Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

You May Not Want To Skip Over That House That’s Been Sitting on the Market

When you see a house that’s been sitting on the market for a while, the reaction is almost automatic. You start thinking:

- What’s wrong with it?

- Why hasn’t anyone bought it yet?

- Am I missing something?

That mindset made sense a few years ago. But in today’s market, you may actually miss out.

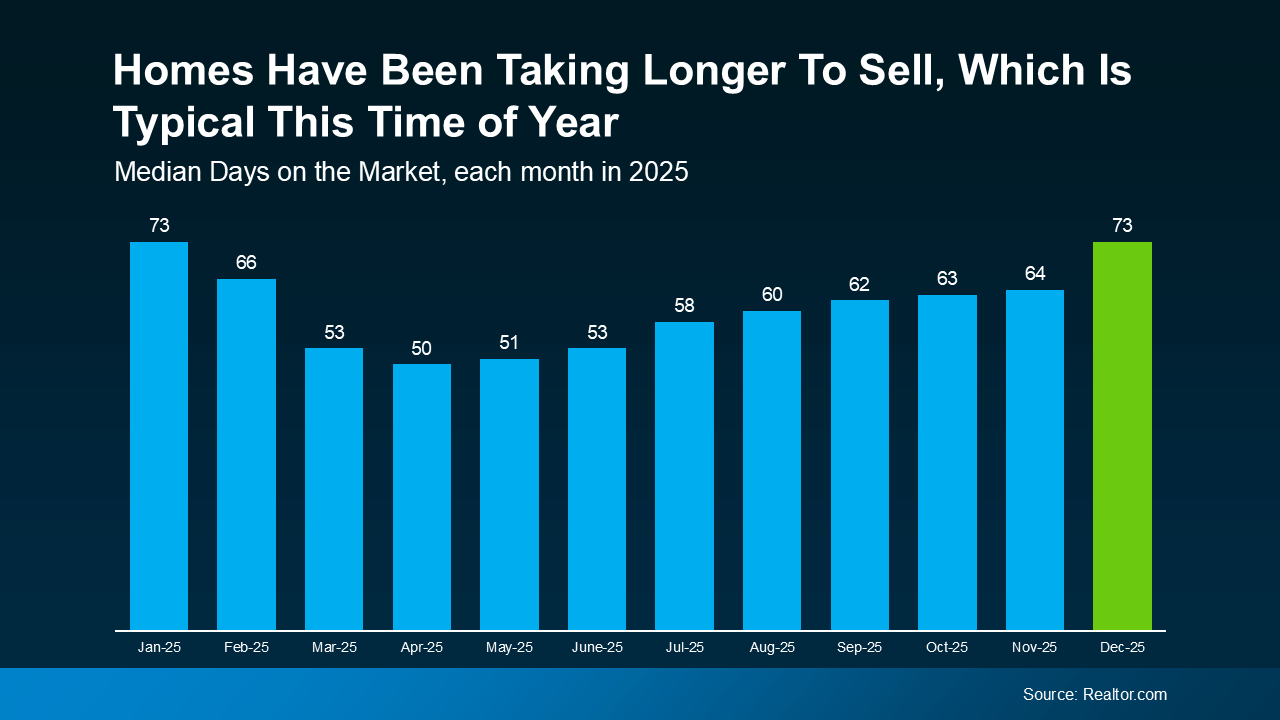

More Time on Market Isn’t Automatically a Concern Anymore

A few years ago, homes sold in just a matter of days. Sometimes, hours. Anything that lingered longer than that raised concerns. But that’s no longer the baseline.

Inventory has grown. Buyers have more choices. And homes are taking longer to sell across the board.

Those are some of the reasons why the typical time it takes a home to sell has climbed this year:

And it’s not that 73 days is slow. That’s actually pretty normal for this time of year. It just feels slow because you heard so much about houses being snapped up in the buying frenzy a few years ago.

That shift alone explains a lot of what you’re seeing. It’s not necessarily that there’s anything wrong with the house itself. Although, let’s be honest, sometimes that is the case.

Most of the time today, a house that’s taking longer to sell simply means:

- There are a lot of homes for sale in that area

- The seller priced a little too high at first

- The home didn’t photograph as well online

- Buyers passed it over for flashier listings nearby

- The timing just wasn’t right when it first hit the market

None of those are necessarily deal-breakers.

What Buyers Often Get Wrong About These Listings

Because even though you may assume a house that hasn’t sold must have hidden issues, the reality is, that’s not always the case. And, if the house does have issues, it’ll show up quickly in your inspection.

That’s information you can use to negotiate. Not a reason to walk away automatically. And in many cases, that’s where buyers find the best deals.

