Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Why You May Still Want To Sell Your House After All

Even though you may feel reluctant to sell your house because you don’t want to take on a mortgage rate that’s higher than the one you have now, there’s more to consider. While the financial side of things does matter, your personal needs may actually matter just as much. As an article from Bankrate says:

“Deciding whether it’s the right time to sell your home is a very personal decision. There are numerous important questions to consider, both financial and lifestyle-based, before putting your home on the market.”

So, ask yourself this: why did I want to move in the first place?

Chances are your primary motivation wasn’t just financial in nature. Why you’re really thinking about selling likely has more to do with something changing in your life or a shift in what you need out of your house.

Reasons Homeowners Still Need To Sell Today

Let’s explore some of the most common reasons sellers are moving today. A recent article from Builder Online helps shed light on this. In this research, they identified the following categories:

- Marriage – If you just got married, you may find you either need more space than you currently have, or the two of you want to find a new place you picked out together.

- Divorce – If you’re getting separated or are divorcing your partner, chances are it’ll be difficult to live under the same roof. Selling the place you have, so you can own get your own spot, may be necessary.

- Births – If your household is growing, you may need more square footage, including more bedrooms. If you’re running out of room for everyone, you may not be able to wait to move.

- Deaths – If you’ve recently lost a loved one, it can be hard to spend time in that home. You may need to move for financial reasons or because you no longer need all the space.

- Retirement – If you’re in the process of retiring, or you just did, you may be looking to downsize to cut costs, relocate to be closer to loved ones, or move to a dream location. In this new phase of life, your current home may not be able to deliver what you need.

You may find you share one of these top motivators. If any of these resonate with you, it may be time to move so you can find a house better suited to your changing needs. A survey from Realtor.com finds other sellers are in the same boat. It says, 1 in 4 sellers are choosing to move for personal reasons, even with current mortgage rates:

“. . . more than half of seller-buyers (56%) who are planning to sell in the next 12 months said they are waiting for rates to come down, while 25% need to sell soon for personal reasons.”

If you need to sell now because something in your own life has changed, don’t let rates hold you back from what you want. You have options to help make that move possible. You can use the equity you already have in your current home toward your next purchase. And with how much equity homeowners have right now, you may be able to finance less than you’d expect, or pay all cash to avoid borrowing at all.

Bottom Line

When you’re ready to prioritize your changing needs, let’s connect. You need an expert on your side to help you list your house and find a home that delivers on everything you’re looking for.

How Inflation Affects the Housing Market

Have you ever wondered how inflation impacts the housing market? Believe it or not, they’re connected. Whenever there are changes to one, both are affected. Here’s a high-level overview of the connection between the two.

