Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Sell Your House During the Winter Sweet Spot

A lot of people assume spring is the ideal time to sell a house. And sure, buyer demand usually picks up at that time of year. But here’s the catch: so does your competition because a lot of people put their homes on the market at the same time.

So, what’s the real advantage of selling your house before spring? It’ll stand out.

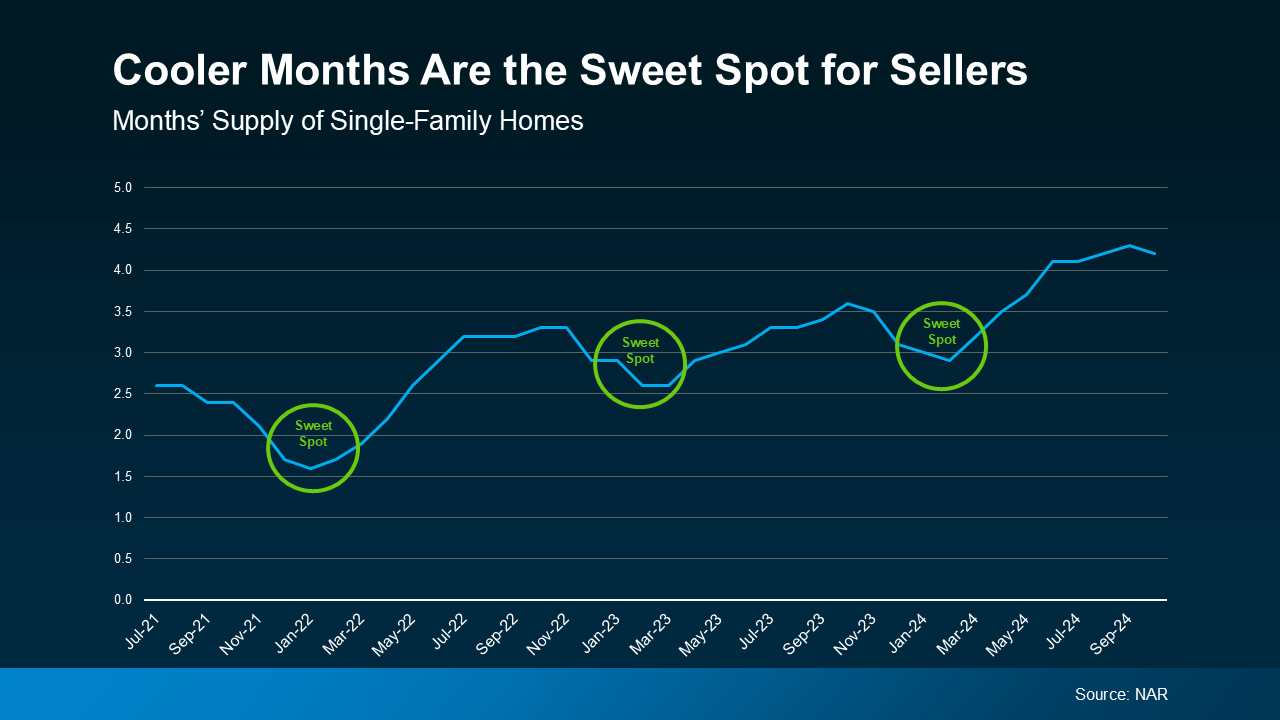

Historically, the number of homes for sale tends to drop during the cooler months – and that means buyers have fewer options to choose from.

You can see how that trend played out over the past few years in this data from the National Association of Realtors (NAR). Each time, the supply of homes for sale dipped during these cooler months. And then, after each winter lull, inventory started to climb as more sellers jumped into the market closer to spring (see graph below):

Here’s why knowing how this trend works gives you an edge. While inventory is higher this year than it‘s been in the last few winters, if you work with an agent to list now, it’ll still be in this year’s sweet spot. So, while other sellers are taking their homes off the market, you can sell before the spring wave of new listings hits, and your house will have a better chance of standing out.

