Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

While I’m away I thought I would reshare this Capital Gains discussion with my accountant. Enjoy!

Home Knowledge • Market Advice •

February 6, 2024

3 Must-Do’s When Selling Your House in 2024

If one of the goals on your list is selling your house and making a move this year, you’re likely juggling a mix of excitement about what’s ahead and feeling a little sentimental about your current home.

A great way to balance those emotions and make sure you’re confident in your decision is to keep these three best practices in mind when you’re ready to sell.

1. Price Your Home Right

The housing market shifted in 2023 as mortgage rates rose and home price appreciation started to normalize once again. As a seller, you still need to recognize how important it is to price your house appropriately based on where the market is today. Hannah Jones, Economic Research Analyst for Realtor.com, explains:

“Sellers need to become familiar with their local market and work closely with a local agent to make sure their listing is attractive to buyers. Buyers feeling the pressure of affordability are likely to be pickier, so a well-priced, well-maintained home is the ticket to drumming up big demand.”

If you price your house too high, you run the risk of deterring buyers. And if you go too low, you’re leaving money on the table. An experienced real estate agent can help determine what your ideal asking price should be, so your house moves quickly and for top dollar.

2. Keep Your Emotions in Check

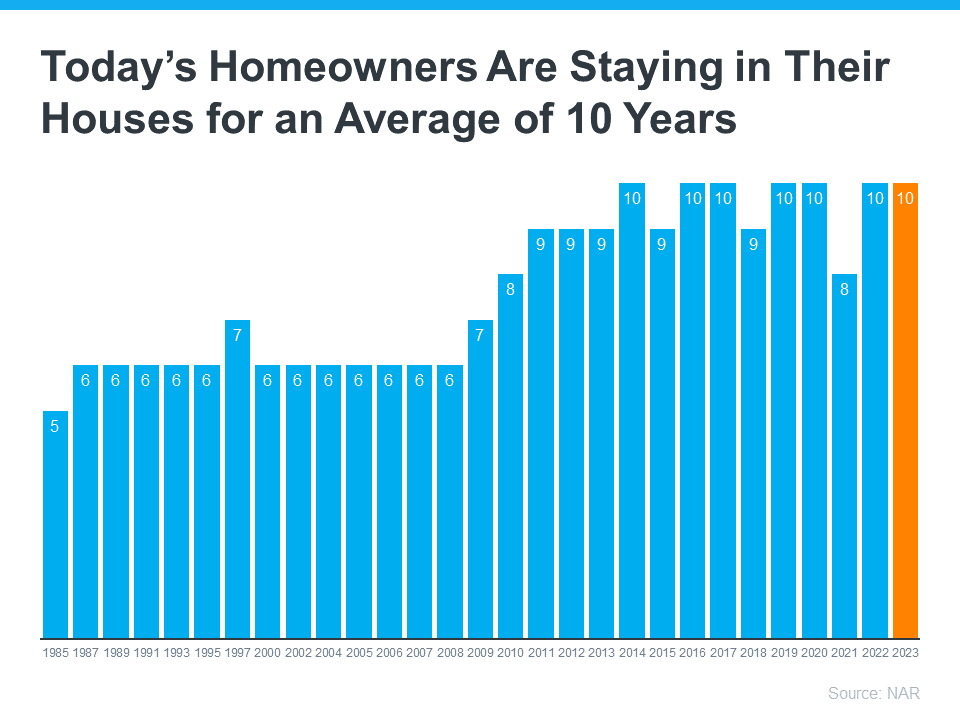

Today, homeowners are staying in their houses longer than they used to. According to the National Association of Realtors (NAR), since 1985, the average time a homeowner has owned their home has increased from 6 to 10 years (see graph below):

This is much more than what used to be the norm. The side effect, however, is when you stay in one place for so long, you may get even more emotionally attached to your space. If it’s the first home you bought or the house where your loved ones grew up, it very likely means something extra special to you. Every room has memories, and it’s hard to detach from the sentimental value.

For some homeowners, that makes it even tougher to separate the emotional value of the house from fair market price. That’s why you need a real estate professional to help you with the negotiations and the best pricing strategy along the way. Trust the professionals who have your best interests in mind.

3. Stage Your Home Properly

While you may love your decor and how you’ve customized your house over the years, not all buyers will feel the same way about your vibe. That’s why it’s so important to make sure you focus on your home’s first impression, so it appeals to as many buyers as possible.