The Relationship Between Housing Inflation and Overall Inflation

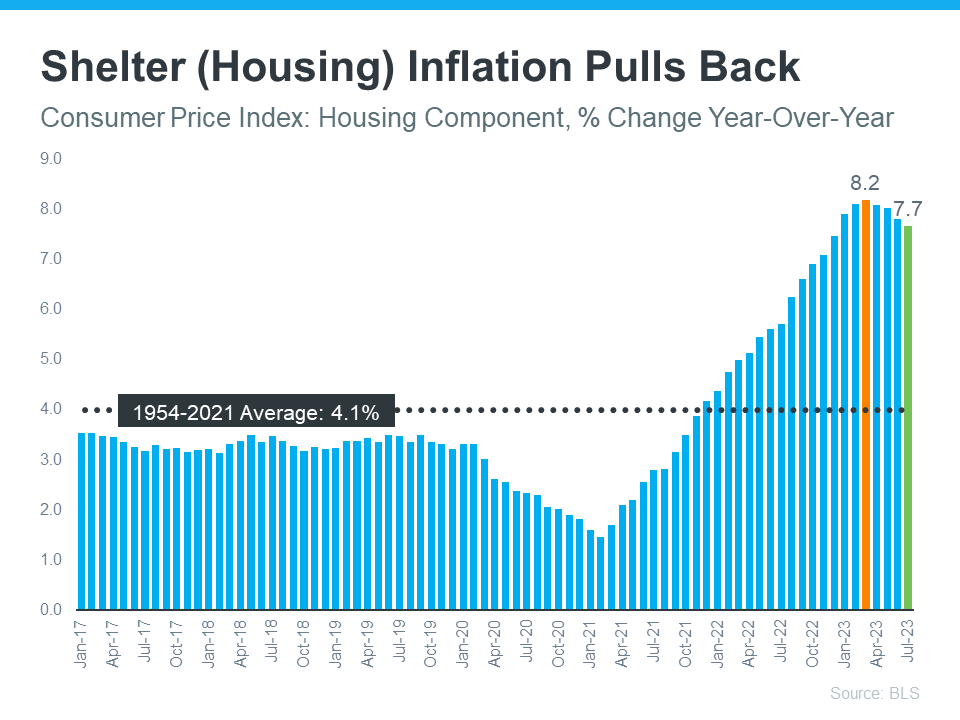

Shelter inflation is the measure of price growth specific to housing. It comes from a survey of renters and homeowners that’s done by the Bureau of Labor Statistics (BLS). The survey asks renters how much they’re paying in rent, and homeowners how much they’d rent their homes for, if they weren’t living in them.

Much like overall inflation measures the cost of everyday items, shelter inflation measures the cost of housing. And for four consecutive months, based on that survey, shelter inflation has been coming down (see graph below):

Why does this matter? Well, shelter inflation makes up about one-third of overall inflation, as measured by the Consumer Price Index (CPI). So, when shelter inflation moves, it leads to noticeable moves in overall inflation. That means the recent dip in shelter inflation might be a sign that overall inflation could fall in the months ahead.

That moderation would be a welcome sight for the Federal Reserve (the Fed). They’ve been working to get inflation under control since early 2022. While they’ve made some headway (it peaked at 8.9% in the middle of last year), they’re still trying to get to their 2% goal (the latest report is 3.3%).

Inflation and the Federal Funds Rate

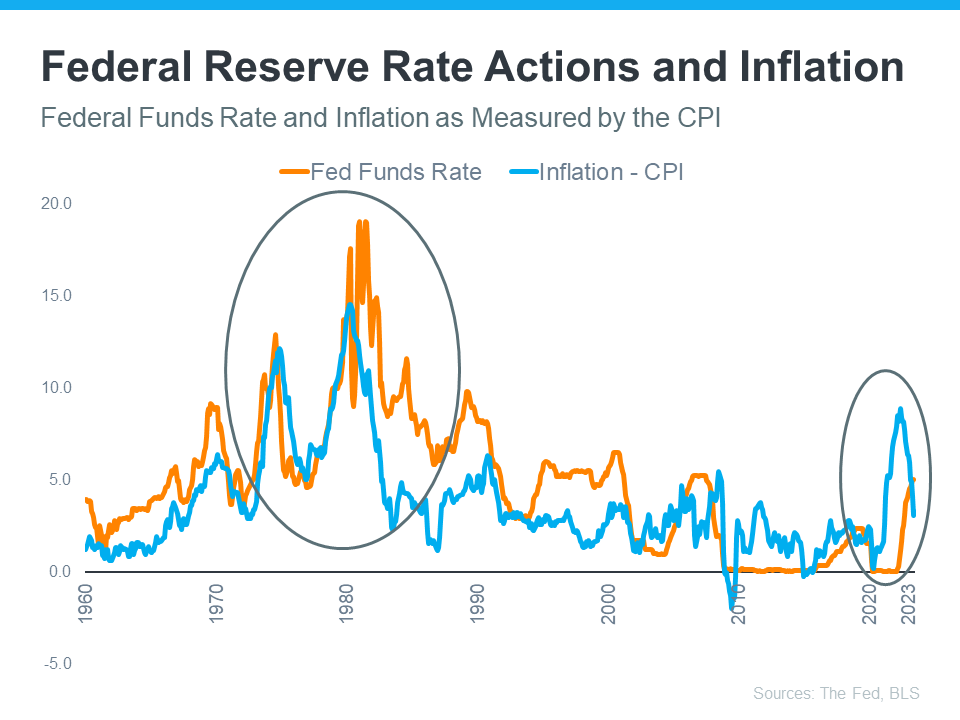

What’s the Fed been doing to lower inflation? They’ve been increasing the Federal Funds Rate. That interest rate influences how much it costs banks to borrow money from each other. When inflation climbed, the Fed responded by raising the Federal Funds Rate to keep the economy from overheating.

