Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Key Skills You Need Your Listing Agent To Have

Selling your house is a big decision. And that can make it feel both exciting and a little bit nerve-wracking. But the key to a successful sale is finding the perfect listing agent to work with you throughout the process. A listing agent, also known as a seller’s agent, helps market and sell your house while advocating for you every step of the way.

But, how do you know you’ve found the perfect match in an agent? Here are three key skills you’ll want your listing agent to have.

They Price Your House Based on the Latest Data

While it may be tempting to pick the agent who suggests the highest asking price for your house, that strategy may cost you. It’s easy to get caught up in the excitement when you see a bigger number, but overpricing your house can have consequences. It could mean it’ll sit on the market longer because the higher price is actually deterring buyers.

Instead, you want to pick an agent who’s going to have an open conversation about how they think you should price your house and why. A great agent will base their pricing strategy on solid data. They won’t throw out a number just to win your listing. Instead, they’ll show you the facts, explain their pricing strategy, and make sure you’re on the same page. As NerdWallet explains:

“An agent who recommends the highest price isn’t always the best choice. Choose an agent who backs up the recommendation with market knowledge.”

They’re a Great Negotiator

The home-selling process can be emotional, especially if you’ve been in your house for a long time. You’re connected to it and have a lot of memories there. This can make the negotiation process harder. That’s where a trusted professional comes in.

A skilled listing agent will be calm under pressure and will be your point-person in all of those conversations. Their experience in handling the back-and-forth gives you with the peace of mind that you’ve got someone on your side who’s got your best interests in mind throughout this journey.

They’re a Skilled Problem Solver

At the heart of it all, a listing agent’s main priority is to get your house sold. A great agent never loses sight of that goal and will help you prioritize your needs above all else. If they identify any necessary steps you need to take, they’ll be open with you about it. Their commitment to your success means they’ll work with you to address any potential roadblocks and find creative solutions to anything that pops up along the way.

BankRate explains it like this:

“Just as important as the knowledge and experience agents bring is their ability to guide you smoothly through the process. Above all, go with an agent you trust and will feel comfortable with. . .”

Bottom Line

Whether you’re a first-time seller or you’ve been through selling a house before, a great listing agent is the key to success. Let’s connect so you have a skilled local expert by your side to guide you through every step of the process.

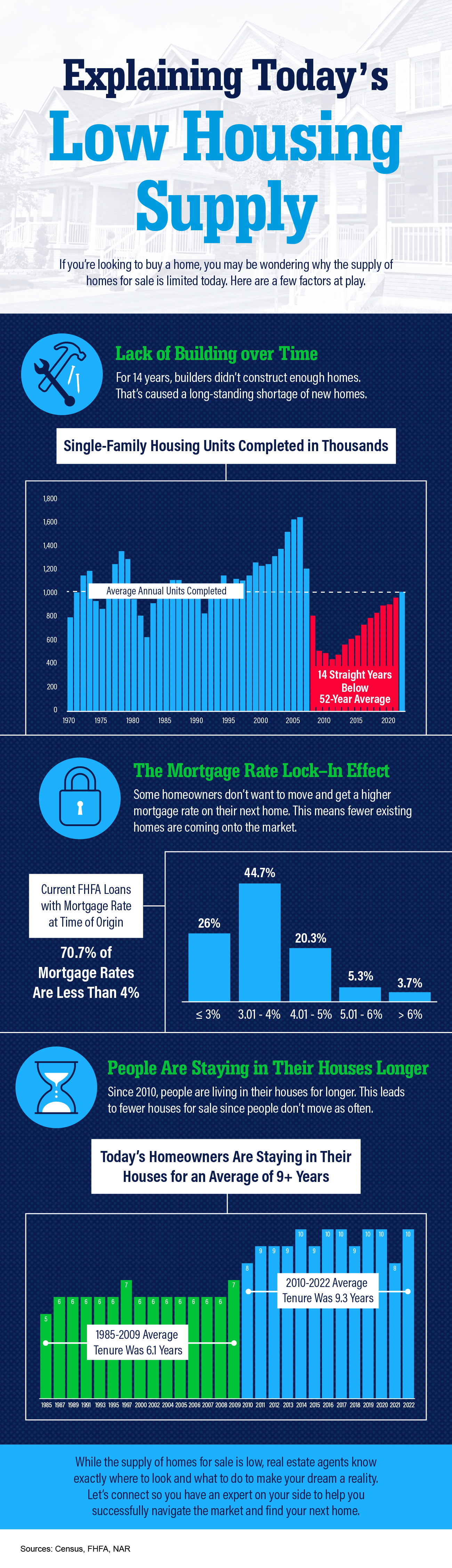

Explaining Today’s Low Housing Supply

Some Highlights

- Wondering why the supply of homes for sale is limited today? There are a few factors at play.