Why wait until spring when you can get ahead of the curve now?

Fewer Listings Also Means More Eyes on Your Home

Another big perk of selling in the winter? The buyers who are looking right now are serious about making a move.

During this season, the window-shopper crowd tends to stay busy with other things, like holiday celebrations, and avoids looking for homes when the weather’s cooler. So, the buyers out looking aren’t casually browsing—they’re motivated, whether it’s because of a job relocation, a lease ending, or some other time-sensitive reason. And those are the types of buyers you want to work with. Investopedia explains:

“. . . if your house is up for sale in the winter and someone is looking at it, chances are that person is serious and ready to buy.”

Bottom Line

With less competition and serious buyers on the hunt, you’ll be in a great position to sell your house this winter. Let’s connect if you’re ready to get the process started.

Why More Sellers Are Hiring Real Estate Agents

Putting your house for sale on your own – often called “For Sale by Owner” or FSBO – might be on your mind. But you should know that it gets complicated very quickly, especially in today’s complex market.

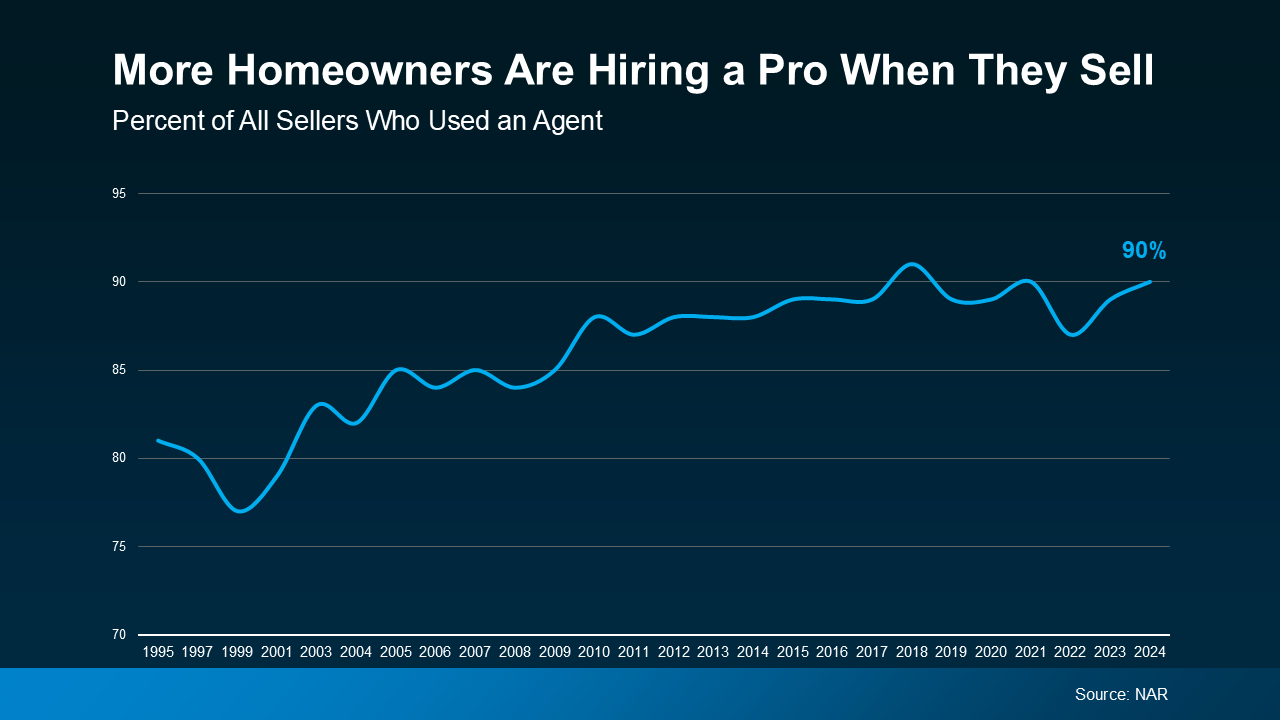

That’s why data from the National Association of Realtors (NAR) shows a record low number are going the route of selling on their own.