The graph below shows the relationship between the two. Each time inflation (shown in the blue line) starts to climb, the Fed raises the Federal Funds Rate (shown in the orange line) to try to get it back to their target of 2% (see below):

The circled portion of the graph shows the most recent spike in inflation, the Fed’s actions to raise the Federal Funds Rate to fight that, and the moderation of inflation that happened in response to that hike. As inflation gets closer to the Fed’s current 2% goal, they may not need to raise the Federal Funds Rate much further.

A Brighter Future for Mortgage Rates?

So, what does all of this mean for you? While the actions coming out of the Fed don’t determine mortgage rates, they do have an impact. As Mortgage Professional America (MPA) explains:

“. . . mortgage rates and inflation are connected, however indirectly. When inflation rises, mortgage rates rise to keep up with the value of the US dollar. When inflation drops, mortgage rates follow suit.”

While no one can predict the future for mortgage rates, it’s encouraging to see the signs of moderating inflation in the economy.

Bottom Line

Whether you’re looking to buy, sell, or just stay informed about the housing market, let’s connect.

Why You Need a True Expert in Today’s Housing Market

The housing market continues to shift and change, and in a fast-moving landscape like we’re in right now, it’s more important than ever to have a trusted real estate agent on your side. Whether you’re buying your first home or selling once again, it’s mission critical to work with an expert who can guide you through each unique step of the process.

The reality is, not all agents operate the same way. To truly make a powerful and confident decision as you buy or sell a home, you need a real estate expert who uses their knowledge of what’s really happening with home prices, housing supply, industry projections, and more to give you the best possible advice. Someone who can provide clarity and trust like that is essential to your success. Jay Thompson, Real Estate Industry Consultant, explains:

“Housing market headlines are everywhere. Many are quite sensational, ending with exclamation points or predicting impending doom for the industry. Clickbait, the sensationalizing of headlines and content, has been an issue since the dawn of the internet, and housing news is not immune to it.”

Unfortunately, when information in the media isn’t clear, it can generate a lot of fear and uncertainty for consumers. As Jason Lewris, Co-Founder and Chief Data Officer at Parcl, says:

“In the absence of trustworthy, up-to-date information, real estate decisions are increasingly being driven by fear, uncertainty, and doubt.”

But it doesn’t have to be that way. Buying a home is a big decision, and it should be one you feel confident making. You can lean on an expert to help you separate fact from fiction and get the answers you need.

The right agent can assist you in figuring out what’s going on at the national level and in your local area. They can debunk headlines using data you can trust. Experts have in-depth knowledge of the industry and can provide context, so you know how current trends compare to the normal ebbs and flows in the housing market, historical data, and more.

Then, to make sure you have the full picture, an agent can tell you if your local area is following the national trend or if they’re seeing something different in your market. Together, you can use all that information to make the best possible decision.

After all, making a move is a potentially life-changing milestone. It should be something you feel ready for and excited about. And that’s where a trusted expert comes in.

Bottom Line

If you want sound advice and trusted information about our local housing market, let’s connect.

Equity Is a Game Changer for Homeowners Looking To Sell

If you’re a homeowner, you might be torn on whether or not to sell your house right now. Maybe that’s because you don’t want to take on a higher mortgage rate on your next home. If that’s your biggest hurdle, understanding your equity may be exactly what you need to help you feel more comfortable making your move.

What Equity Is and How It Works

Equity is the current value of your home minus what you owe on the loan. And recently, that equity has been growing far faster than you may expect.

