Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

How Do Presidential Elections Impact the Housing Market?

Are you wondering if the upcoming election will have an impact on the housing market? Here’s what history tells us you need to know if you’re considering a move. Data shows home sales slow in November but quickly bounce back and rise the following year. Prices usually keep climbing. And mortgage rates typically come down slightly. Presidential elections have only a small and temporary impact on the housing market. If you have questions, let’s connect.

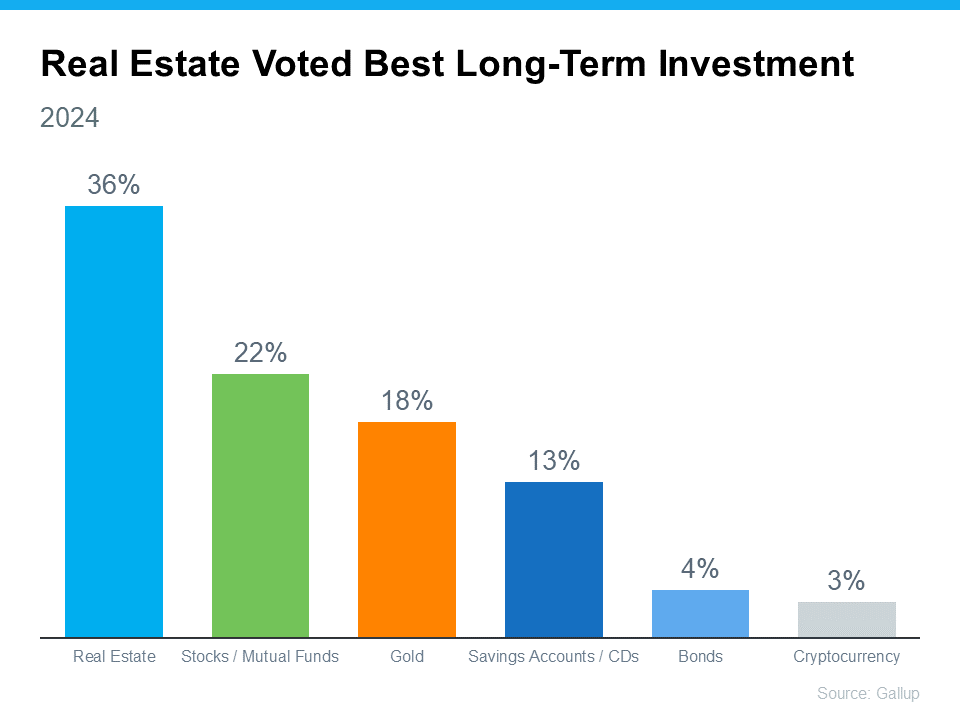

Real Estate Still Holds the Title of Best Long-Term Investment

With all the headlines circulating about home prices and mortgage rates, you may be asking yourself if it still makes sense to buy a home right now, or if it’s better to keep renting. Here’s some information that could help put your mind at ease by showing that investing in a home is still a powerful decision.

According to the experts at Gallup, real estate has been crowned the top long-term investment for a whopping 12 years in a row. It has consistently beat out other investment types like gold, stocks, and bonds. Just take a look at the graph below – it speaks volumes:

But why does real estate continue to reign supreme as a top-notch long-term investment? It’s because, even today, buying a home can be your golden ticket to building wealth over time.

Unlike other investments that can feel a bit like riding a rollercoaster with all the ups and downs and ongoing risk factors, real estate follows a more predictable and positive pattern.

History shows home values usually rise. And while prices may vary by market, that means as time goes by, your house is likely to appreciate in value. And that helps you grow your net worth in a big way. As an article from Realtor.com explains:

“Homeownership has long been tied to building wealth—and for good reason. Instead of throwing rent money out the window each month, owning a home allows you to build home equity. And over time, equity can turn your mortgage debt into a sizeable asset.”

So, if you’re on the fence about whether to rent or buy, remember that real estate was consistently voted the best long-term investment for a reason. And if you want to get in on that action, it may make sense to go ahead and buy (if you’re ready and able).