- Lack of building over time, the mortgage rate lock-in effect, and people staying in their houses longer are three of the main reasons why supply is low.

- But real estate agents know exactly where to look and what to do to make your dream a reality. Let’s connect so you have an expert on your side to help you successfully navigate the market and find your next home.

Beginning with Pre-Approval

If you’re looking to buy a home this fall, there are a few things you need to know. Affordability is tight with today’s mortgage rates and rising home prices. At the same time, there’s a limited number of homes on the market right now and that’s creating some competition among buyers. But, if you’re strategic, there are ways to navigate these waters. The first thing you’ll want to do is get pre-approved for a mortgage. That way you’ll know your numbers and can set yourself up for success from the start of your home search.

What Pre-Approval Does for You

To understand why it’s such an important step, you need to know what pre-approval is. As part of the homebuying process, a lender looks at your finances to determine what they’d be willing to loan you. From there, your lender will give you a pre-approval letter to help you know how much money you can borrow. Freddie Mac explains it like this:

“A pre-approval is an indication from your lender that they are willing to lend you a certain amount of money to buy your future home. . . . Keep in mind that the loan amount in the pre-approval letter is the lender’s maximum offer. Ultimately, you should only borrow an amount you are comfortable repaying.”

Basically, pre-approval gives you critical information about the homebuying process that’ll help you understand how much you may be able to borrow. Why does this help you, especially today? With higher mortgage rates and home prices impacting affordability for many buyers right now, a solid understanding of your numbers is even more important so you can truly wrap your head around your options.

Pre-Approval Helps Show Sellers You’re a Serious Buyer

Let’s face it, there are more buyers looking to buy than there are homes available for sale and that imbalance is creating some competition among homebuyers. That means you could see yourself in a multiple-offer scenario when you make an offer on a home. But getting pre-approved for a mortgage can help you stand out from other hopeful buyers.

As an article from Wall Street Journal (WSJ) says:

“If you plan to use a mortgage for your home purchase, preapproval should be among the first steps in your search process. Not only can getting preapproved help you zero in on the right price range, but it can give you a leg up on other buyers, too.”

Pre-approval shows the seller you’re a serious buyer that’s already undergone a credit and financial check, making it more likely that the sale will move forward without unexpected delays or financial issues.

Bottom Line

Getting pre-approved is an important first step when you’re buying a home. The more prepared you are, the better chance you have of getting the home you want. Connect with a trusted lender so you have the tools you need to purchase a home in today’s market.

Are More Homes Coming onto the Market?

An important factor shaping today’s market is the number of homes for sale. And, if you’re considering whether or not to list your house, that’s one of the biggest advantages you have right now. When housing inventory is this low, your house will stand out, especially if it’s priced right.

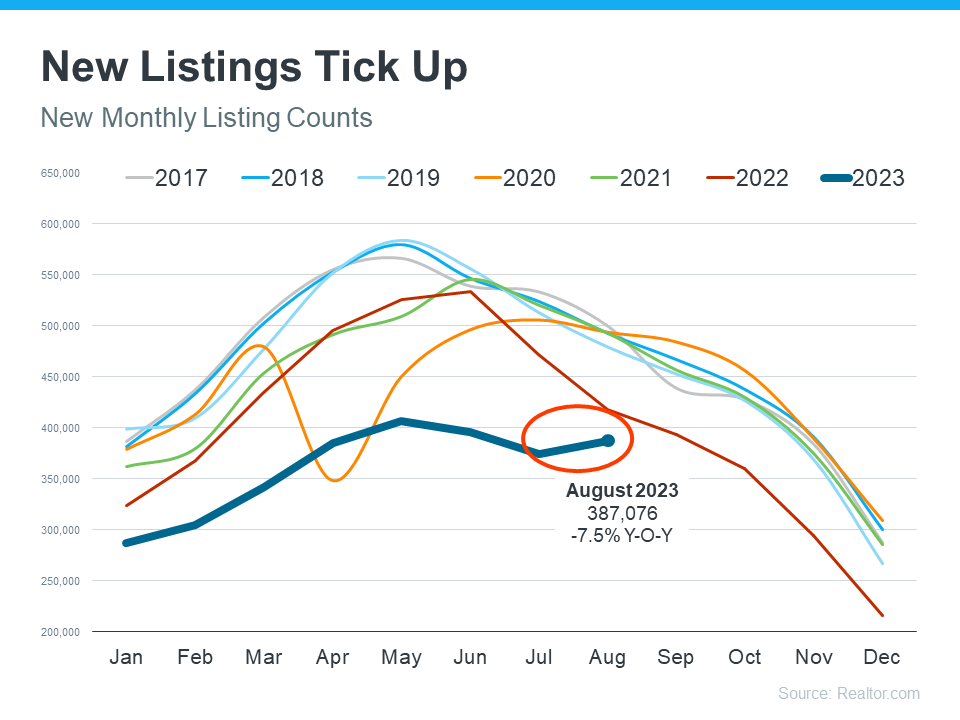

But there are some early signs that more listings are coming. According to the latest data, new listings (homeowners who just put their house up for sale) are trending up. Here’s a look at why this is noteworthy and what it may mean for you.