The key is knowing which homes that have been sitting for a while are worth a second look – and which ones aren’t. That’s why working with a local agent makes a real difference. They’ll be able to look at disclosures and more to help you uncover hidden gems other buyers may overlook.

Bottom Line

A home sitting on the market isn’t always a warning sign. Sometimes it’s an overlooked opportunity.

If you want help identifying which homes are worth a second look (and which ones to skip), let’s talk.

Four Ways Your Home Equity Can Work for You

You may have heard homeowners today have a lot of equity built up. But what does that really mean? Let’s break it down.

Because your equity isn’t just a number, it’s a powerful asset that can help you take your next big step in life.

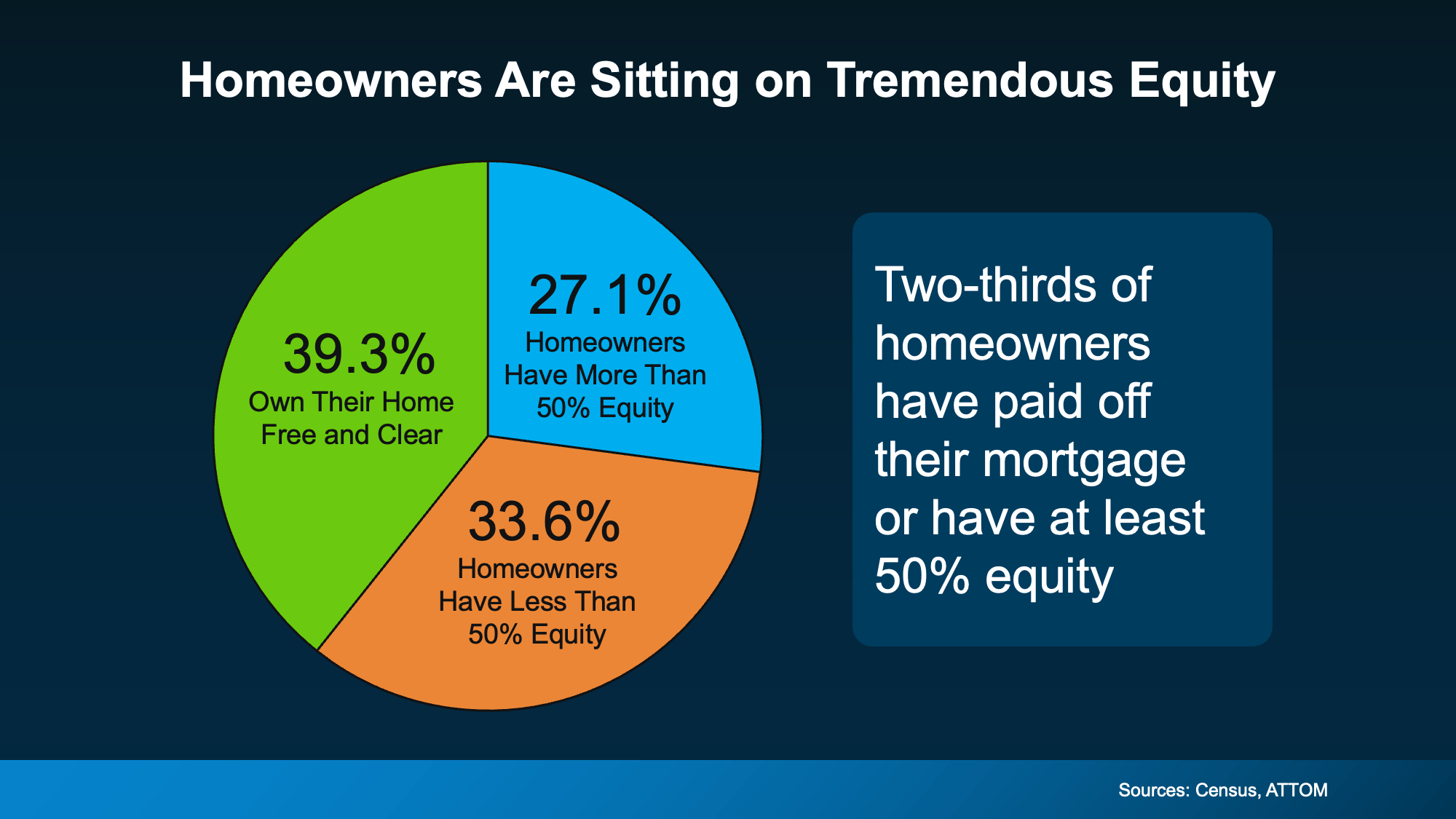

How Much Equity Does the Typical Homeowner Have?