Instead, more and more homeowners are choosing to work with a real estate agent (see graph below):

And here’s why partnering with an expert is the go-to choice. Selling your home is a big deal, and while FSBO might seem like a way to save time or money, it comes with a lot of responsibilities.

The selling process requires setting the right price, navigating a growing amount of legal paperwork, and creating a solid strategy to attract buyers. And going it alone often means taking on more than you bargained for.

Let’s look at two big reasons why working with a pro can make all the difference.

- Getting the Price Right

One of the biggest hurdles when selling a house on your own is figuring out the right price. It’s not as simple as picking a number that sounds good – you need to hit the bullseye. Price your home too high, and buyers may overlook your listing. Price it too low, and you could leave money on the table or even raise red flags about the condition of your home.

Real estate agents are experts in finding the right price for today’s market trends. As Zillow explains:

“Agents are pros when it comes to pricing properties and have their finger on the pulse of your local market. They understand current buying trends and can provide insight into how your home compares to others for sale nearby.”

With their knowledge of the local market, buyer behavior, and what homes like yours are selling for, an agent will help you make sure you set a price that’s competitive and that’ll draw in buyers. And it’s that perfectly strategic price that’ll set the stage for selling at top dollar.

- Understanding and Managing the Paperwork

Another part of the process is dealing with a growing stack of paperwork, from disclosure forms to contracts. Each document needs to be completed accurately, and there are legal requirements to follow that can feel overwhelming if you’re not familiar with them.

This is another area where an agent’s expertise really shines. They’ve handled these documents countless times and know exactly what’s needed to keep everything on track. Your agent will guide you through the paperwork step by step, making sure it’s done right the first time and you understand what you’re signing. With their help, you can avoid unnecessary stress and mistakes that can lead to delays, legal complications, and more.

Bottom Line

Selling your house is a big decision, and having a trusted real estate agent on your side can make all the difference.

Let’s connect so you have a pro to help with everything from pricing your home to managing the details. That way we can take the guesswork out of the process and help you sell with confidence.

