Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

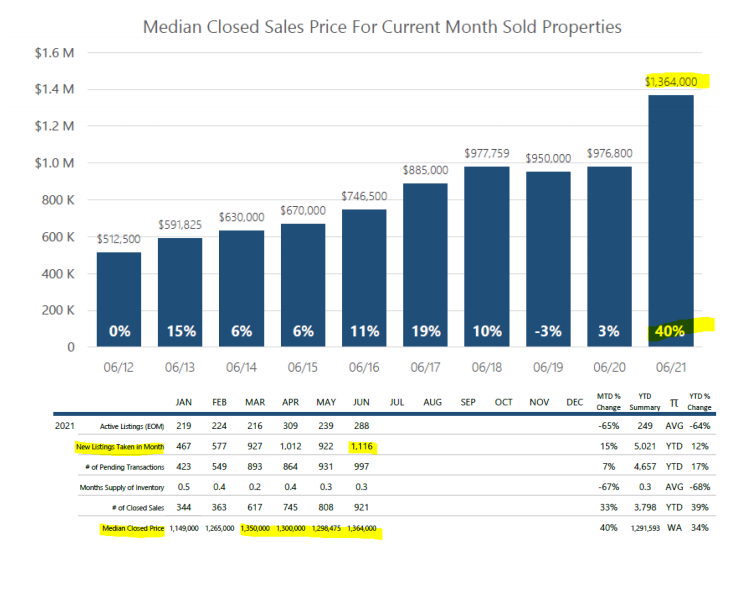

The June statistics show more of the same…..astonishing statistics:

• Median closed sales price $1,364,000 up 40%

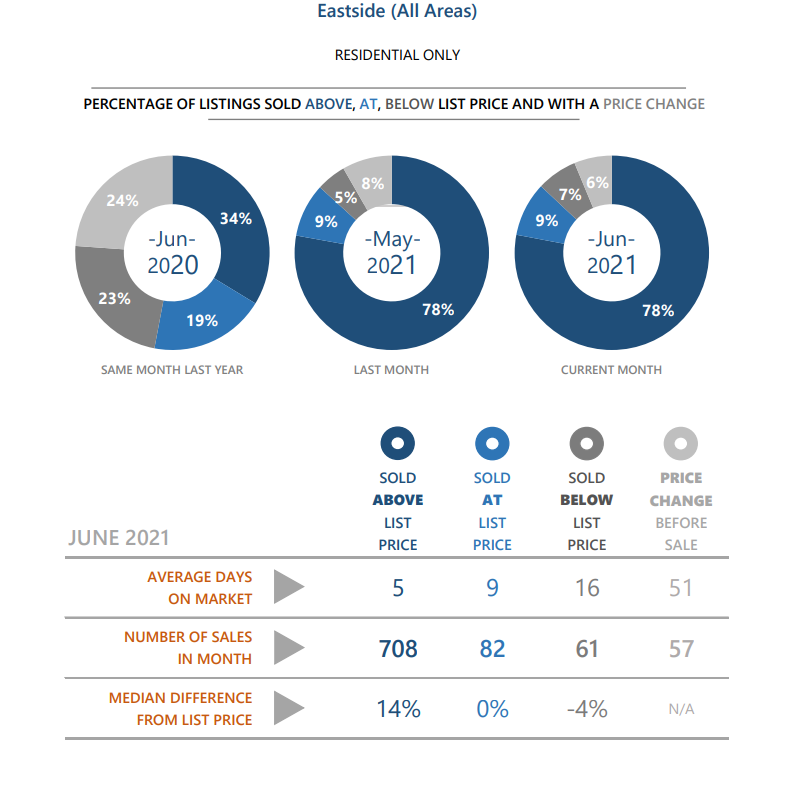

• 78% of homes sold for over the list price. The median over list price paid was 14%.

• 92% of properties that sold had less than 15 days on market.

Looking for signs that our prediction (written in May. Copy below), that Buyers would experience “minor”

relief:

• Median closed sales price for the past four months are relatively flat when compared to the

40% year over year increase: $1,350,000 (March), $1,300,000 (April), $1,298,475 (May), and

$1,364,000 (June).