Here’s how it works. As you pay down your loan and home prices rise through the years, the share of your home that you own free and clear grows. That’s your equity.

And according to data from the Census and ATTOM, two-thirds of homeowners have a substantial amount of it today.

39% own their home outright without owing anything on it. And another 27% have at least 50% equity in their homes (see chart below):

That’s a big deal. And just in case you’re wondering how that translates into real dollars, Cotality says the typical homeowner has almost $300k in equity today.

That’s six figures.

And whether you have that much, even more, or a bit less, here are a few examples of how you can use it.

Ways You Could Use Your Home Equity

1. Move Into a Home That Better Fits Your Life

Your needs change over time. Maybe your home is starting to feel cramped, or maybe you have more space than you need now that your adult children have moved out. Either way, you can use your equity as a down payment on a home that’s a better fit for what you need now, and going forward. You may even have enough equity to buy your next house in cash.

2. Upgrade Your Current Home

And if you’re not ready to move just yet, you could reinvest it in your current home instead. Renovations like a kitchen refresh or updated bathrooms could add value when it’s time to sell down the line. Just be sure to talk to a real estate agent before you tackle your project list, so you can prioritize updates that’ll give you the biggest return later on.

3. Fund a Major Life Goal

Equity can also help fund your life goals – whether it’s starting a business, saving for retirement, covering education costs, or helping out someone you love. Some homeowners are even passing down some of that wealth to help fund a loved one’s down payment on a home.

4. Avoid Foreclosure in Tough Times

If you’re struggling with payments, your equity can also be a lifeline. Many homeowners who hit financial hardships can sell their homes and walk away with money in their pockets instead of facing foreclosure. If that’s something on your mind, talk to a real estate expert about your options and how your equity can help.

Your Next Steps

If you’re interested in using your equity for one of the reasons above, here’s what to do:

- Step 1: Ask a local agent for a personalized equity assessment on your home.

- Step 2: Meet with a financial advisor if you’re interested in using that equity.

Because when it comes to tapping into this resource, there are a few things you’ll want to keep in mind – like making sure you still have a good loan-to-value ratio (LTV) even if you use some of your equity.

That means, as a general rule of thumb, you want to maintain at least 20% equity in your home as a financial cushion – something many homeowners didn’t know back in the crash of 2008.

The good news is, according to the Intercontinental Exchange, most of today’s equity meets that guideline:

“As of Q4, mortgage holders have $17.3T in home equity, including $11.2T in tappable equity ‒ accessible via cash-out refinances or home equity lines while maintaining 20% equity in the property . . . ”

Bottom Line

Your home equity is one of the biggest financial assets you have. Whether you’re thinking about moving, remodeling, or working toward a big goal, it’s worth exploring your options. Reach out to a financial advisor to learn more.

What’s one goal you have that you’d go after right now, if you had the funds for it?

February Eastside Stats

The Eastside market remains active but highly selective. Buyers are out there, yet pricing and presentation matter more than ever. Sellers who lead with clarity—pricing realistically and preparing thoughtfully—are the ones attracting serious buyers and avoiding long days on market.

February stats are always a little strange. It feels like we’re well into the new year, but most of the sold data reflects homes that went under contract in December—which is often a very different market than Q1. Pending sales, however, do reflect current buyer behavior, and that’s where things get interesting.

Year over year, pending sales are up 36%, which is genuinely encouraging. New listings are up 28%, though some of that increase likely comes from relists rather than truly new inventory—so total inventory is the better metric to watch. We entered the year with 67% more inventory than last year, and we’re now sitting at 53% higher, so we are moving in the right direction.

The most telling number, though, is months of inventory, which speaks to market velocity. At 1.8 months, we’re technically in a sellers’ market—yet 56% of homes required a price reduction before selling. That disconnect tells you everything you need to know about today’s market.

Year over year, prices are down. The reported 16% depreciation feels artificially high to me; my educated guess is something closer to 5%, but we’ll need more data to confirm that. Frankly, this is one of those moments where the market feels confusing—and that’s okay.

What we are seeing clearly is that homes priced right (or slightly low) are still getting multiple offers. That dynamic will likely show up in next month’s stats—this month’s 6% of homes selling over asking is one of the lowest figures I can remember. Buyers are out there, but they’re selective.

One industry expert put it well: you have to pull the curtain back to see the true market. A meaningful portion of today’s inventory is sitting for a reason—it’s simply not sellable at its current price. When you account for that, the “real” inventory is lower than it appears.

So, what does this all mean?

Sellers should continue to approach the market as both a price war and a beauty competition.

For buyers, the key right now is clarity. Know your numbers, know your non-negotiables, and be ready to act when value shows up. Indecision is more costly than patience in this market.