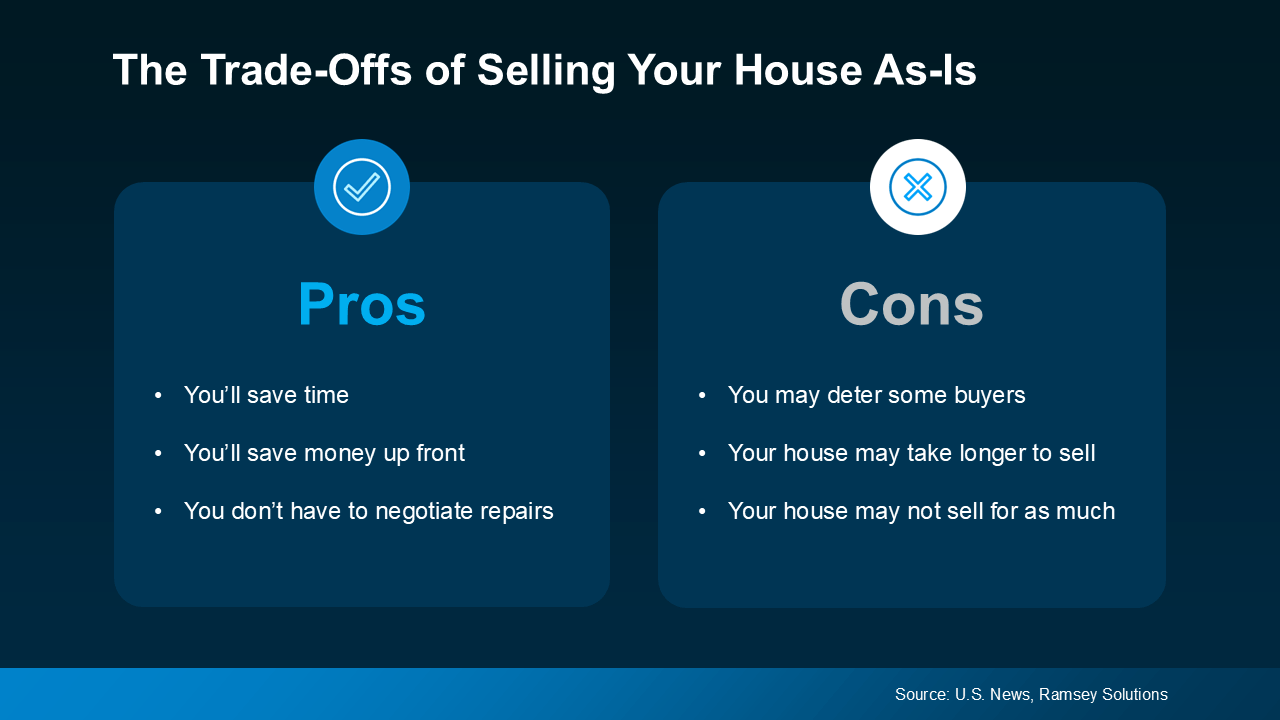

Should You Sell Your House As-Is or Make Repairs?

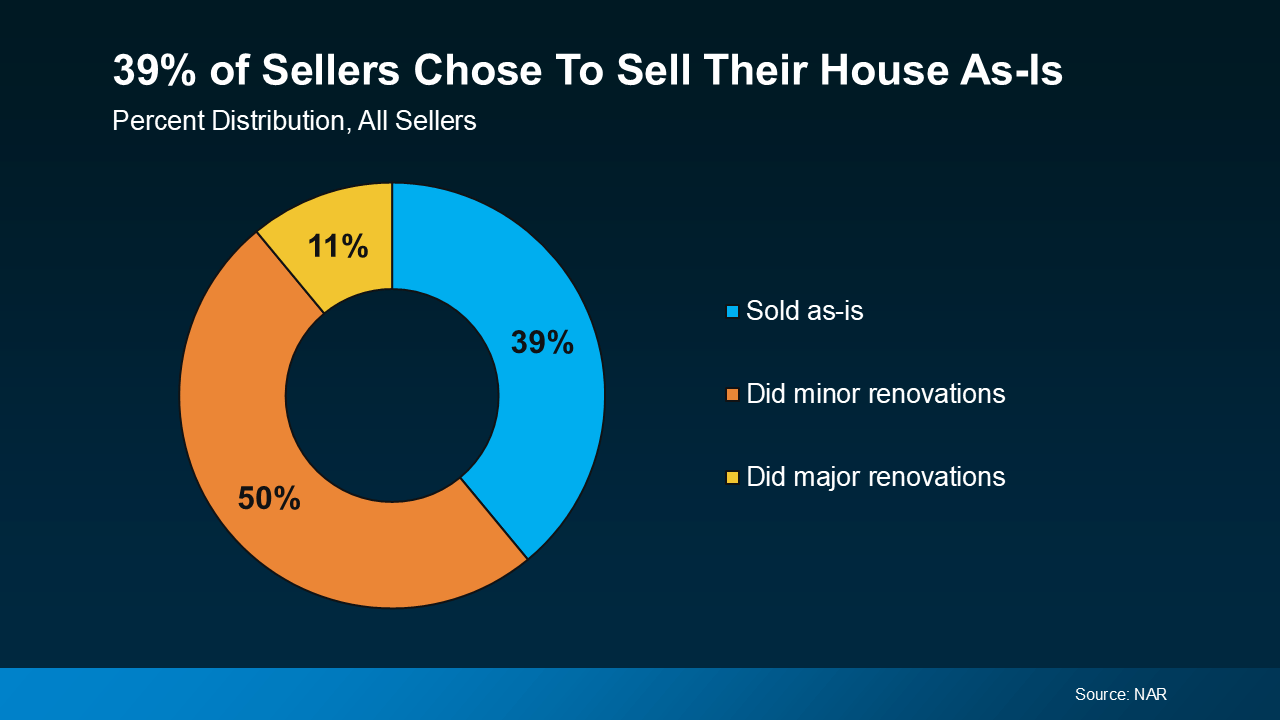

A recent study from the National Association of Realtors (NAR) shows most sellers (61%) completed at least minor repairs when selling their house. But sometimes life gets in the way and that’s just not possible. Maybe that’s why, 39% of sellers chose to sell as-is instead (see chart below):