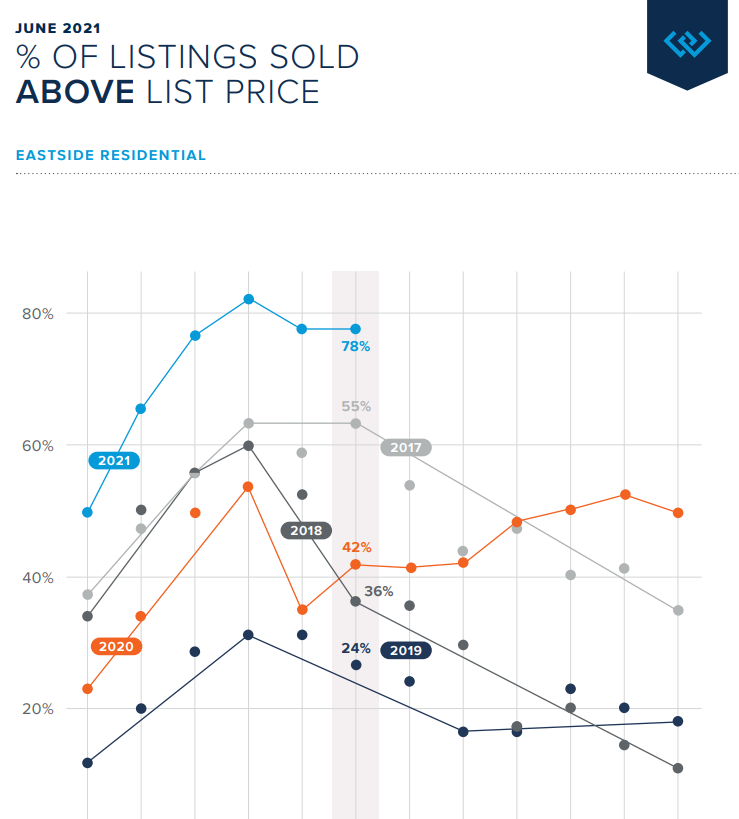

• The percentage of homes sold for over the list price peaked in March and historically drops

from April through December (see page 3 below).

• June had the most new listings this year. July is historically is the third highest number of

new listings behind May and June

The market is so low on inventory that historic norms may not occur. If norms do occur, buyers may

experience minor relief.

• May, June and July are the top three new listings months.

• Historically the percentage of homes selling over list price decreases after April.

• Median closed sale price generally flatten out in the second half of the year.

• Monthly payments, based on the average King County Residential sales price and prevailing 30

year interest rates, as a percentage of an inflationary trend line are approaching previous market

highs (136 vs 140 and 151)

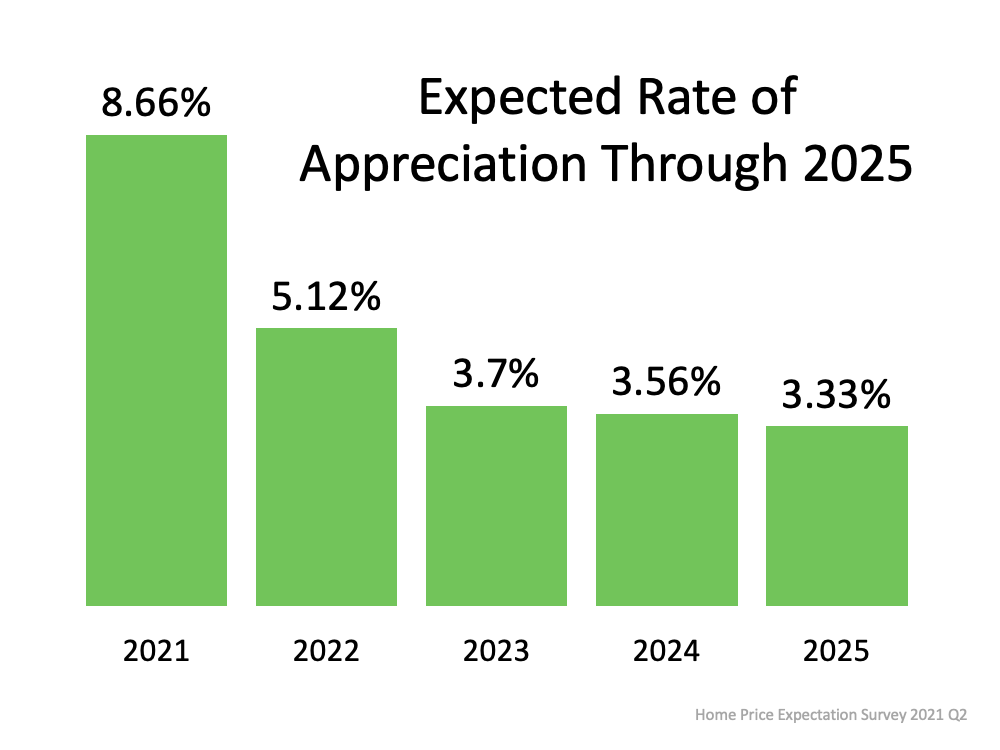

![Homebuyers: Hang in There [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2021/06/24105823/20210625-MEM-1046x2093.png)