Buyers want to be able to picture themselves in the home. They need to see themselves inside with their furniture and keepsakes – not your pictures and decorations. As Jessica Lautz, Deputy Chief Economist and Vice President of Research at NAR, says:

“Buyers want to easily envision themselves within a new home and home staging is a way to showcase the property in its best light.”

A real estate professional can help you with expertise on getting your house ready to sell.

Bottom Line

If you’re considering selling your house, let’s connect so you have help navigating the process while prioritizing these must-do’s.

Market Advice • Real Estate Forecast •

January 30, 2024

Experts Project Home Prices Will Increase in 2024

Even though home prices are going up nationally, some people are still worried they might come down. In fact, a recent survey from Fannie Mae found that 24% of people think home prices will actually decline over the next 12 months. That means almost one out of every four people are dealing with that fear, and you might be, too.

To help ease that concern, here’s what experts forecast will happen with prices this year.

Experts Project a Modest Increase

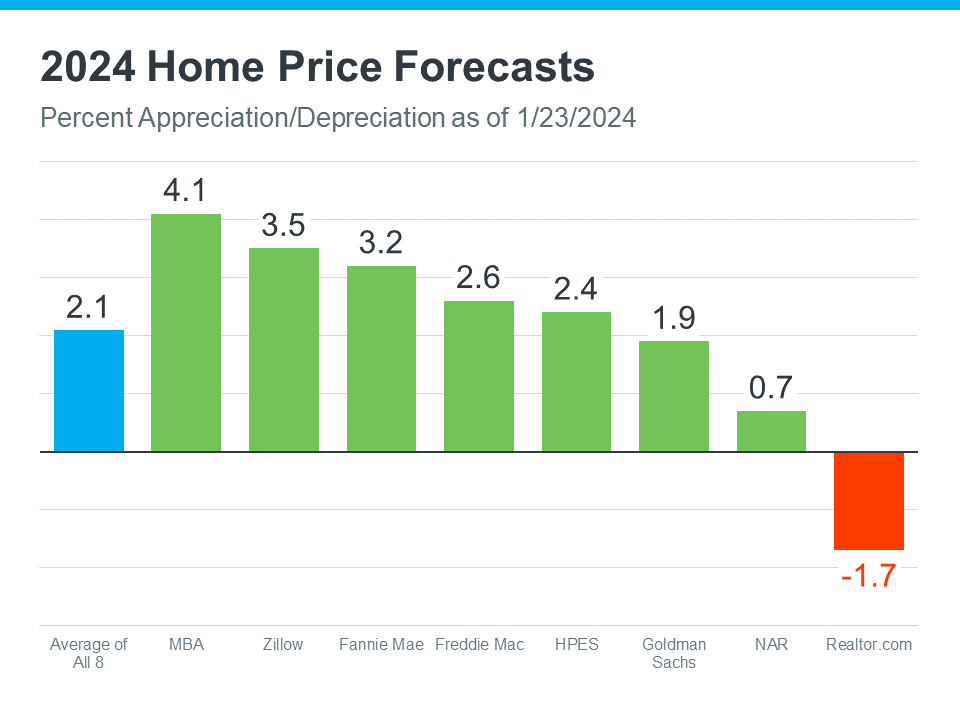

Check out the latest home price forecasts from eight different sources (see graph below):

The blue bar on the left means, on average, experts think home prices will go up over 2% by the end of this year – not down.

Prices aren’t likely to depreciate in 2024 because inventory is still tight and lower mortgage rates are leading to strong buyer demand. Those two factors will keep pushing prices up as the year goes on. As Selma Hepp, Chief Economist at CoreLogic, explains:

“With mortgage rates dropping, demand for homes in early 2024 is likely to be strong and will again put pressure on prices, similar to trends observed in early 2023 . . . Most markets will continue to reach new home price highs over the course of 2024.”

What Does This Mean for You?

Experts are saying home prices will go up this year, and that’s good news if you’re thinking about buying a home. When you become a homeowner, you want the value of your house to go up. That appreciation is what builds equity and makes homeownership such a good investment over time.

Beyond that, expected home price appreciation also means if you’re ready, willing, and able to buy, waiting just means it will cost more later.

Bottom Line

If you’re worried home prices will come down, don’t be. Many experts believe they’ll actually go up this year. If you have questions or worries about what’s happening with prices in our area, let’s connect.