Top 2026 Housing Markets for Buyers and Sellers

Who doesn’t love a top 10 list? Well, here are two top 10 lists for the housing market this year. But before you take a look, there’s something you should know. If a move is on your radar for 2026, here’s the most important thing you need to understand upfront: there isn’t one housing market this year – there are many.

Experts agree 2026 is shaping up to be one of the most geographically split housing markets in years. Some areas are tilting in favor of sellers, while others are opening real doors for buyers. Who has the advantage depends almost entirely on where you are. Selma Hepp, Chief Economist at Cotality, puts it this way:

“Looking ahead to 2026, regional differences will remain pronounced, with demand favoring areas that offer both economic opportunity and relative affordability.”

To show just how divided the landscape is, here’s a look at where sellers are expected to have the upper hand, and where first-time buyers may finally find their opening this year.

Where Sellers Are Poised To Win Big in 2026

Zillow identified the following metros as some of the strongest seller markets for 2026, based on buyer demand, pricing momentum, and how quickly homes are expected to sell:

In markets like these, buyers are going to be competing for limited inventory, which gives sellers more leverage.

Homeowners in seller’s markets this year can expect:

- Stronger buyer interest

- Shorter time on market

- Better odds of selling close to (or above) asking price

That doesn’t mean every listing is guaranteed success. But it does mean sellers who prepare well and lean on an agent’s expertise should be very happy with their results in 2026.

Markets Where There’s More Opportunity for First-Time Buyers

On the flip side, here’s a look at where buyers have the power – in particular, first-time buyers, since they’ve had the hardest time breaking into the market lately. Realtor.com highlights the top metros where first-time buyers are expected to have better opportunities in 2026:

These markets stand out for a mix of:

- More affordable home prices

- Better housing availability

- Strong local amenities and economic health

For first-time buyers, that combination matters. It’s what could finally turn “someday” into “this could actually work.” In buyer’s markets, they should expect:

- Less intense competition

- More room to negotiate

- A clearer path to getting an offer accepted

What Matters More Than Any Top 10 List

Not seeing your city on the list? Don’t stress. This is just a national snapshot, not a judgment on your local market. The goal here is just to show you how different the market really is depending on where you are.

And remember, you can buy or sell no matter how your local market leans. You just need an agent’s help to figure out the right strategy to get it done. For example:

- A seller in a more buyer-friendly metro may need to be aggressive on their price and prep.

- A buyer in a seller-leaning area may still need to come prepared with their best offer.

To find out where your market falls and what you should expect, you’ll want the help of a local expert.

Bottom Line

The housing market in 2026 isn’t one-size-fits-all. It’s a year where local conditions matter more than ever.

Whether your market leans more buyer-friendly or seller-friendly, the right strategy can put you in a strong position. And that’s where a local expert comes in. Let’s connect.

It’s Getting More Affordable To Buy a Home

There’s finally a little good news for anyone who’s been priced out or sitting on the sidelines.

Buying a home is getting more affordable.

Monthly payments have started to come down, and the squeeze buyers have been feeling for the past few years is slowly loosening. Now, that doesn’t mean everyone can suddenly afford a home, but with how tough the market’s been, the improvement we’re seeing matters.