Bottom Line

When it comes to building wealth that stands the test of time, real estate is the name of the game. If you’re ready to start on your own journey toward homeownership, let’s connect today.

What To Do When Your House Didn’t Sell

If your listing expired and your house didn’t sell, it’s totally natural to feel a mix of frustration and disappointment. And as you’re working through that, you’re probably also wondering what went wrong and what you should do next.

If you still need to move and want to get it back on the market, here are some things to consider as you look back.

Was It Priced for Today’s Market?

Setting the right price from the start is key. While it might be tempting to try shooting high with your price, that can slow down the selling process big time. If your house was priced higher than others similar to it, it may have turned away buyers. And that’s likely why it sat on the market. As Rocket Mortgage explains:

“Buyer interest in your home is highest when it first comes on the market. That’s why it’s so important to start with the right price on day one. . . If you overprice your house, buyers may just raise an eyebrow and move on to the next listing without even coming for a showing. . . It can be easy to think your home is worth more but try not to let sentimental value color your judgment. Your home’s true value is whatever a buyer is willing to pay for it.”

Was It Easy for Buyers To Tour?

One of the biggest mistakes you can make when selling your house is overly restricting the days and times when potential buyers can tour it. Even though it might feel stressful to drop everything and leave when buyers want to see your house, being flexible with your schedule is important. After all, minimal access means minimal exposure to buyers. ShowingTime advises:

“. . . do your best to be as flexible as possible when granting access to your house for showings.”

Was It Set Up To Make the Best Impression on Buyers?

If buyers weren’t interested in your house, it’s worth taking another look at your home through their eyes. Are there outstanding repairs that may be distracting them? Even if it’s a small thing, some buyers may see it as a sign the maintenance on the home is falling behind.

Just remember, you don’t always need to make big upgrades. Selective small repairs or touch-ups go a long way. Things like tidying up your landscaping, a fresh coat of paint inside, or removing personal items and clutter can work wonders in sprucing up the house for potential buyers. You could also consider staging the home.

Were You Willing To Negotiate?

If there were offers coming in, but you weren’t ready to negotiate, that may be another reason why it didn’t sell. While you want to get top dollar for your house, you also need to be realistic about what your house can net in today’s market. The market is still tipped in a seller’s favor, but the supply of homes for sale is growing and buyers are feeling the sting of higher mortgage rates. So being willing to play ball can make closing a deal a whole lot easier. A skilled agent can help. As Ramsey Solutions explains:

“If you don’t have the money or time to fix home issues, consider offering some other form of incentive to buyers. . . An experienced real estate agent can help you arrange a deal where you and your buyer both come out on top.”

Did You Listen To Your Agent?

If you want an expert’s advice on why it didn’t sell, rely on a trusted real estate agent. Whether that’s the agent you used previously or a new one once the listing has officially expired, a great agent will sit down and take the time to talk it over with you. They’ll want to hear your honest opinion on what worked and what didn’t, and where you want to go from here.

Then, they’ll offer their perspective. This includes tailored advice and effective strategies for re-listing your house to get it sold. As Better Homes & Gardens says, an agent should be your go-to resource in this situation:

“If you’re frustrated with the timeline of your sale, chat with your real estate agent. Agents want what is best for you and the sale of your home, and having open communication about any frustrations will be key.”

Bottom Line

It’s natural to feel disappointed when your listing has expired and your house didn’t sell. Connect with a reliable real estate agent to determine what happened, and what changes you should make to get your house back on the market.

Housing Market Forecast: What’s Ahead for the 2nd Half of 2024

As we move into the second half of 2024, here’s what experts say you should expect for home prices, mortgage rates, and home sales.

