide whether waiting still makes sense, let’s connect. That way you understand what’s happening in our local market and what it could mean for your plans.