Affordability Is Finally Moving in the Right Direction

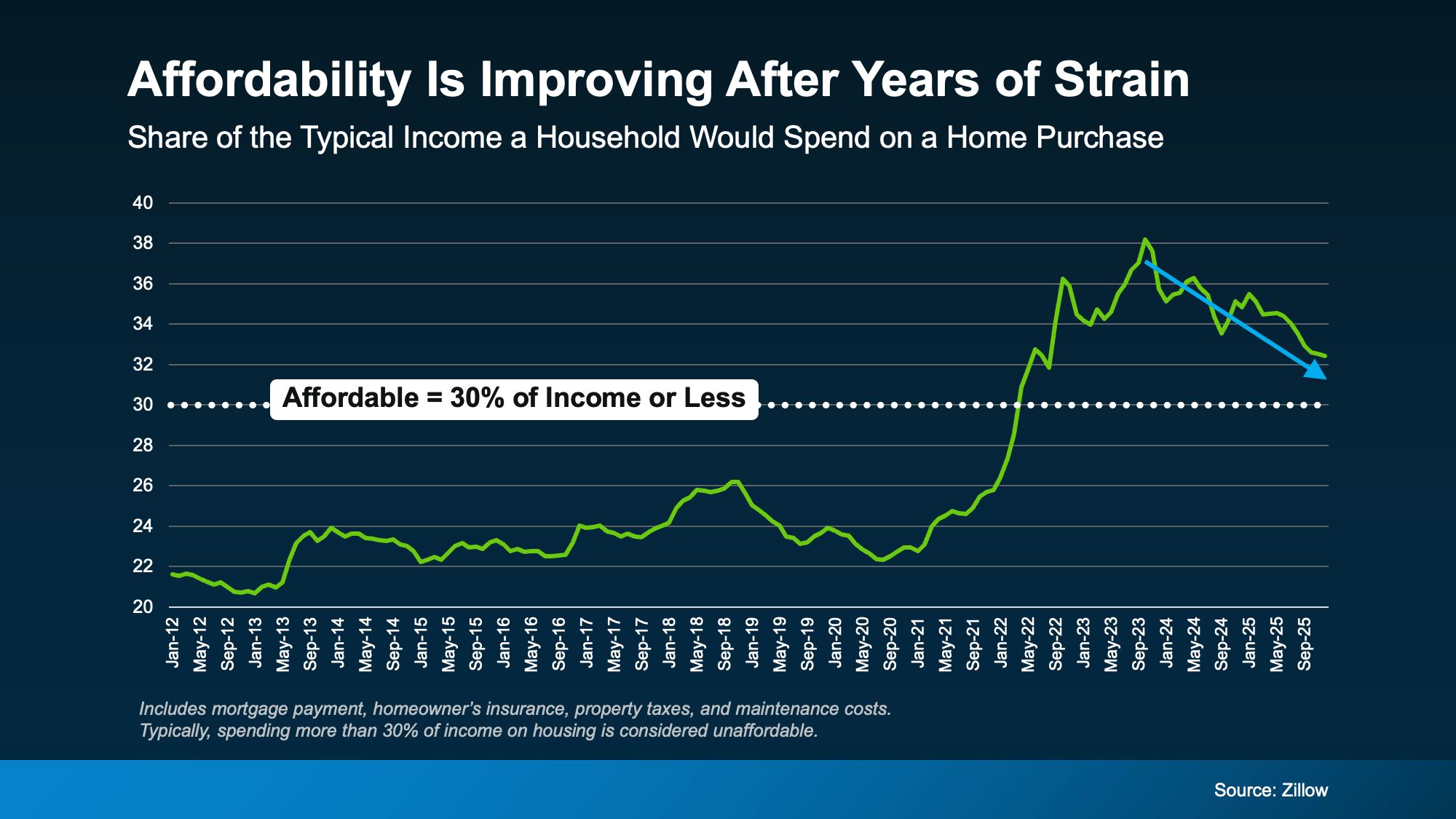

One of the best ways to see this shift is by looking at how much of a household’s income it takes to buy a home.

According to Zillow, housing is typically considered affordable when it takes 30% or less of your monthly income to cover your expenses. That includes your mortgage payment, taxes, insurance, and basic maintenance.

For the past few years, the math was well above that threshold, and it made buying a home unachievable for many. But now, we’re slowly moving back toward a balance. Zillow research shows it’s taking less of a typical household’s income to buy a home than it did just a few years ago (see graph below):

Now, we’re not all the way back to Zillow’s threshold of 30% of your income or less, so affordability is still tight. But things are trending in the right direction.