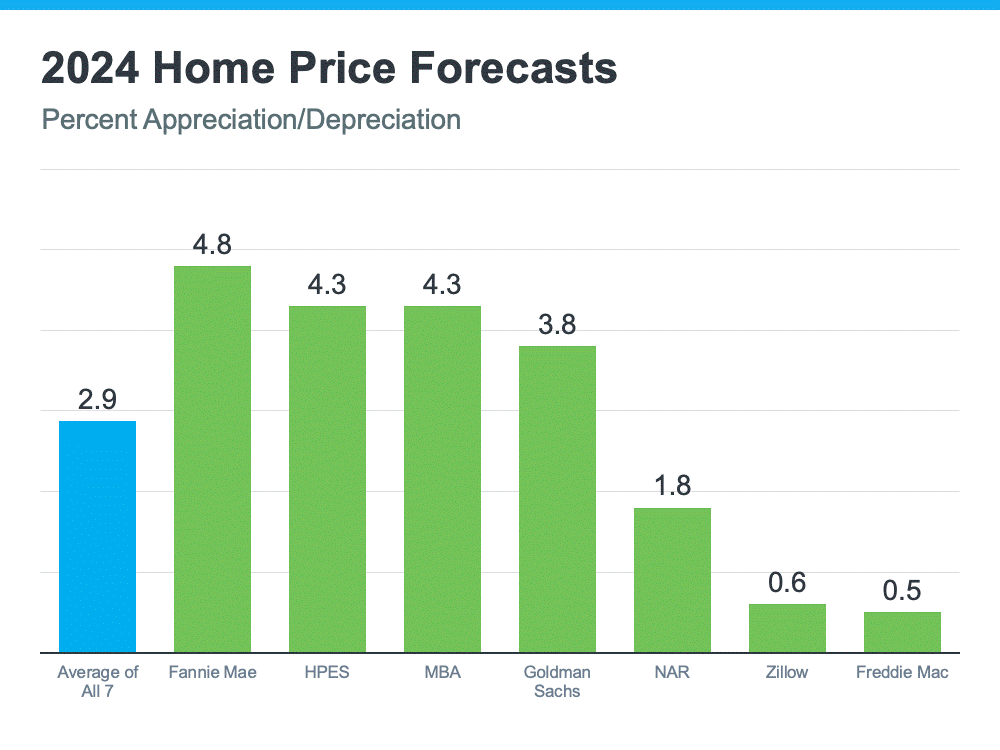

Home Prices Are Expected To Climb Moderately

Home prices are forecasted to rise at a more normal pace. The graph below shows the latest forecasts from seven of the most trusted sources in the industry:

The reason for continued appreciation? The supply of homes for sale. Jessica Lautz, Deputy Chief Economist at the National Association of Realtors (NAR), explains:

“One thing that seems to be pretty solid is that home prices are going to continue to go up, and the reason is that we don’t have housing inventory.”

While inventory is up compared to the last couple of years, it’s still low overall. And because there still aren’t enough homes to go around, that’ll keep upward pressure on prices.

If you’re thinking of buying, the good news is you won’t have to deal with prices skyrocketing like they did during the pandemic. Just remember, prices aren’t expected to drop. They’ll continue climbing, just at a slower pace.

So, getting into the market sooner rather than later could still save you money in the long run. Plus, you can feel confident experts say your home will grow in value after you buy it.