Home Knowledge • Market Advice • Real Estate Forecast •

January 23, 2024

3 Key Factors Affecting Home Affordability

Over the past year, a lot of people have been talking about housing affordability and how tight it’s gotten. But just recently, there’s been a little bit of relief on that front. Mortgage rates have gone down since their most recent peak in October. But there’s more to being able to afford a home than just mortgage rates.

To really understand home affordability, you need to look at the combination of three important factors: mortgage rates, home prices, and wages. Let’s dive into the latest data on each one to see why affordability is improving.

1. Mortgage Rates

Mortgage rates have come down in recent months. And looking forward, most experts expect them to decline further over the course of the year. Jiayi Xu, an economist at Realtor.com, explains:

“While there could be some fluctuations in the path forward … the general expectation is that mortgage rates will continue to trend downward, as long as the economy continues to see progress on inflation.”

And even a small change in mortgage rates can have a big impact on your purchasing power, making it easier for you to afford the home you want by reducing your monthly mortgage payment.

2. Home Prices

The second important factor is home prices. After going up at a relatively normal pace last year, they’re expected to continue rising moderately in 2024. That’s because even with inventory projected to grow slightly this year, there still aren’t enough homes for sale for all the people who want to buy them. According to Lisa Sturtevant, Chief Economist at Bright MLS:

“More inventory will be generally offset by more buyers in the market. As a result, it is expected that, overall, the median home price in the U.S. will grow modestly . . .”

That’s great news for you because it means prices aren’t likely to skyrocket like they did during the pandemic. But it also means it’ll probably cost you more to wait. So, if you’re ready, willing, and able to buy, and you can find the right home, purchasing before more buyers enter the market and prices rise further might be in your best interest.

3. Wages

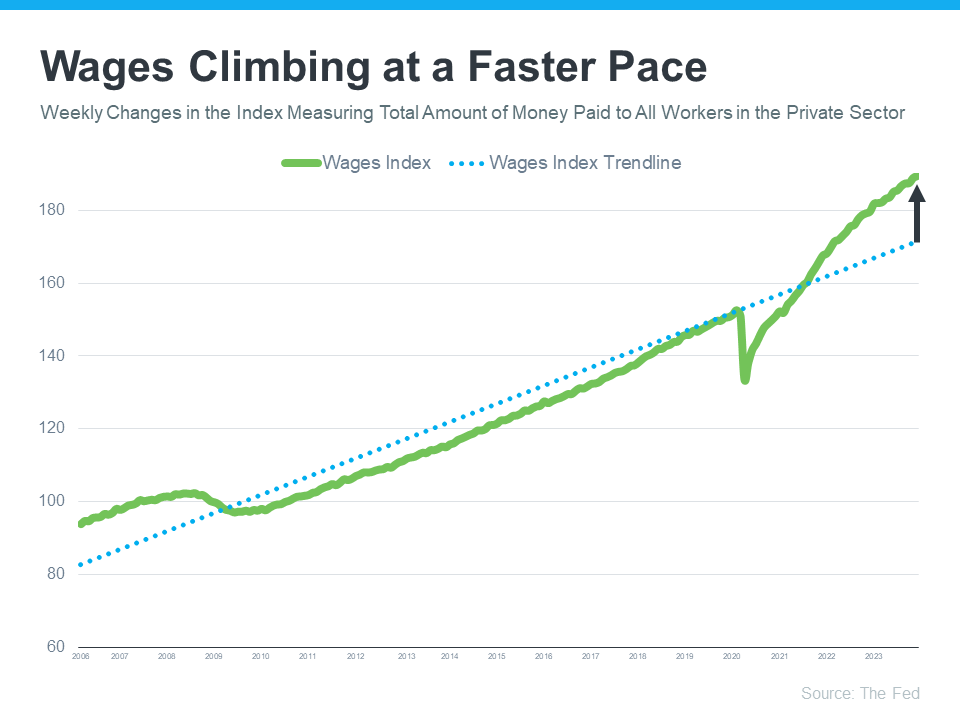

Another positive factor in affordability right now is rising income. The graph below uses data from the Federal Reserve to show how wages have grown over time:

If you look at the blue dotted trendline, you can see the rate at which wages typically rise. But on the right side of the graph, wages are above the trend line today, meaning they’re going up at a higher rate than normal.

Higher wages improve affordability because they reduce the percentage of your income it takes to pay your mortgage. That’s because you don’t have to put as much of your paycheck toward your monthly housing cost.

What This Means for You

Home affordability depends on three things: mortgage rates, home prices, and wages. The good news is, they’re moving in a positive direction for buyers overall.