More Homes Are Coming onto the Market than Usual

It’s well known that the busiest time in the housing market each year is the spring buying season. That’s why there’s a predictable increase in the volume of newly listed homes throughout the first half of the year. Sellers are anticipating this and ramping up for the months when buyers are most active. But, as the school year kicks off and as the holidays approach, the market cools. It’s what’s expected.

But here’s what’s surprising. Based on the latest data from Realtor.com, there’s an increase in the number of sellers listing their houses later this year than usual. A peak this late in the year isn’t typical. You can see both the normal seasonal trend and the unusual August in the graph below:

As Realtor.com explains:

“While inventory continues to be in short supply, August witnessed an unusual uptick in newly listed homes compared to July, hopefully signaling a return in seller activity heading toward the fall season . . .”

While this is only one month of data, it’s unusual enough to note. It’s still too early to say for sure if this trend will continue, but it’s something you’ll want to stay ahead of if it does.

What This Means for You

If you’ve been putting off selling your house, now may be the sweet spot to make your move. That’s because, if this trend continues, you’ll have more competition the longer you wait. And if your neighbor puts their house up for sale too, it means you may have to share buyers’ attention with that other homeowner. If you sell now, you can beat your neighbors to the punch.

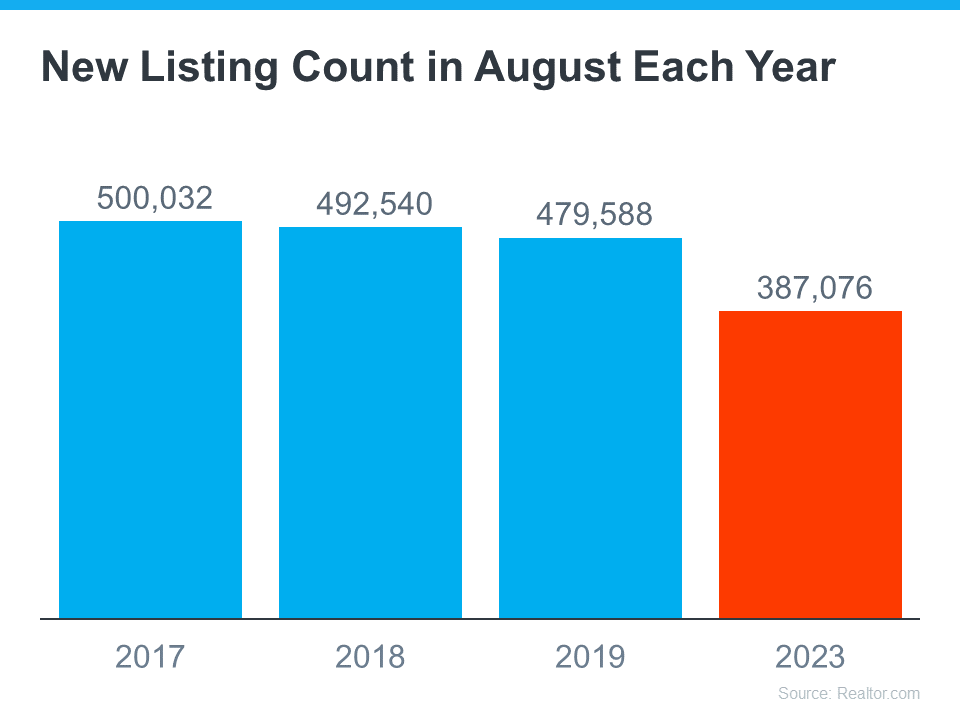

But, even with more homes coming onto the market, the market is still well below normal supply levels. And, that inventory deficit isn’t going to be reversed overnight. The graph below helps put this into context, so you can see the opportunity you still have now:

Bottom Line

Even though inventory is still low, you don’t want to wait for more competition to pop up in your neighborhood. You still have an incredible opportunity if you sell your house today. Let’s connect to explore the benefits of selling now before more homes come to the market.