Why Affordability Is Improving

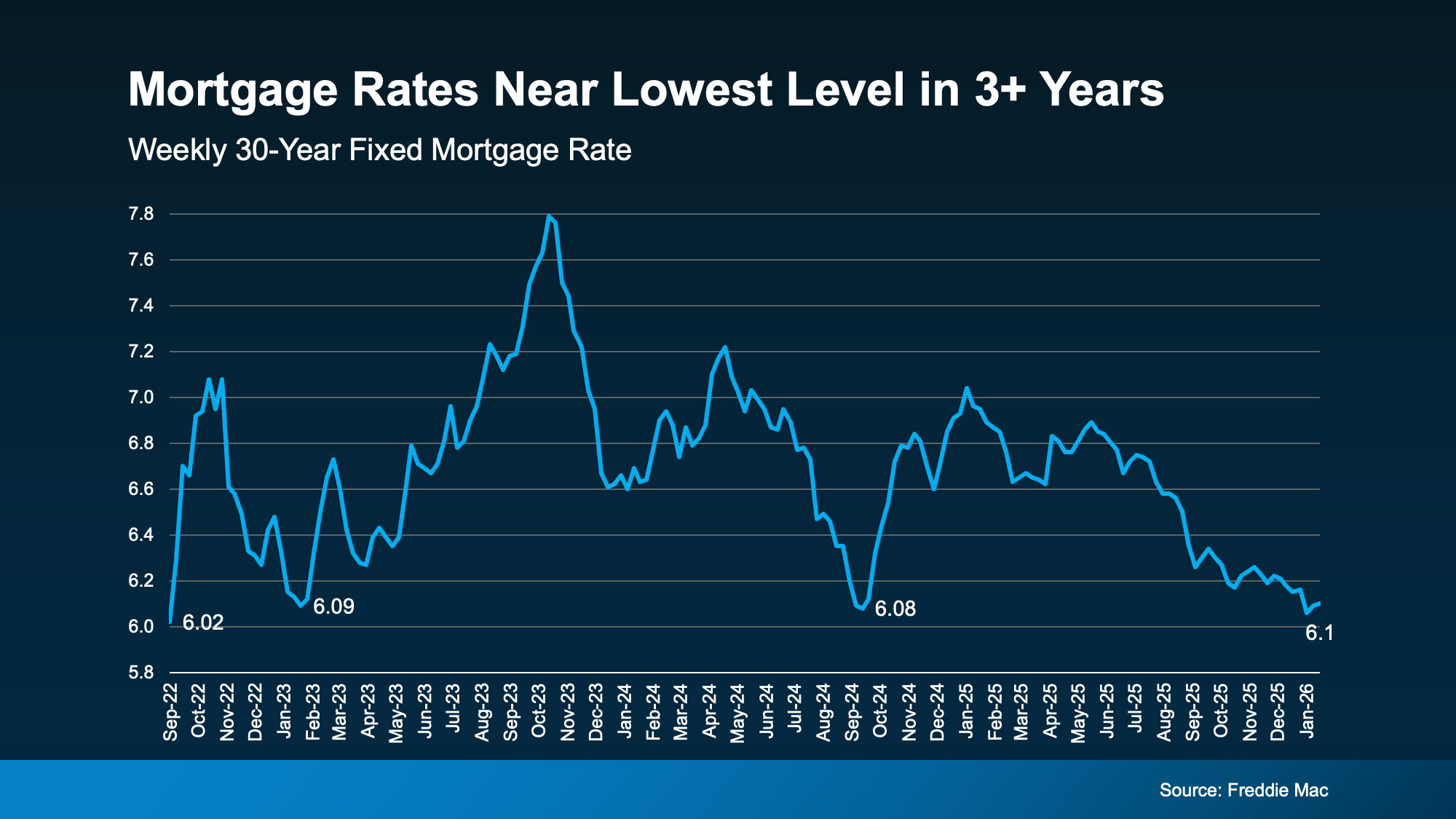

So, what’s driving the change? A lot of the focus lately has been on mortgage rates and how much they’ve come down over the course of the past year. But that’s not the only factor working in favor of buyers right now. Here are three trends benefiting buyers today:

- Mortgage rates have eased. Rates are near their lowest level in more than three years, which helps lower monthly payments (see graph below):

- Home price growth has cooled. Prices aren’t falling nationally, but they’re growing much more slowly than they were a few years ago. That means buyers today aren’t facing the same sharp jumps in purchase prices, which helps keep monthly payments more manageable – and buying more predictable.

- Wages are growing faster than home prices. This one matters a lot. As Mark Fleming, Chief Economist at First American, explains:

“When income growth exceeds house price growth, house-buying power improves—even if mortgage rates don’t decline meaningfully.”

None of this makes buying cheap, but it does explain why the math is starting to work a little better for buyers than it did even a just a year ago. Put simply, the forces that hurt affordability over the past few years are finally easing. Fleming again explains it well:

“Affordability remains challenging, but for the first time in several years, the underlying forces are finally aligned toward gradual improvement. Mortgage rates may drift down only slowly, but income growth exceeding house price appreciation will provide a boost to house-buying power — even in a higher-rate world. Affordability won’t snap back overnight, but like a ship finally catching a steady tailwind, it’s now sailing in the right direction.”

These three factors combined are why economists expect affordability to keep improving in 2026.