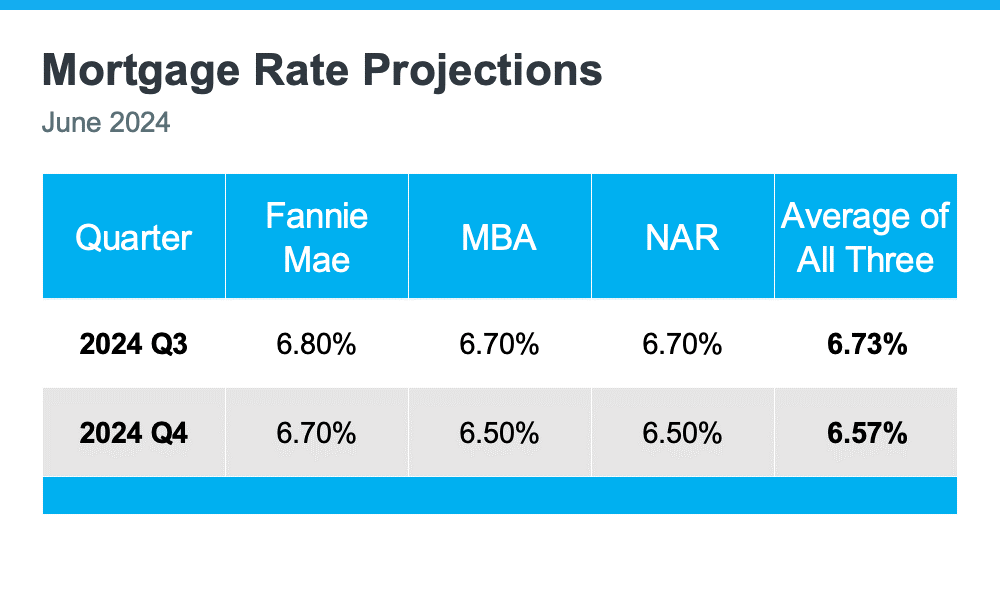

Mortgage Rates Are Forecast To Come Down Slightly

One of the best pieces of news for both buyers and sellers is that mortgage rates are expected to come down a bit, according to Fannie Mae, the Mortgage Bankers Association (MBA), and NAR (see chart below):

When you buy, even a small drop in mortgage rates can make a big difference in your monthly payments. For sellers, lower rates will bring more buyers back into the market, which can help you sell faster and potentially at a higher price. Plus, it may help you get off the fence, if you’ve been hesitant to sell due to today’s rates.

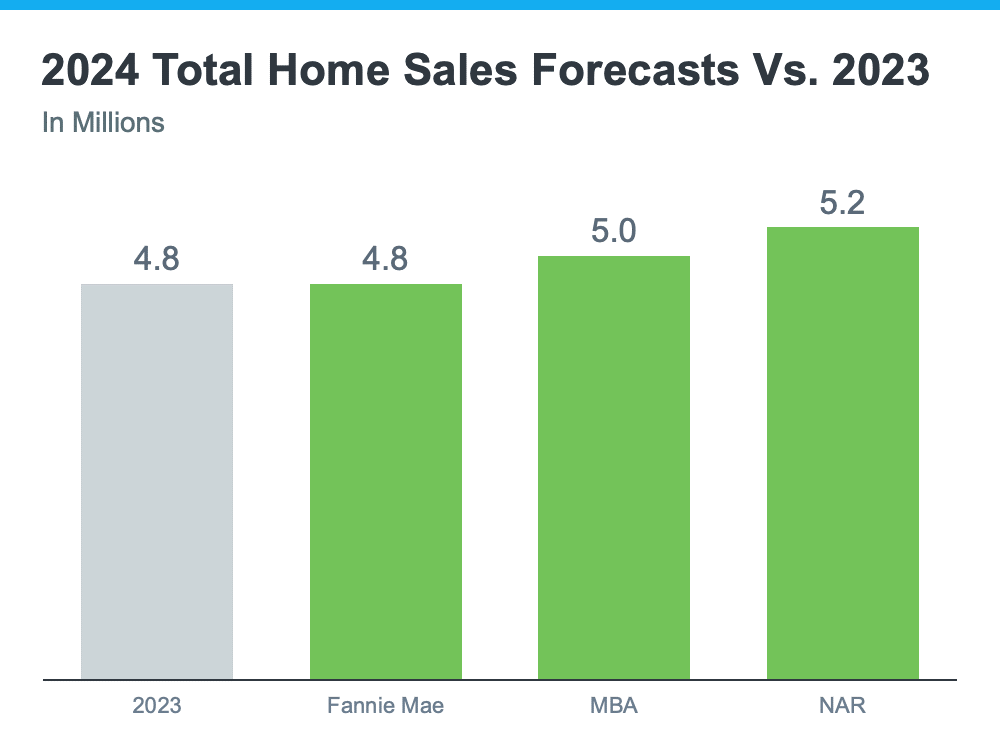

Home Sales Are Projected To Hold Steady

For 2024, the number of home sales will be about the same as last year and may even rise slightly. The graph below compares the 2024 home sales forecasts from Fannie Mae, MBA, and NAR to the 4.8 million homes that sold last year:

The average of the three forecasts is about 5 million sales in 2024 – a small increase from 2023. Lawrence Yun, Chief Economist at NAR, explains why:

“Job gains, steady mortgage rates and the release of inventory from pent-up home sellers will lead to more sales.”