If you’re feeling stressed because you don’t have the time, budget, or resources to tackle any repairs or updates, you may be tempted to sell your house as-is, too. But before you decide to go this route, here’s what you need to know.

What Does Selling As-Is Really Mean?

Selling as-is means you won’t make any repairs before the sale, and you won’t negotiate fixes after a buyer’s inspection. And this sends a signal to potential buyers that what they see is what they get.

If you’re eager to sell but money or time is tight, this can be a relief because it’s that much less you’ll have to worry about. But there are a few trade-offs you’ll have to be willing to make. This visual breaks down some of the pros and cons:

Typically, a home that’s updated sells for more because buyers are often willing to pay a premium for something that’s move-in ready. That’s why you may find not as many buyers will look at your house if you sell it in its current condition. And less interest from buyers could mean fewer offers, taking longer to sell, and ultimately, a lower price. Basically, while it’s easier for you, the final sale price might be less than you’d get if you invested in repairs and upgrades.

That doesn’t mean your house won’t sell – it just means it may not sell for as much as it would in top condition.

Here’s the good news though. In today’s market, as many as 56% of buyers surveyed would be willing to buy a home that needs some work. That’s because affordability is still a challenge, and while there are more homes for sale right now, inventory is lower than the norm. So, you might find there are a few more buyers who may be willing to take on the work themselves.

How an Agent Can Help

So, how do you make sure you’re making the right decision for your move? The key is working with a pro.

A good agent will help you weigh your options by showing you what comparable homes in your area have sold for, what updates your neighbors are making, and guide you in setting a fair price no matter what you decide. That helps you anticipate what your house may sell for either way – and that can be a key factor in your final decision.

Once you’ve picked which route you’re going to go and the asking price is set, your agent will market your house to maximize its appeal. And if you decide to sell as-is, they’ll call attention to the best features, like the location, size, and more, so it’s easy for buyers to see the potential, not just projects.

Bottom Line

Selling a home without making any repairs is possible in today’s market, but it does have some trade-offs. To make sure you’re considering all your options and making the best choice possible, let’s have a conversation.

Should You Sell Your House or Rent It Out?

When you’re ready to move, figuring out what to do with your house is a big decision. And today, more homeowners are considering renting their home instead of selling it.

Recent data from Zillow shows about two-thirds (66%) of sellers thought about renting their home before listing, with nearly a third (28%) taking that possibility seriously. Compared to 2021, when fewer than half (47%) of homeowners considered renting before selling, it’s clear this trend is on the rise.

So, should you sell your house and use the money toward your next home or keep it as a rental to build long-term wealth? Let’s walk through some important questions to help you determine the right path for your financial and lifestyle goals.

Is Your House a Good Fit for Renting?

Before you decide what to do, it’s important to think about if it would make a good rental in the first place. For instance, if you’re moving far away, managing ongoing maintenance could become a major hassle. Other factors to consider are if your neighborhood is ideal for rentals and if your house needs significant repairs before it’s ready for tenants.

If any of these situations sound familiar, selling might be a more practical choice.

Are You Ready for the Realities of Being a Landlord?

Managing a rental property involves more than collecting monthly rent. It’s a commitment that can be time-consuming and challenging.

For example, you may get maintenance calls at all hours of the day or discover damage that needs to be repaired before a new tenant moves in. There’s also the risk of tenants missing payments or breaking their lease, which can add unexpected stress and financial strain. As Redfin notes:

“Landlords have to fix things like broken pipes, defunct HVAC systems, and structural damage, among other essential repairs. If you don’t have a few thousand dollars on hand to take care of these repairs, you could end up in a bind.”