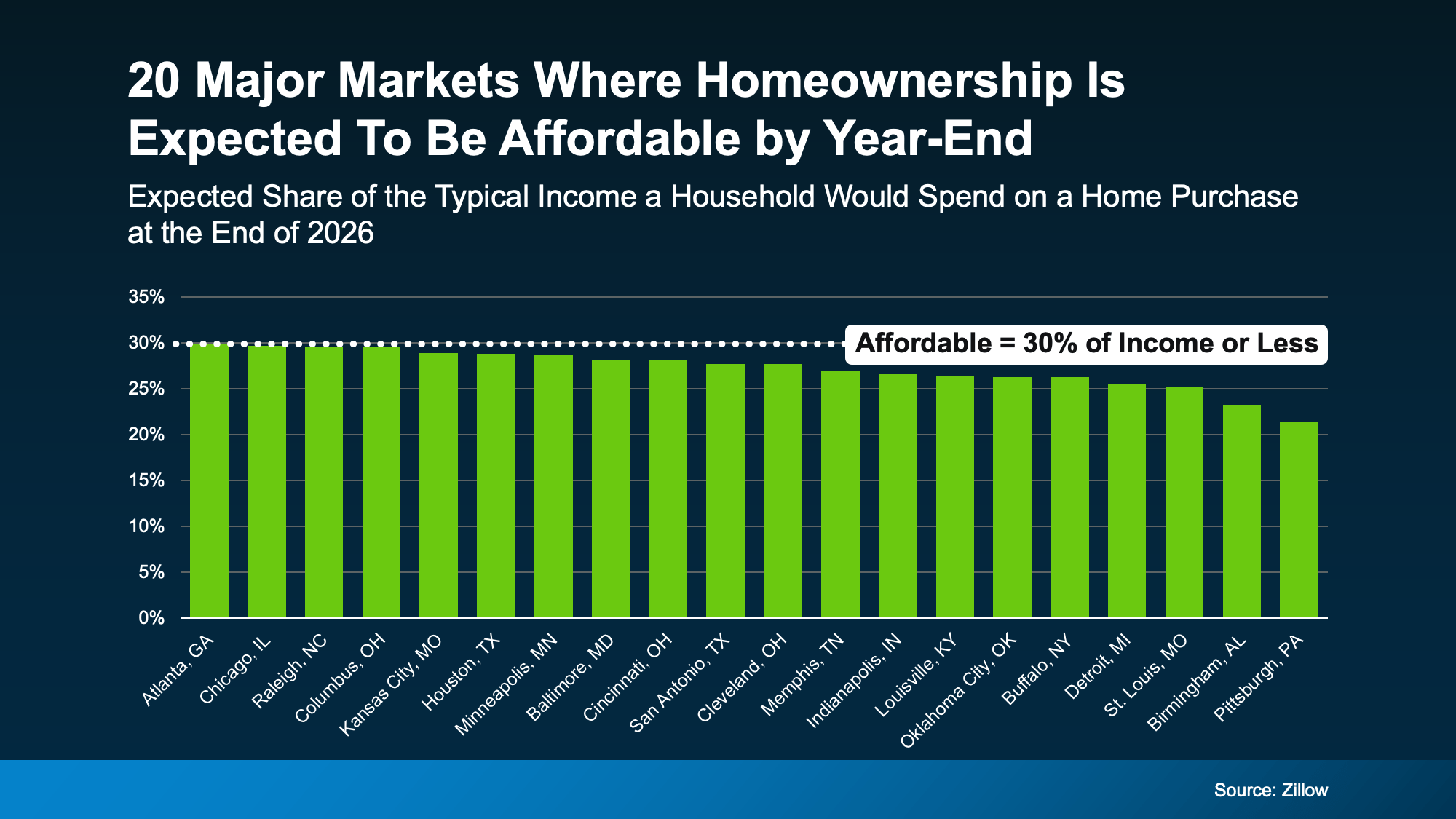

Where Homes Are Becoming Affordable First

But how much is affordability really going to improve? In some places, noticeably. Zillow says some markets are expected to fall back under their affordability threshold (30% of your income or less) by the end of the year:

But that doesn’t mean you have to be in one of these markets or wait until year-end to buy. Other places are already seeing big improvements in affordability. So, talk to a local agent about what’s happening in your market. You may find you’re able to buy after all.

Bottom Line

For the first time in quite a while, affordability is easing. That’s a meaningful shift.

And because this improvement isn’t happening everywhere at the same speed, understanding what’s changing locally is what really makes a difference. If you want to see how these trends show up in our area, let’s talk it through.

Why So Many Homeowners Are Downsizing Right Now

For a growing number of homeowners, retirement isn’t some distant idea anymore. It’s starting to feel very real.

According to Realtor.com and the Census, nearly 12,000 people will turn 65 every day for the next two years. And the latest data shows as many as 15% of those older Americans are planning to retire in 2026. And another 23% will do the same in 2027.

If you’re considering retiring soon too, here’s what you should be thinking about.

Why Downsize?

Now’s the perfect time to reflect on what you want your life to look like in retirement. Because even though your finances will be going through a big change, you don’t necessarily want to feel like you’re living with less.

But odds are, what you do want is for life to feel easier.

Easier to enjoy.

Easier to manage.

Easier to maintain day-to-day.