With more inventory available and mortgage rates expected to go down, a few more homes are expected to be sold this year compared to last year. This means more people will be able to move. Let’s work together to make sure you’re one of them.

Bottom Line

If you have any questions or need help navigating the market, reach out.

Do Elections Impact the Housing Market?

The 2024 Presidential election is just months away. As someone who’s thinking about potentially buying or selling a home, you’re probably curious about what effect, if any, elections have on the housing market.

It’s a great question because buying or selling a home is a major decision, and it’s natural to wonder how such a major event might impact your plans.

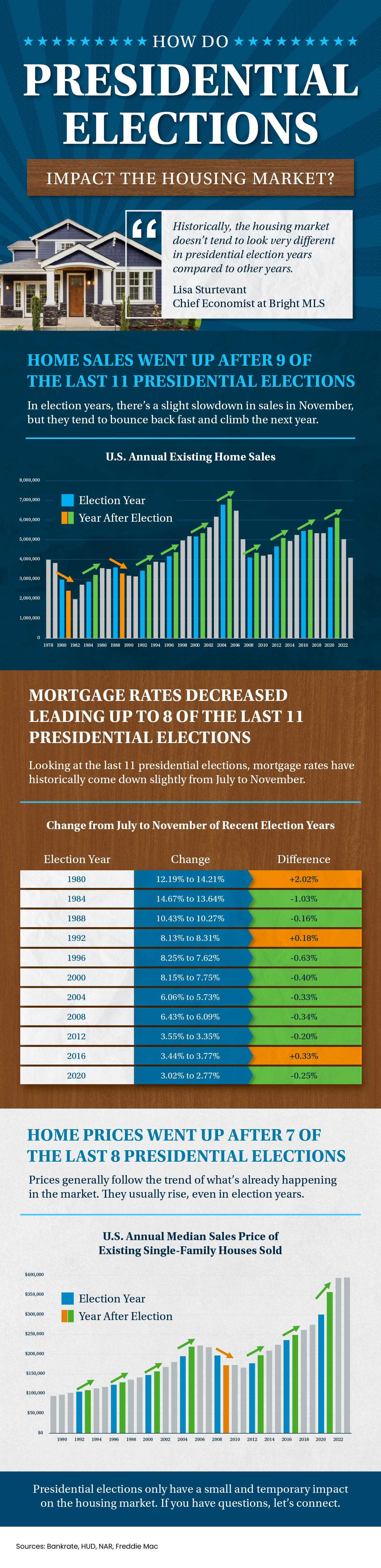

Historically, Presidential elections have only had a small, temporary impact on the housing market. Here’s the latest on exactly what’s happened to home sales, prices, and mortgage rates throughout those time periods.