Bottom Line

If you’re thinking about buying a home, it’s important to know the main factors impacting affordability are improving. To get the latest updates on each, let’s connect.

Home Knowledge • Market Advice • Real Estate Forecast •

January 16, 2024

Homeownership Is Still at the Heart of the American Dream

Buying a home is a powerful decision, and it remains at the heart of the American Dream. Unlike renting, owning a home means more than just having a place to live – it offers a sense of belonging, stability, and freedom. According to Nicole Bachaud, Senior Economist at Zillow:

“The American Dream is still owning a home. There’s a lot of pent-up demand for ownership; that isn’t going to go away.”

Let’s explore just a few of the reasons why so many Americans continue to value homeownership.

The Financial Benefits of Owning a Home

One possible reason homeownership is viewed so highly is because owning a home is a significant wealth-building tool. That may be why Jessica Lautz, Deputy Chief and VP of Research at the National Association of Realtors (NAR), says:

“Homeownership is the number one way to build wealth in America.”

Over time, owning a home not only helps boost your own net worth, but it also sets future generations up for success as you pass that wealth down. Habitat for Humanity explains:

“Overall, homeownership promotes wealth building by acting as a forced savings mechanism and through home value appreciation. Homeowners make monthly payments that increase their equity in their homes by paying down the principal balance of their mortgage. . . . In addition, owning a home promotes intergenerational homeownership and wealth building. Children of homeowners transition to homeownership earlier — lengthening the period over which they can accumulate wealth . . .”

It can also provide meaningful financial stability compared to renting. When you buy with a fixed-rate mortgage, you can lock in your monthly housing payments for the length of your home loan.

The Non-Financial Benefits of Homeownership

But, owning a home offers more than just financial benefits—it benefits you socially and emotionally too. Your home provides feelings of achievement, responsibility, and more. In a recent survey, Fannie Mae outlines just a few of these more emotionally-driven benefits, including:

“The top three were having control over what you do with your living space (94%) to having a sense of privacy and security (91%) and having a good place for your family or to raise your children (90%) . . .”

What Does That Mean for You?

If your idea of the American Dream involves greater freedom, security, and prosperity, homeownership could be a key player in bringing that dream to life. And with mortgage rates now on a downward trend, it might be a good time for you to consider making a move.

If you’re ready and able to buy, know that there are incredible benefits waiting at the end of your journey. You’ll gain more than just a home – it’s a place to grow your wealth and call your very own. Like Ksenia Potapov, Economist at First American says:

“…homeownership remains an important driver of wealth accumulation and the largest source of total wealth among most households.”

Bottom Line

Buying a home is a powerful decision and the cornerstone of the American Dream. If finding a place to call your own is part of your dream for this year, let’s connect to start the process today.

Market Advice • Real Estate Forecast •

January 12, 2024

January 2024 Eastside Market Update

December is always a squirrelly month and not a great month to glean much from the data. The stats in the video are interesting, 11% year-over-year appreciation (though not quite to the peak of 2022) and 1.2 months of inventory illustrate a healthy, dare I say robust, market. What is more interesting is the that we ended the year with 43% less inventory than 2022, which performed like a ‘normal/pre-pandemic’ year with the bulk of the appreciation happen in the first part of the year. Also interesting is that December had more pending sales than new listings showing that buyers are out there. Another noteworthy point when comparing last year to this year is that interest rates are about the same (~6.46% last year vs ~6.62% today). I am cautiously optimistic that the first quarter will be strong. For buyers this means buy with courage and confidence. For sellers it means you should list with confidence.

Market Advice • Real Estate Forecast • Video Blogs •

January 11, 2024

Weekly update – January 10th

This week I talk about stats. Inventory is low and interest rates are lower than they have been. Should be a recipe for price appreciation.

Home Knowledge • Market Advice • Real Estate Forecast •

January 9, 2024

Thinking About Buying a Home? Ask Yourself These Questions

If you’re thinking of buying a home this year, you’re probably paying closer attention than normal to the housing market. And you’re getting your information from a variety of channels: the news, social media, your real estate agent, conversations with friends and loved ones, the list goes on and on. Most likely, home prices and mortgage rates are coming up a lot.

Here are the top two questions you need to ask yourself as you make your decision, including the data that helps cut through the noise.