Over the last few years, home prices rose dramatically, and that gave your equity a big boost very quickly. While the market has started to normalize, there’s still an imbalance between the number of homes available for sale and the number of buyers looking to make a purchase. And it’s because homes are in such high demand that prices are back on the rise today. Rob Barber, CEO of ATTOM, a property data provider, explains:

“Equity levels were high even during the recent downturn, and now they are going back up and better than ever.”

How Equity Benefits You in Today’s Market

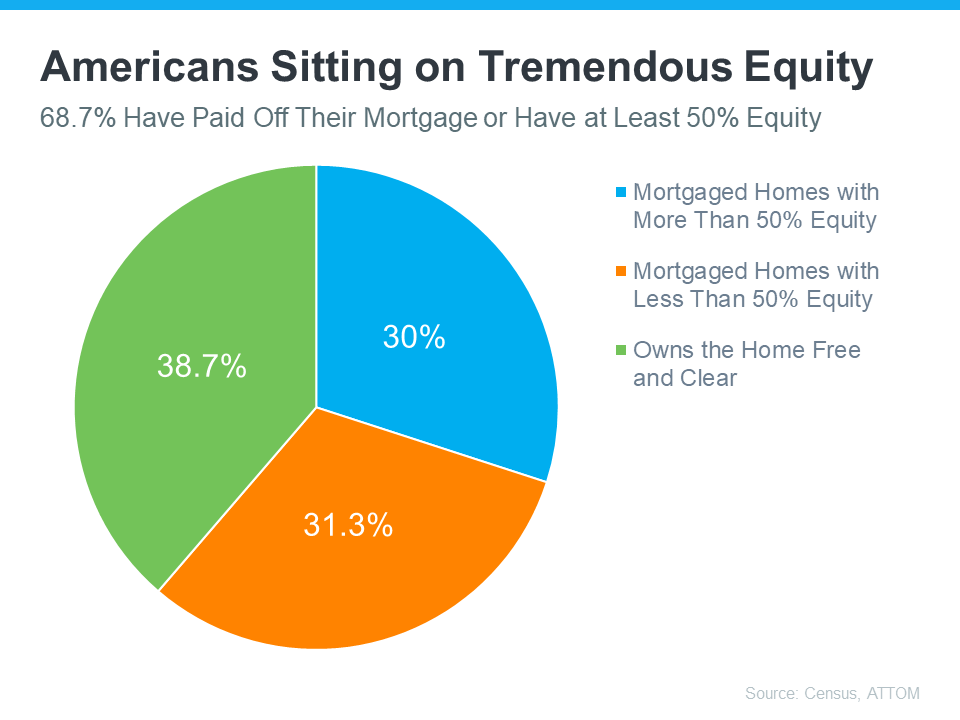

With today’s affordability challenges, that equity can be a game changer when you move. Here’s why. Based on data from ATTOM and the Census, nearly two-thirds (68.7%) of homeowners have either paid off their mortgages or have at least 50% equity (see chart below):

That means roughly 70% have a tremendous amount of equity right now.

Once you sell your house, you can use your equity to help with your next purchase. It could be some (if not all) of what you’ll need for your next down payment. It may even be enough to allow you to put a considerably larger down payment on your next home, so you don’t have to finance quite as much. And, if you’ve been in your current house for years, you may have even built up enough equity to pay in all cash. If that’s true for you, you’d be able to avoid borrowing altogether, so you wouldn’t have to worry about today’s mortgage rates.

How To Find Out How Much Equity You Have

The best way to learn how much you have is to reach out to a trusted real estate agent for a Professional Equity Assessment Report (PEAR).

Bottom Line

If you’re planning to make a move, the equity you’ve gained can make a big impact. To find out just how much equity you have in your current home and how you can use it to fuel your next purchase, let’s connect.

About 11,000 Houses Will Sell Today

Some homeowners have been waiting for months to put their house on the market because they don’t think people are buying homes right now. If that’s you, know that even though the housing market has slowed compared to the frenzy of a couple of years ago, it isn’t at a standstill. Contrary to what you may believe, buyers are still active and plenty of homes are selling right now.