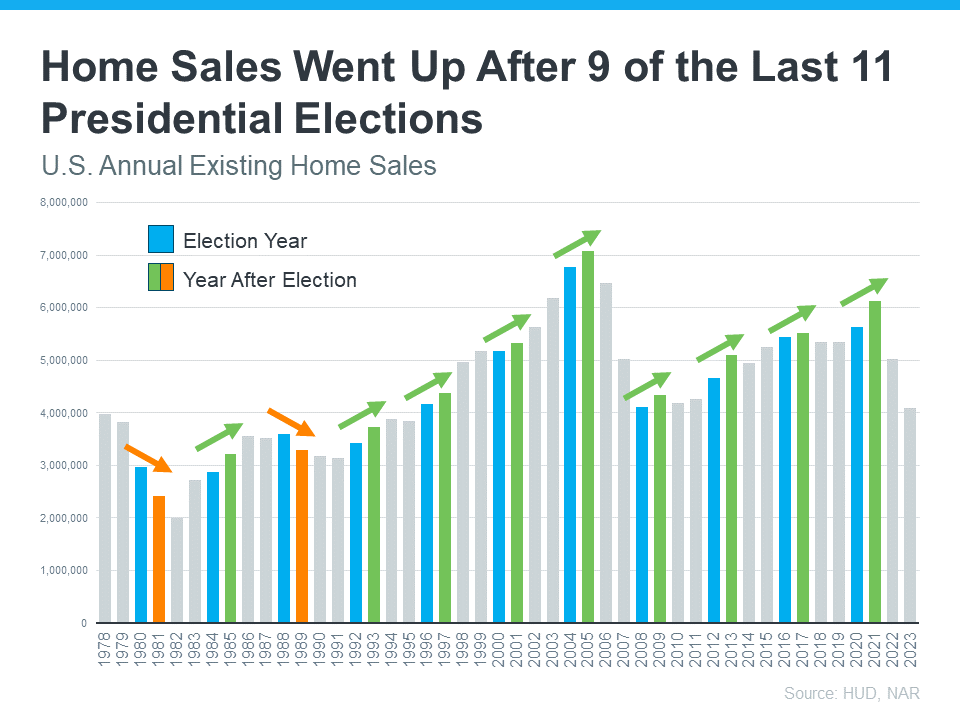

Home Sales

During the month of November, in years when the Presidential election takes place, there’s typically a slight slowdown in home sales. As Ali Wolf, Chief Economist at Zonda, explains:

“Usually, home sales are unchanged compared to a non-election year with the exception being November. In an election year, November is slower than normal.”

This is mostly because some people feel uncertain and hesitant about making big decisions during such a pivotal time. However, it’s important to know this slowdown is temporary. Historically, home sales bounce back in December and continue to rise the following year.

In fact, data from the Department of Housing and Urban Development (HUD) and the National Association of Realtors (NAR) shows after nine of the last 11 Presidential elections, home sales went up the next year (see graph below)

The graph shows annual home sales going back to 1978. Each year with a Presidential election is noted in blue. The year immediately after each election is green if existing home sales rose that year. The two orange bars represent the only years when home sales decreased after an election.

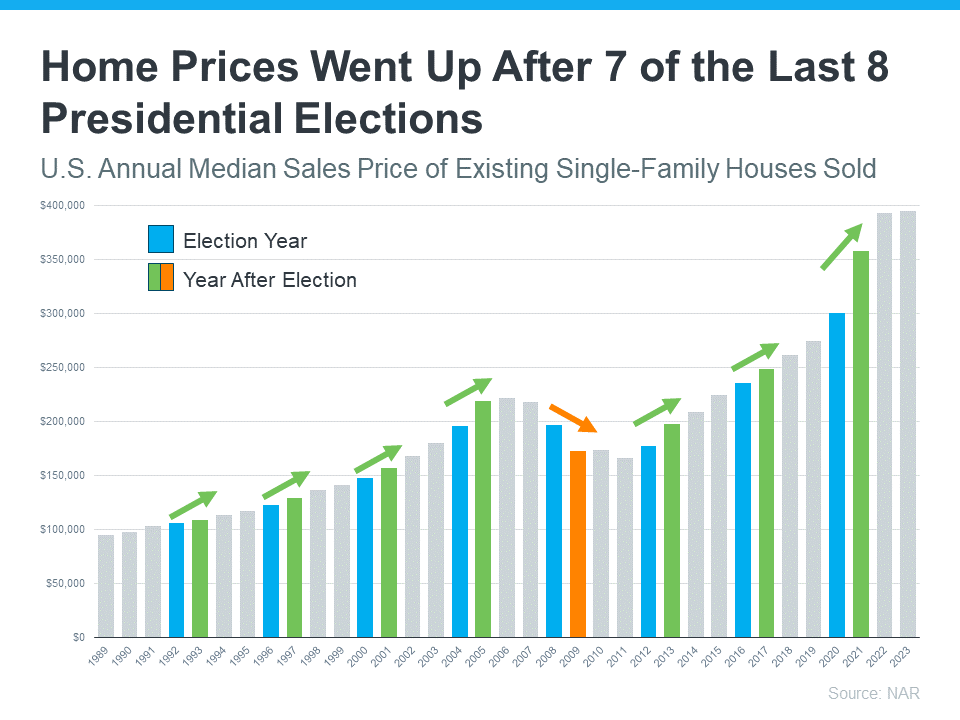

Home Prices

What about home prices? Do they drop during election years? Not typically. As residential appraiser and housing analyst Ryan Lundquist puts it:

“An election year doesn’t alter the price trend that is already happening in the market.”