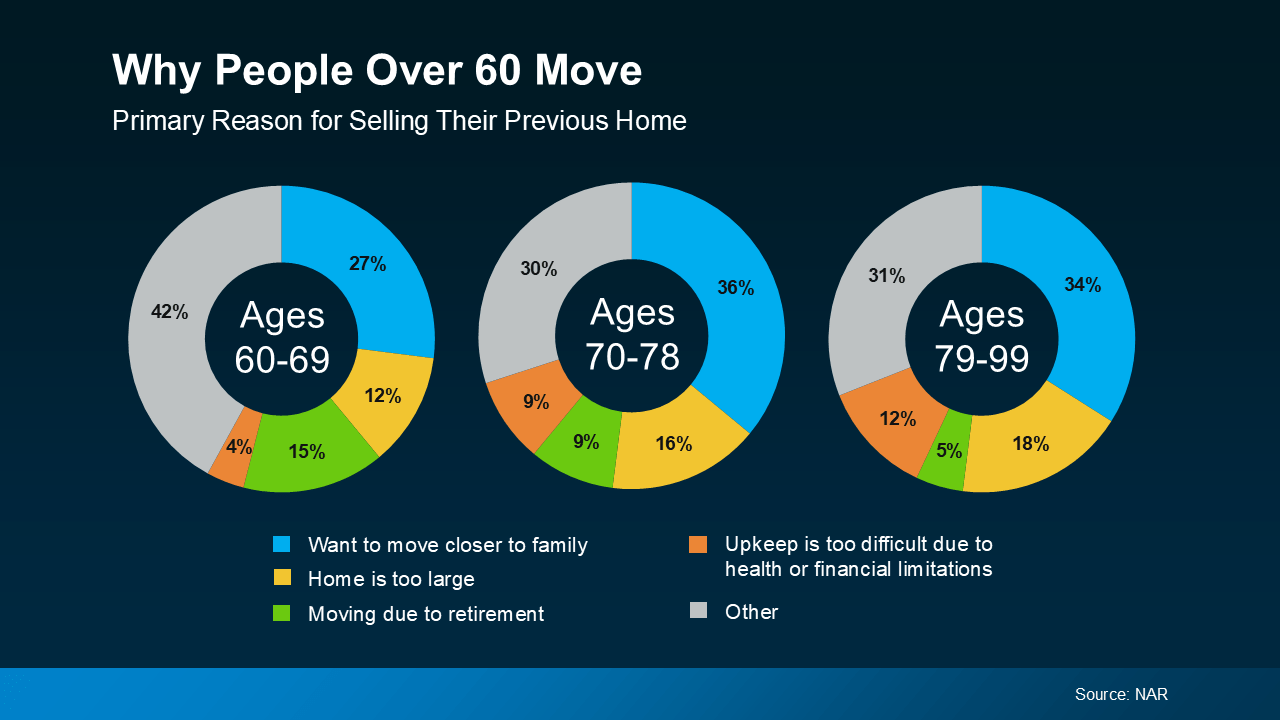

The Top Reasons People Over 60 Move

You can see these benefits show up in the data when you look at why people over 60 are moving. The National Association of Realtors (NAR) finds the top 4 reasons aren’t about timing the market or chasing top dollar. They’re about lifestyle:

- Being closer to children, grandchildren, or long-time friends so it’s easier to spend more time with the people who matter most

- Wanting a smaller, more functional home with fewer stairs and easier upkeep

- Retiring and no longer needing to live near the office, so it’s easier to move wherever you want

- Opting for something smaller to reduce monthly expenses tied to utilities, insurance, and maintenance

No matter the reason, the theme is the same: downsizing isn’t about giving something up. It’s about gaining control and choosing simplicity. And it brings peace of mind to know your home fits the years ahead, not the years behind.

And the best part? It’s more financially feasible now than many homeowners would expect.

The #1 Thing Helping So Many Homeowners Downsize

Here’s the part that makes it possible. Thanks to how much home values have grown over the years, many longtime homeowners are realizing they’re in a stronger position than they thought to make that move.

According to Cotality, the average homeowner today has about $299,000 in home equity. And for older Americans, that number is often even higher – simply because they’ve lived in their homes longer.

When you stay in one place for years (or even decades), two things happen at the same time:

- Your home value has time to grow.

- Your mortgage balance shrinks or disappears altogether.

That combination creates more options than you’d expect, even in today’s market.

So, whether you just retired, or you’re about to, it’s not too soon to start thinking about what comes next. Sure, it can be hard to leave the house you made so many years of memories in, but maybe it’s time to close one chapter to open a new one that’s just as exciting.

Bottom Line

Downsizing is about setting yourself up for what comes next – on your terms.

If retirement is on the horizon and you’ve started wondering what your current house (and your equity) could make possible, the first step isn’t selling. It’s understanding your options.

Let’s talk. A simple, no-pressure conversation can help you see what downsizing might look like – and whether it makes sense for you.