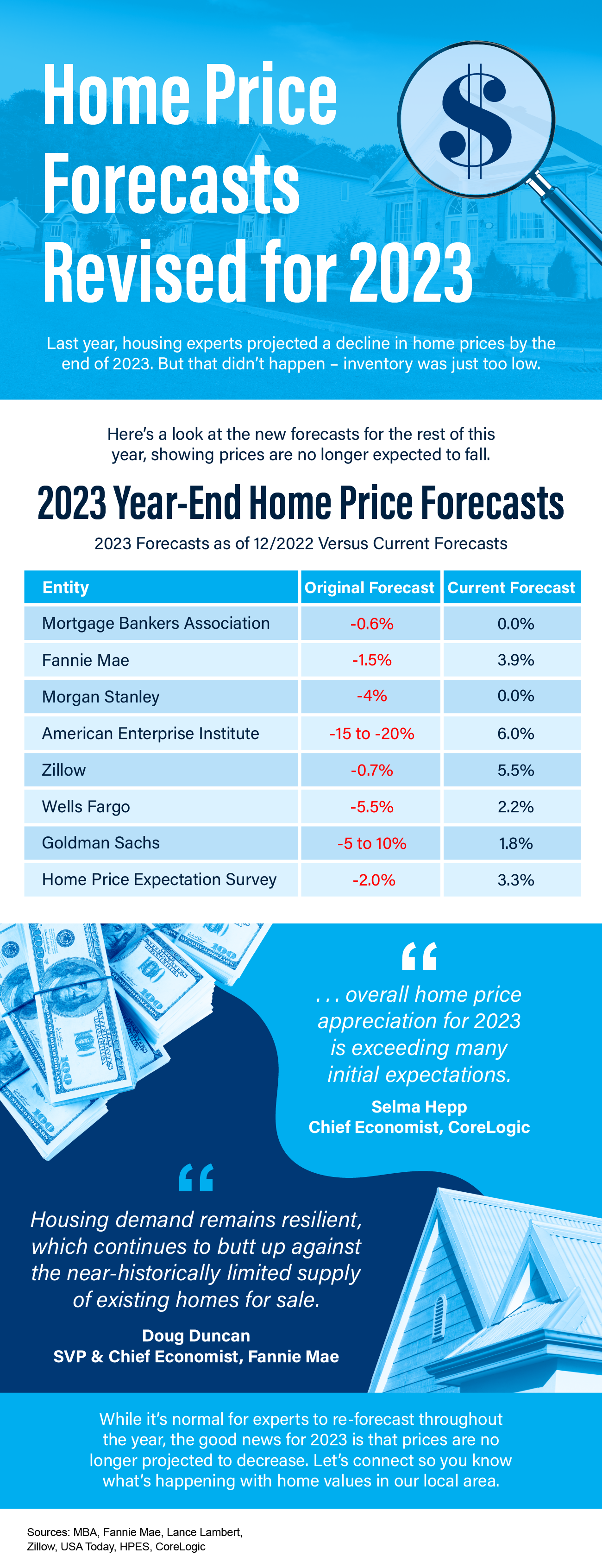

Home Price Forecasts Revised for 2023

Some Highlights

- Last year, some housing experts projected a decline in home prices by the end of 2023. But that didn’t happen – inventory was just too low.

- While it’s normal for experts to re-forecast throughout the year, the good news for 2023 is that prices are no longer projected to decrease.

- Let’s connect so you know what’s happening with home values in our local area.

Sources

- https://www.mba.org/docs/default-source/research-and-forecasts/forecasts/mortgage-finance-forecast-dec-2022.pdf

- https://www.mba.org/docs/default-source/research-and-forecasts/forecasts/2023/mortgage-finance-forecast-aug-2023.pdf

- https://www.fanniemae.com/media/45801/display

- https://www.fanniemae.com/media/48726/display

- https://twitter.com/NewsLambert/status/1671900591113609216 (Morgan Stanley)

- https://twitter.com/NewsLambert/status/1671556169712672768 (AEI)

- https://www.zillow.com/research/data/

- https://www.zillow.com/research/housing-market-challenges-32923/

- https://ustoday.news/a-20-drop-in-house-prices-7-forecast-models-tend-to-crash-here-the-other-13-models-show-the-housing-market-in-2023/ (Wells Fargo)

- https://twitter.com/NewsLambert/status/1686959362563092480 (Wells Fargo)

- https://twitter.com/NewsLambert/status/1691799764466008217 (Goldman Sachs)

- https://pulsenomics.com/surveys/#home-price-expectations

- https://www.corelogic.com/intelligence/us-corelogic-sp-case-shiller-index-down-by-0-5-year-over-year-in-may-but-a-turning-point-may-be-ahead/

- https://view.e.fanniemae.com/?qs=