According to the National Association of Realtors (NAR), based on the pace of sales right now, just over 4 million homes will sell this year. With some simple math, let’s break down what that really means for you:

- 4.16 million homes divided by 365 days in a year = 11,397 houses sell each day

- 11,397 divided by 24 hours in a day = 475 houses sell per hour

- 475 divided by 60 minutes in an hour = about 8 houses sell each minute

So, on average, about 11,000 homes sell each day in this country.

A real estate expert can give you more information about how many houses are being sold in your neighborhood, the amazing advantages that sellers are experiencing right now, and the most important things buyers are searching for in your area. Together you’ll use this knowledge to shape how you market your house based on local trends.

Bottom Line

If you’ve been waiting to sell because you don’t think there are buyers out there, know today’s market is active. Every day you wait, around 11,000 other homeowners are selling. In the time it took you to read this, eight homes sold. When you’re ready to sell too, let’s connect.

Housing Market Forecast for the Rest of 2023

Some Highlights

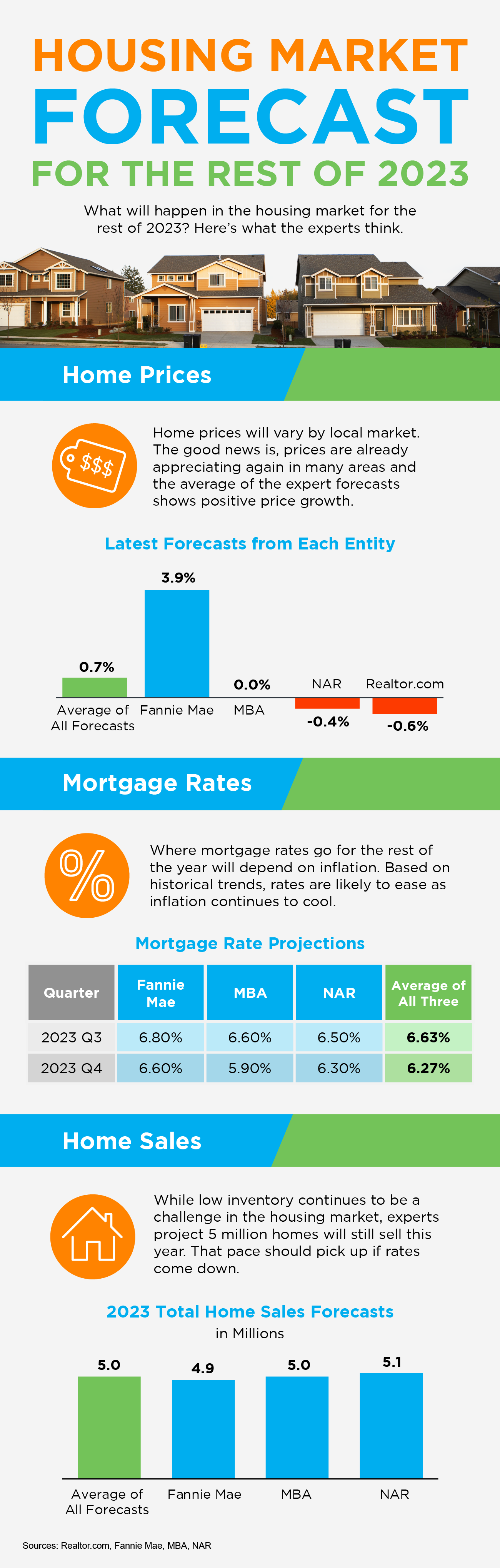

- Want to know what experts say will happen in the rest of 2023? Home prices are already appreciating again in many areas. The average of the expert forecasts shows positive price growth.

- Where mortgage rates go for the rest of the year will depend on inflation. Based on historical trends, rates are likely to ease as inflation continues to cool.

- Even though low inventory continues to be a challenge, experts project 5 million homes will still sell this year. That pace should pick up if rates come down.