1. Where Do I Think Home Prices Are Heading?

One reliable place you can turn to for information on home price forecasts is the Home Price Expectations Survey from Fannie Mae – a survey of over one hundred economists, real estate experts, and investment and market strategists.

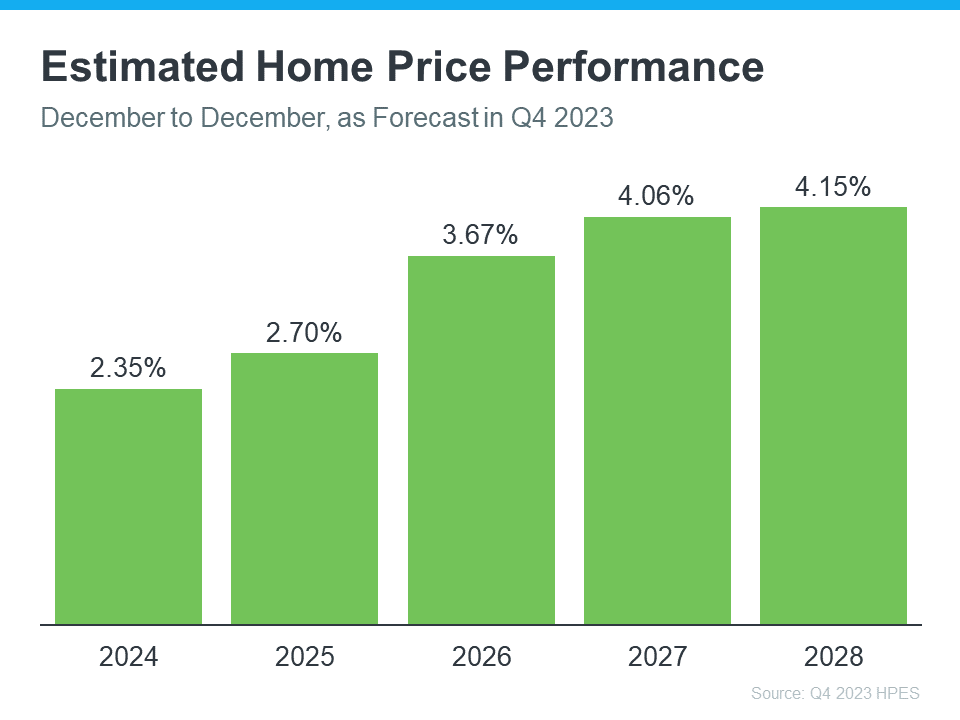

According to the most recent release, the experts are projecting home prices will continue to rise at least through 2028 (see the graph below):

So, why does this matter to you? While the percent of appreciation may not be as high as it was in recent years, what’s important to focus on is that this survey says we’ll see prices rise, not fall, for at least the next 5 years.

And home prices rising, even at a more moderate pace, is good news not just for the market, but for you too. It means, by buying now, your home will likely grow in value, and you should gain home equity in the years ahead. But, if you wait, based on these forecasts, the home will only cost you more later on.

2. Where Do I Think Mortgage Rates Are Heading?

Over the past year, mortgage rates spiked up in response to economic uncertainty, inflation, and more. But there’s an encouraging sign for the market and mortgage rates. Inflation is moderating, and here’s why this is such a big deal if you’re looking to buy a home.

When inflation cools, mortgage rates generally fall in response. That’s exactly what we’ve seen in recent weeks. And, now that the Federal Reserve has signaled they’re pausing their Federal Funds Rate increases and may even cut rates in 2024, experts are even more confident we’ll see mortgage rates come down.

Danielle Hale, Chief Economist at Realtor.com, explains:

“. . . mortgage rates will continue to ease in 2024 as inflation improves and Fed rate cuts get closer. . . . a key factor in starting to provide affordability relief to homebuyers.”

As an article from the National Association of Realtors (NAR) says:

“Mortgage rates likely have peaked and are now falling from their recent high of nearly 8%. . . . This likely will improve housing affordability and entice more home buyers to return to the market . . .”

No one can say with absolute certainty where mortgage rates will go from here. But the recent decline and the latest decision from the Federal Reserve to stop their rate increases, signals there’s hope on the horizon. While we may see some volatility here and there, affordability should improve as rates continue to ease.

Bottom Line

If you’re thinking about buying a home, you need to know what’s expected with home prices and mortgage rates. While no one can say for certain where they’ll go, making sure you have the latest information can help you make an informed decision. Let’s connect so you can stay up to date on what’s happening and why this is such good news for you.