Home prices are pretty resilient. They generally rise year-over-year, regardless of elections. The latest data from NAR shows after seven of the last eight Presidential elections, home prices increased the following year (see graph below)

Just like the previous graph, this shows election years in blue. The only year when prices declined after an election is in orange. That was during the housing market crash, which was far from a typical year. Today’s market is different than it was back then.

All the green bars represent when prices rose the following year. So, if you’re worried about your home losing value because of an election, you can rest easy knowing prices rise after most Presidential elections.

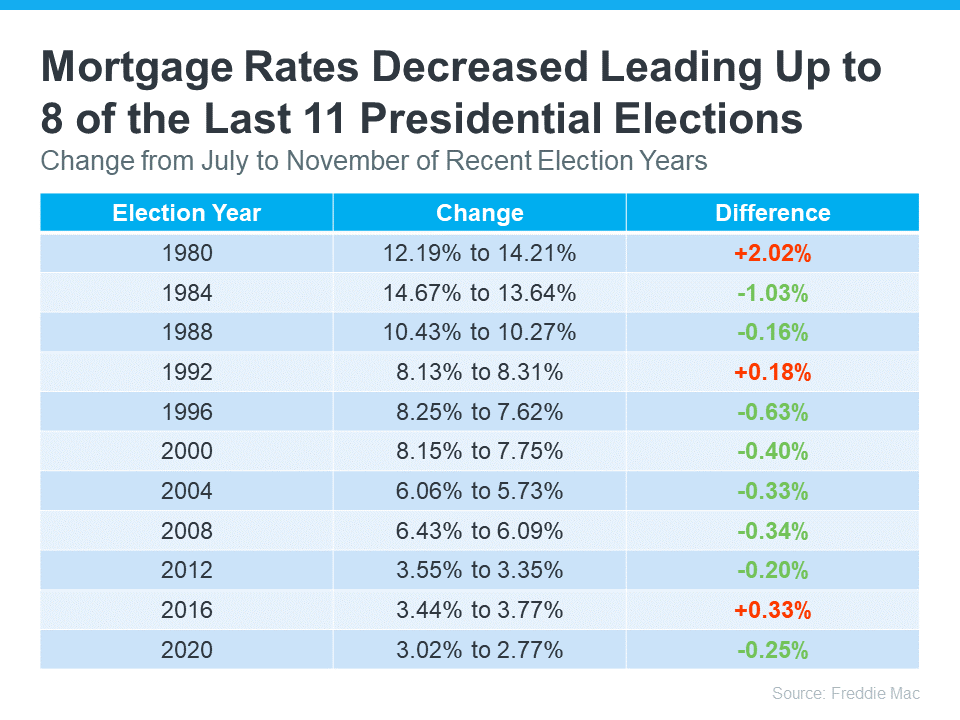

Mortgage Rates

Mortgage rates are important because they affect how much your monthly payment will be when you buy a home. Looking at the last 11 Presidential election years, data from Freddie Mac shows mortgage rates decreased from July to November in eight of them (see chart below)

Most forecasts expect mortgage rates to ease slightly throughout the remainder of the year. If they’re right, this year will follow the trend of declining rates leading up to most previous elections. And if you’re looking to buy a home in the coming months, this could be good news, as lower rates could mean a lower monthly payment.

What This Means for You

So, what’s the big takeaway? While Presidential elections do have some impact on the housing market, the effects are usually small and temporary. As Lisa Sturtevant, Chief Economist at Bright MLS, says:

“Historically, the housing market doesn’t tend to look very different in presidential election years compared to other years.”

For most buyers and sellers, elections don’t have a major impact on their plans.

Bottom Line

While it’s natural to feel a bit uncertain during an election year, history shows the housing market remains strong and resilient. For help navigating the market, election year or not, let’s connect.