Do You Understand the Costs?

If you’re considering renting primarily for passive income, remember, there are additional costs you should anticipate. As an article from Bankrate explains:

Mortgage and Property Taxes: You still need to pay these expenses, even if the rent doesn’t cover all of it.

Insurance: Landlord insurance typically costs about 25% more than regular home insurance, and it’s necessary to cover damages and injuries.

Maintenance and Repairs: Plan to spend at least 1% of the home’s value annually, more if the house is older.

Finding a Tenant: This involves advertising costs and potentially paying for background checks.

Vacancies: If the property sits empty between tenants, you’ll lose rental income and have to cover the cost of the mortgage until you find a new tenant.

Management and HOA Fees: A property manager can ease the burden, but typically charges about 10% of the rent. HOA fees are an additional cost too, if applicable.

Bottom Line

To sum it all up, selling or renting out your home is a personal decision. Let’s connect so you have a pro on your side to help you feel supported and informed as you make your decision.

Expect the Unexpected: Anticipating Volatility in Today’s Housing Market

You’ve probably noticed one thing if you’re thinking about making a move: the housing market feels a bit unpredictable right now. The truth is, from home prices to mortgage rates, we’re seeing more volatility – and it’s important to understand why.

At a high-level, let’s break down what’s happening and the best way to navigate it.

What’s Driving Today’s Market Volatility?

Factors like economic data, unemployment numbers, decisions coming out of the Federal Reserve (The Fed), and even the presidential election, are creating uncertainty right now – and uncertainty leads to market volatility.

You can see that when you look at what’s happening with mortgage rates. New economic reports and other geopolitical events have an impact and can cause sudden shifts up or down, even though experts still forecast rates will come down overall. We’ve seen that effect play out recently, like when employment and inflation data get released each month.

And as the markets react, these types of updates will continue to have an impact on rates moving forward. As Greg McBride, CFA, Chief Financial Analyst at Bankrate, says:

“After steadily declining throughout the summer months, I expect more ups and downs to mortgage rates . . . Job market data will be closely watched as well as any clues from the Fed about the extent of upcoming interest rate cuts.”

This is exactly why the projected decline in mortgage rates isn’t going to be a straight line down over the next year. As Hannah Jones, Senior Economic Research Analyst at Realtor.com, explains:

“Rates have shown considerable volatility lately, and may continue to do so . . . Overall, we still expect a downward long-term mortgage rate trend.”

Plus, home prices and the number of homes on the market vary dramatically depending on where you’re looking to buy or sell, which makes it even harder to get a clear picture. In some areas, home prices are rising and inventory is tight, while in others, there are more homes available and it’s leading to more moderate pricing shifts.

As all of this unfolds, understanding what’s happening will help you make the right decisions, whether that’s buying or selling. And there’s one easy way to get that information: from a professional.

The Importance of Partnering with a Pro

While the road ahead may have some bumps and unexpected turns, you don’t have to go it alone. A great agent will keep you up to date on the latest market developments, guide you through any shifts, and help you make smart decisions based on your goals.

For example, as mortgage rates change, professionals (like your agent and a trusted lender) will explain how the shifts impact what you can reasonably plan for in your monthly payment. This will help you see how even a small change in rates can impact your bottom line – that way you don’t lose sight of the big picture even as shifts happen here and there.

And since conditions can vary significantly from one neighborhood to another, your agent will also help you understand the specifics of your market—whether it’s how to navigate competition with other buyers, the number of homes available, or what’s happening with local home prices. Their insights and expertise will help you adapt to any movement in the market.

Bottom Line

The housing market may be experiencing some shifts, but don’t let it stop you from making your move. With the support of an experienced real estate agent and a trusted lender, you’ll be ready to navigate the changes and make the most of the opportunities that come your way.

Let’s turn any uncertainty into your advantage, helping you move forward with confidence.